Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Two Column Cash Book

- Definition: Contra Entry

- Features of Two Column Cash Book

- Format and Contents

- Accounting Treatment: Banking Transactions

- Balancing the Two Column Cash Book: Cash Column

- Balancing the Two Column Cash Book: Bank Column

- Types of Bank Accounts

- Examples: Recording Transactions in Two Column Cash Book

- Key Takeaways

Definition : Two Column Cash Book

A two column cash book is a special accounting book that has two money columns—one for cash and one for bank—on each side, used to record all cash and bank transactions (including cheques, deposits, and withdrawals) using the double-entry system.

Definition : Contra Entry

A contra entry is an accounting transaction where funds are transferred between a business’s cash and bank accounts—both aspects (debit and credit) are recorded within the same cash book but in different columns, and such entries do not affect the overall financial position of the business.

Features of Two Column Cash Book

Format and Contents

In the books of --------------

Dr. Two column Cash Book Cr.

| Date | Receipts | R. No. | L.F. | Cash (₹) | Bank (₹) | Date | Payments | V. No. | L.F. | Cash (₹) | Bank (₹) |

|---|---|---|---|---|---|---|---|---|---|---|---|

Contents:

-

Date: The day the transaction takes place.

-

Particulars: The details or description of the account involved (such as “To Sales A/c” or “By Purchases A/c”).

-

Voucher/Receipt No.: The serial number for each payment or receipt.

-

Ledger Folio (L.F.): The page number in the ledger where the account is posted.

-

Cash Column: Used to record amounts received or paid in cash.

-

Bank Column: Used to record bank-related amounts such as deposits, withdrawals, or cheque transactions.

Accounting Treatment : Banking Transactions

| Transaction/Event | Where Recorded in Cash Book | Journal Entry |

|---|---|---|

| Opening balance (debit) | Receipt side, Bank column (“To Balance b/d”) | (Opening balance, so no entry) |

| Opening balance (overdraft/credit) | Payment side, Bank column (“By Balance b/d”) | (Overdraft, so no entry) |

| Crossed cheque received | Receipt side, Bank column | Bank A/c…Dr To Sales/Asset/Income/Debtor’s A/c |

| Bearer cheque received | Receipt side, Cash column | Cash A/c… Dr To Sales/Asset/Income/Debtor’s A/c |

| Cheque received & deposited same day | Receipt side, Bank column | Bank A/c…Dr To Sales/Asset/Income/Debtor’s A/c |

| Cheque received dishonoured | Payment side, Bank column | Person’s A/c…Dr To Bank A/c |

| Cheque issued | Payment side, Bank column | Purchases /Expenses/Assets /Creditor’s A/c… Dr To Bank A/c |

| Cheque issued dishonoured | Receipt side, Bank column | Bank A/c…Dr To Person’s A/c |

| Cash withdrawn from bank (personal use) | Payment side, Bank column (“By Drawings A/c”) | Drawings A/c…Dr To Bank A/c |

| Direct deposit by customer into bank | Receipt side, Bank column (“To Customers A/c”) | Bank A/c…Dr To Customer’s A/c |

| Interest allowed by bank | Receipt side, Bank column (“To Interest A/c”) | Bank A/c… Dr To Interest A/c |

| Interest charged on overdraft debited by bank | Payment side, Bank column (“By Interest on overdraft A/c”) | Interest on overdraft A/c…Dr To Bank A/c |

| Bank charges debited by bank | Payment side, Bank column (“By Bank Charges A/c”) | Bank Charges A/c… Dr To Bank A/c |

| Dividend/interest on investment by bank | Receipt side, Bank column (“To Interest on Investment/Dividend A/c”) | Bank A/c… Dr To Interest on Investment/Dividend A/c |

| Payment by bank under standing instruction | Payment side, Bank column (“By Respective Expenses A/c”) | Respective Expenses A/c… Dr To Bank A/c |

| Cash credit/loan account to current account | Receipt side, Bank column (“To Cash Credit/Loan A/c”) | Bank A/c…Dr To Cash Credit/Loan A/c |

| Current account to cash credit/loan account | Payment side, Bank column (“By Cash Credit/Loan A/c”) | Cash Credit/Loan A/c…Dr To Bank A/c |

| Personal savings to current account (capital introduced) | Receipt side, Bank column (“To Capital A/c”) | Bank A/c… Dr To Capital A/c |

| Current account to personal savings (drawings) | Payment side, Bank column (“By Drawings A/c”) | Drawings A/c…Dr To Bank A/c |

| Contra (cash deposited into bank) |

|

Bank A/c…Dr To Cash A/c |

| Contra (cash withdrawn from bank for office use) |

|

Cash A/c…Dr To Bank A/c |

| Contra (bearer cheque deposited into bank, received earlier) |

|

Bank A/c…Dr To Cash A/c |

Important Terms:

- Standing instruction to the bank: A request given by a customer to the bank to automatically pay certain bills or transfer money on a regular schedule, so the payments happen without needing to remember or do them manually.

- Overdraft: When the bank lets a person or business spend more money than is actually in their account, up to an approved limit, and charges interest on the amount used.

- Direct deposit: Money is sent straight into a person’s bank account electronically, without using cash or cheques.

- Cash credit: A short-term loan facility from the bank that allows a business to borrow money as needed up to a certain limit, usually by pledging security or assets.

- Pledging of securities or assets means giving your shares, property, or other valuables to the bank as security for a loan, so if the loan is not repaid, the bank can take or sell those assets to recover the money.

