Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Trial Balance

- Advantages and Disadvantages, with Examples

- Types

- Methods of Preparation

- Steps to Prepare Trial Balance

- Example: Preparation of Trial Balance

- Road to Trial Balance

- Key Takeaways

Definition : Trial Balance

A trial balance is a statement that lists the debit and credit balances of all ledger accounts on a specific date to check the mathematical accuracy of the books.

Advantages and Disadvantages,with Examples

| Advantage | Explanation | Example |

|---|---|---|

| Helps detect errors quickly | If debit and credit totals don’t match, it shows there’s a mistake somewhere. | Totals don’t match by ₹500, so the accountant rechecks and finds a posting error. |

| Saves time in error checking | Instead of checking each transaction, it gives a quick math check of all accounts. | The accountant finds the sum mismatch early, avoiding costly manual rechecks. |

| Useful for preparing final accounts | Provides a summarized list of all account balances for preparing financial statements. | Trial balance totals matched, so the profit and loss account is prepared using these balances. |

| Easy to review and analyze accounts | Shows all ledger balances in one place, making it convenient to review finances. | Management sees a high purchase balance and decides to control expenses. |

| Internal control tool | Helps identify errors or frauds before finalizing accounts. | Duplicate transactions were spotted because the trial balance didn’t tally. |

| Disadvantage | Explanation | Example |

|---|---|---|

| Does not detect all errors | Some mistakes, like posting a wrong amount on the correct side, won’t show up. | Posting ₹500 less instead of ₹5,000 but still on the debit side won’t be caught. |

| Cannot find omission errors | If a transaction is completely left out, trial balance still “tallies” (totals are equal on both sides) | A sale not recorded at all won’t affect trial balance totals. |

| Compensating errors may hide mistakes | Two mistakes cancelling each other won’t show imbalance. | Errors in two accounts that offset make totals appear equal. |

| Time-consuming to prepare manually | Making a trial balance by hand is detailed work for many accounts. | A shop with 100 ledger accounts takes hours to summarize accurately. |

| Limited information | Shows totals but not details or correctness of each transaction. | A trial balance won’t show if assets are overstated wrongly. |

Types

| Type | What It Means | When It’s Prepared | Why It’s Used |

|---|---|---|---|

| Unadjusted Trial Balance | A list of all ledger account balances before making any corrections or changes | At the end of an accounting period, before adjustments | To check if debits and credits match before fixing entries |

| Adjusted Trial Balance | Updated balances after making necessary corrections (for expenses or income) | After passing adjusting entries | To prepare accurate financial statements like income statement and balance sheets |

| Post-Closing Trial Balance | Balances after closing temporary accounts (such as expenses and income accounts) | After closing all temporary accounts | To ensure books are balanced and ready for the next accounting period |

Important Terms

-

Adjusting Entries: Changes made at the end of the accounting period to record expenses or revenue that occurred but were not yet recorded.

-

Temporary Accounts: Accounts like revenue and expenses that get closed at the end of the accounting period.

-

Permanent Accounts: Accounts related to assets, liabilities, and capital that continue to the next accounting period.

Methods of Preparation

| Method | Description | When to Use | Advantages | Disadvantages |

|---|---|---|---|---|

| Total Method (Gross Trial Balance) | List the total debit and credit entries of each ledger account separately without balancing the account. | After posting all journal entries but before balancing accounts. | Quick to prepare initially. | Does not show net balances; less useful for final accounts. |

| Balance Method (Net Trial Balance) | List only the net balance (either debit or credit) of each ledger account after balancing. | Most common; used before preparing final accounts. | Clear view of actual balances for financial statements. | Requires all ledger accounts to be balanced first. |

| Totals-cum-Balances Method | Shows both total debits/credits and net balances side by side in the trial balance with four columns. | Rarely used due to complexity and time involved. | Very detailed and accurate. | Time-consuming and more complex. |

| Vertical Form (Journal Format) | The trial balance is presented in a list form with columns for account name, ledger folio, debit, and credit. | Used in reports and easy to prepare on paper or spreadsheet. | Simple and easy to read in report form. | Can become lengthy with many accounts. |

| Horizontal Form (Ledger Format) | A trial balance is shown as two sides: debit balances on one side and credit balances on the other, like ledger accounts. | Useful for smaller businesses or manual bookkeeping. | Mimics ledger format; easy to compare debit and credit sides. | Less compact, may require more space. |

