Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Pay-in-Slip

- Sample

- Advantages and Disadvantages

- Process Flow of a Pay-in-Slip

- Key Takeaways

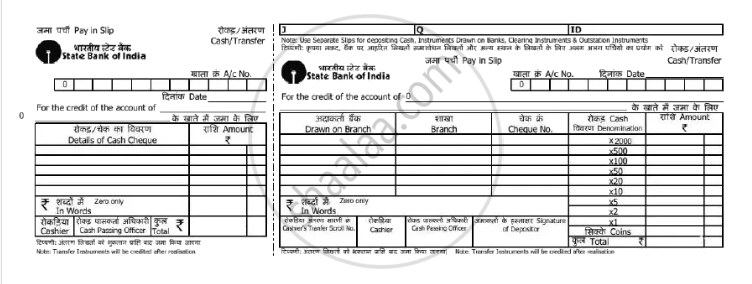

Definition : Pay-in-Slip

A pay-in-slip (also called deposit slip) is a form provided by banks that the account holder fills when depositing cash or a cheque into a bank account.

Sample Pay-in-Slip

Contents:

-

Bank Details: "State Bank of India" is printed at the top with the bank logo for easy identification.

-

Account Details: Spaces for the account number (A/c No.), date, and account holder’s name for whom the deposit is made.

-

Type of Transaction: The form mentions whether the deposit is by cash or transfer.

-

Cheque Section: Includes areas for "Drawn on Branch," "Branch," and "Cheque No." for those depositing cheques and not cash.

-

Cash Denominations: Lists rows for ₹2000, ₹500, ₹100, ₹50, ₹20, ₹10, and coins. You fill in how many notes/coins of each you are depositing, ensuring transparency and helping the bank verify the sum.

-

Amount Columns: Separate columns for entering individual and total amounts. There’s also a line for writing the total amount in words.

-

Signature fields: The depositor signs the form, and bank officials (cashier, cash posting officer) also sign after verifying.

-

Counterfoil: The left side is a copy for the depositor, stamped as a receipt, while the right side stays with the bank for record-keeping.

- PAN card number of account holder if the amount of deposit is more than ₹50,000 (It is used by the tax departmentment to track high-value transactions)

Advantages and Disadvantages

| Advantages | Disadvantages |

|---|---|

| Provides written proof of deposit | Slips can be lost or misplaced |

| Helps prevent errors in account credit | Filling out forms can be slow and inconvenient |

| Ensures proper record-keeping for bank & customer | Not user-friendly for those with low literacy |

| Useful for auditing and resolving disputes | Manual processing may lead to delays or mistakes |

| Promotes transparency and internal checks | Not suitable for modern digital transactions |

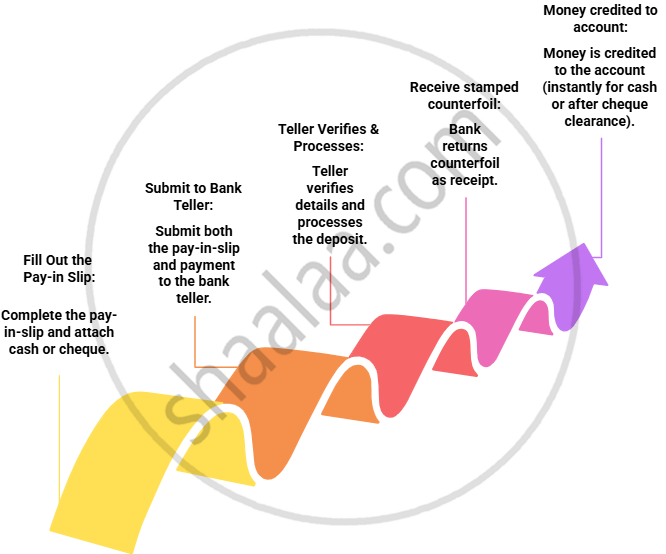

Process Flow of a Pay-in-Slip

Key Takeaways

-

A pay-in-slip is a form used in Indian banks to deposit cash or cheques into an account, recording all important transaction details.

- It ensures clarity and accuracy and serves as legal evidence of the transaction.

-

It contains spaces for bank and branch name, account number, date, amount (in figures and words), depositor’s name, type of account, denomination details, cheque details, and PAN for deposits above ₹50,000.

-

The counterfoil (stub) is the stamped portion returned to the depositor as proof of deposit; the bank keeps the other side.

-

Main steps: Fill the slip clearly, attach cash/cheque, submit at the bank, receive the stamped counterfoil, and check for the deposit in the account.