Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Written Down Value (WDV) Method

- Overview

- Formula

- Advantages and Disadvantages

- Real-life Example

- Comparison with Fixed Instalment Method

- Key Takeaways

Definition: Written Down Value (WDV) Method

The Written Down Value (WDV) Method is a way to calculate depreciation where a fixed percentage is charged every year on the asset’s current book value (its remaining value after previous depreciation), making the depreciation amount decrease each year as the asset’s value reduces.

Overview

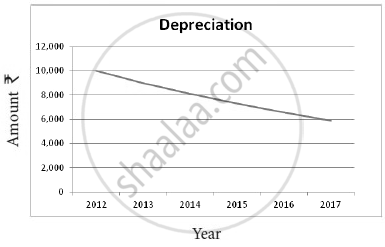

Because the depreciation amount decreases every year in the Written Down Value (WDV) Method, the graph of depreciation forms a downward sloping curve, showing less depreciation with each passing year(as shown in the below image)

This method is also known as:

-

Diminishing Balance Method

-

Reducing Balance Method

Formula

\[\text{Depreciation}=\text{Book Value at beginning of year}\times\frac{\text{Rate of Depreciation}}{100}\]

Where:

-

Book Value = Cost – Accumulated Depreciation

-

Rate of Depreciation (%) = Fixed rate used each year

Advantages and Disadvantages

Advantages

-

Reflects realistic asset use — higher depreciation in early years.

-

Equalizes total annual charge (Depreciation + Repairs).

-

Accepted by income tax authorities.

-

Reduces risk of overvaluation of older assets.

Disadvantages

-

Complicated calculation compared to SLM.

-

Asset value never becomes fully zero.

-

May not create sufficient funds for replacement without reserve planning.

Real-life Example

A company purchased machinery on 1st April 2020 for ₹1,00,000. The rate of depreciation is 10% per annum under the Written Down Value Method. Find:

-

The depreciation amount each year, and

-

The book value at the end of each year, for 4 years.

| Year | Opening Book Value (₹) | Depreciation (10%) (₹) | Closing Book Value (₹) |

|---|---|---|---|

| 1st Year | 1,00,000 | 10,000 | 90,000 |

| 2nd Year | 90,000 | 9,000 | 81,000 |

| 3rd Year | 81,000 | 8,100 | 72,900 |

| 4th Year | 72,900 | 7,290 | 65,610 |

Detailed Calculations

Step 1: In the first year, depreciation is charged on the cost of the asset.

- Depreciation = 10% of 1,00,000 = ₹10,000

- Book value at end of Year 1 = 1,00,000 − 10,000 = ₹90,000

Step 2: In the second year, depreciation is charged on the opening book value (₹90,000).

- Depreciation = 10% of 90,000 = ₹9,000

- Book value at end of Year 2 = 90,000 − 9,000 = ₹81,000

Step 3: In the third year, depreciation = 10% of 81,000 = ₹8,100

- Book value = 81,000 − 8,100 = ₹72,900

Step 4: In the fourth year, depreciation = 10% of 72,900 = ₹7,290

- Book value = 72,900 − 7,290 = ₹65,610

Comparison with Fixed Instalment Method

| Basis | Fixed Instalment Method (SLM) | Written Down Value Method (WDV) |

|---|---|---|

| Meaning | Depreciation per year stays fixed | Depreciation per year keeps reducing |

| Calculation | On the original cost of the asset | On the book value after previous years |

| Depreciation Amount | Same amount every year | Decreases year by year |

| Asset’s Value at End | Can be reduced to scrap/zero value | Never becomes zero (keeps reducing) |

| Profit Impact | Equal effect each year | Lower profits early, higher profits later |

| Recognition by Tax/Law | Not usually accepted by tax law | Accepted by tax law |

| Suitability | Furniture, buildings (steady use) | Machinery, vehicles (high initial use) |

| Depreciation Curve | Parallel to X-axis (straight line) | Slopes downward (decreasing curve) |

| Other Names | Straight Line, Original Cost Method | Diminishing, Reducing Balance Method |

Key Takeaways

-

The WDV method calculates depreciation by applying a fixed percentage to the book value of an asset at the beginning of each year.

-

The method is also called the Diminishing Balance Method or Reducing Balance Method.

-

WDV results in higher depreciation charges in the early years and lower charges in later years.

-

The graph for depreciation using WDV forms a downward-sloping curve, showing less depreciation with each passing year.

-

WDV is recognized by tax authorities like the Indian Income Tax Department.

-

This method matches the natural wear and tear of assets such as machinery, vehicles, and tools—assets that lose value faster in their initial years.

-

WDV is more complex than the Straight-Line Method, and it never reduces asset value to zero.

- Under SLM, asset value can fall to zero, and profit remains steady, whereas under WDV, depreciation and profits both decrease over time.