- Current account: A type of bank account mainly for businesses that allows unlimited deposits and withdrawals and is often used for frequent transactions.

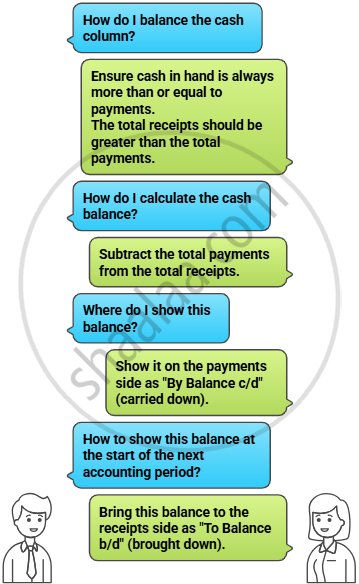

Balancing the Two Column Cash Book : Cash Column

Balancing the Two Column Cash Book : Bank Column

| Situation | How to Show in Current Period | How to Show in Next Period |

|---|---|---|

| Receipts > Payments (positive/normal balance) | Payment side: "By Balance c/d" | Receipt side: "To Balance b/d" |

| Payments > Receipts (overdraft/credit balance) | Receipt side: "To Balance c/d" | Payment side: "By Balance b/d" |

Types of Bank Accounts

| Type of Account | Who is it for? | Key Features | Interest |

|---|---|---|---|

| Savings Account | People with regular/fixed income |

|

Yes |

| Fixed Deposit Account | Anyone wanting to save lump sum |

|

Highest |

| Recurring Deposit Account | Regular savers (monthly) |

|

Higher than savings, but lower than fixed deposit |

Examples : Recording Transactions in Two Column Cash Book

List of transactions to prepare a two column cash book in the books of XYZ Enterprises for September-October 2025:

| Date | Particulars | Amount (₹) |

|---|---|---|

| Sept. 1 | Started business with Cash | 80,000 |

| Sept 4 | Cash deposited into Bank of India | 10,000 |

| Sept 6 | Sold goods to R and received a bearer cheque | 25,000 |

| Sept 15 | Rakesh’s cheque deposited into Bank | 25,000 |

| Sept 20 | Cash withdrawn for personal use | 5,000 |

| Sept 25 | Cash purchases of ₹60,000 at 10% T.D. and 5% C.D.; half in cash, remainder by cheque |

25,650 each for cash and cheque |

| Oct 2 | Received crossed cheque for dividend | 6,250 |

| Oct 5 | Cheque received from our debtor B returned dishonoured | 2,000 |

| Oct 10 | Cheque issued to our creditor E was dishonoured | 6,000 |

| Oct 16 | Directly deposited into our bank account by our debtor G | 7,500 |

| Oct 20 | The bank paid insurance premium as per our standing instruction | 1,000 |

| Oct 27 | The bank collected interest on investment in shares as per our standing instruction | 1,650 |

Dr. Cash Book Cr.

| Date | Receipts | R. No. | L. F. | Cash ₹ | Bank ₹ | Date | Payments | V. No. | L. F. | Cash ₹ | Bank ₹ |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025 | 2025 | ||||||||||

| Sept 1 | To Capital A/c (Being started business) | 80,000 | 4 | By Bank A/c (Being cash deposited) | C | 10,000 | |||||

| 4 | To Cash A/c (Being cash deposited) | C | 10,000 | 15 | By Bank A/c (Being cheque deposited into bank) | 25,000 | |||||

| 6 | To Sales A/c (Being cash sales made) | 25,000 | 20 | By Drawings A/c (Being cash withdrawn for personal use) | 5,000 | ||||||

| 15 | To Cash A/c (Being cheque deposited into bank) | C | 25,000 | 25 | By Purchases A/c (Being Cash purchases) | 25,650 | 25,650 | ||||

| 30 | By Balance c/d | 40,000 | 9,350 | ||||||||

| 1,05,000 | 35,000 | 1,05,000 | 35,000 | ||||||||

| Oct | |||||||||||

| 1 | To Balance b/d | 40,000 | 9,350 | 5 | By B A/c (Being cheque received from B dishonoured) | 2,000 | |||||

| 2 | To Dividend A/c (Being Dividend received) | 6,250 | 27 | By Insurance Premium A/c (Being insurance premium paid by bank) | 1,000 | ||||||

| 16 | To E A/c (Being cheque issued to B dishonoured) | 6,000 | 31 | By Balance c/d | 40,000 | 27,750 | |||||

| 16 | To G A/c (Being direct deposit by G) | 7,500 | |||||||||

| 27 | To Interest on Investment A/c (Being interest on investment collected by bank) | 1,650 | |||||||||

| 40,000 | 30,750 | 40,000 | 30,750 | ||||||||

| Nov 1 | To Balance b/d | 40,000 | 27,750 |

Key Takeaways

-

A two-column cash book records both cash and bank transactions together in one place, helping businesses track and balance daily receipts and payments efficiently.

- Contra entries happen when money is transferred internally between cash and bank accounts and are marked with 'C,' with both sides of the transaction recorded.

-

Key features of the two-column cash book include columns for date, particulars, voucher numbers, ledger folios, and distinct columns for cash and bank; it includes transactions like cheques, cash deposits, withdrawals, and contra entries.

-

Main contents include recording opening balances, cheque transactions (received, issued, dishonoured), direct deposits, bank charges, interest, loans, and payments on behalf of the trader.

- Types of bank accounts: current, savings, fixed deposit, recurring deposit