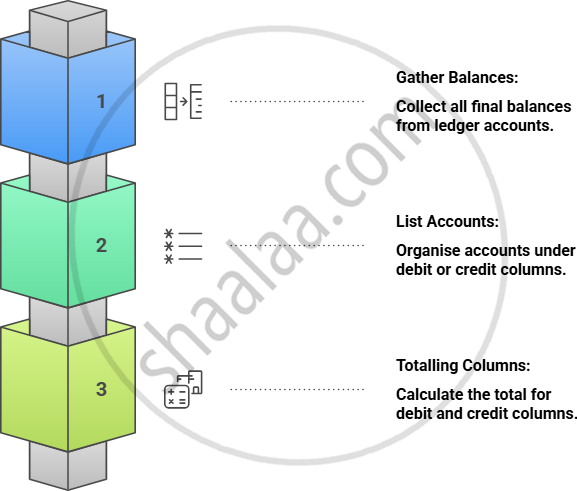

Steps to Prepare Trial Balance

What If the Totals Don’t Match?

-

Recheck ledger posting.

-

Review additions and carry-forwards

-

Search for missed, double, or wrongly posted entries.

Example : Preparation of Trial Balance

Suppose a small business has the following ledger balances at the end of the month:

-

Cash: ₹10,000 (Debit)

-

Purchases: ₹7,000 (Debit)

-

Rent Expense: ₹2,000 (Debit)

-

Sales: ₹15,000 (Credit)

-

Capital: ₹3,000 (Credit)

-

Bank Loan: ₹1,000 (Credit)

Trial Balance as on 31.03.2025 (Vertical Form)

| Sr. No. | Name of Account | L.F. | Debit (₹) | Credit (₹) |

|---|---|---|---|---|

| 1 | Cash | 10,000 | ||

| 2 | Purchases | 7,000 | ||

| 3 | Rent Expense | 2,000 | ||

| 4 | Sales | 15,000 | ||

| 5 | Capital | 3,000 | ||

| 6 | Bank Loan | 1,000 | ||

| Total | 19,000 | 19,000 |

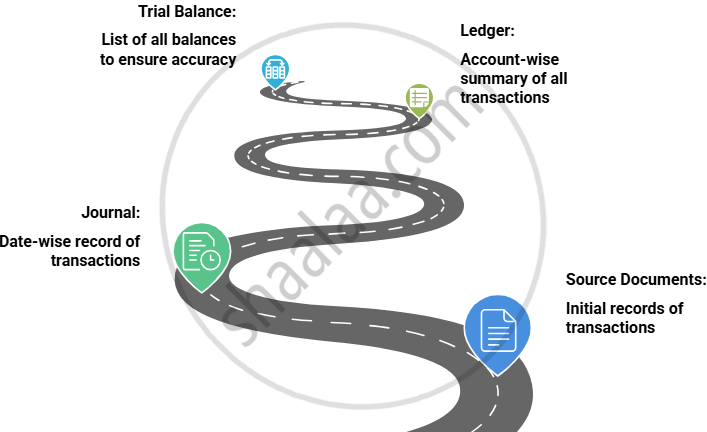

Road to Trial Balance

Key Takeaways

- A trial balance is a financial report that lists all ledger account balances in debit and credit columns at a specific date to check the mathematical accuracy of bookkeeping.

- It ensures that total debits equal total credits, helping detect errors before preparing final financial statements.

- Though it confirms arithmetic correctness, some errors like omissions or misclassifications may remain undetected.

- The trial balance serves as a crucial step in the accounting process to summarize financial transactions and prepare reports like the profit and loss account and balance sheet.

Related QuestionsVIEW ALL [9]

Prepare a trial balance with the following information:

| Name of the account | ₹ | Name of the account | ₹ |

| Purchases | 1,00,000 | Sales | 1,50,000 |

| Bank Loan | 75,000 | Creditors | 50,000 |

| Debtors | 1,50,000 | Cash | 90,000 |

| Stock | 35,000 | Capital | 1,00,000 |