Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Analytical Petty Cash Book

- Comparison with Simple Petty Cash Book

- Format and Contents

- Definition: Imprest System

- Imprest System: Related Concepts

- Reasons for Using Imprest System in Analytical Petty Cash Book

- Example: Recording Transactions in Analytical Petty Cash Book

- Key Takeaways

Definition : Analytical Petty Cash Book

An Analytical Petty Cash Book is a special type of petty cash book used to record all small cash payments in separate columns for each expense category, like postage, stationery, or travel, making it easy to track exactly how much is spent on each type of petty expense

Comparison with Simple Petty Cash Book

| Feature | Simple Petty Cash Book | Analytical Petty Cash Book |

|---|---|---|

| Expense Classification | No classification—one amount column | Each type of petty expense has its own column |

| Format | Receipts on one side, payments on another | Receipts on one side, payments split into columns |

| Display of Expenses | All expenses together (no breakdown) | Postage, stationery, travel, etc., each have a column |

| Analysing Expenses | Difficult to analyse each expense, as all expenses are shown in one column | Easy to total and analyse each expense type separately |

| Best for | Small businesses or very few petty payments | Businesses with frequent or varied petty expenses |

Format and Contents

Format

| Amount Received (₹) | Cash Book Folio | Date | Particulars | Voucher No. | Total Amount ₹ | Printing & Stationery ₹ | Postage ₹ |

Carriage ₹ |

Travelling Expenses ₹ |

Miscellaneous Expenses ₹ |

Telephone Charges ₹ |

L.F. | Ledger Account ₹ |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| xx | To... | ||||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| By... | xx | xx | |||||||||||

| Total Exp | - | xxx | xx | xx | xx | xx | xx | xx | xx | ||||

| By Balance c/d | xx | ||||||||||||

| xx | xxx | ||||||||||||

| xx | To Balance b/d | ||||||||||||

| xxx | To... |

Contents:

| Column Title | Description |

|---|---|

| Amount Received | The total petty cash amount given to the petty cashier to spend for small expenses. |

| Cash Book Folio | Reference number or page from the main cash book where the transaction is recorded. |

| Date | The date on which each petty transaction (receipt or payment) occurs. |

| Particulars | Description/details about the transaction (e.g., what was purchased or paid for). |

| Voucher No. | The serial number of the supporting voucher or bill for the transaction. |

| Total Amount | The total amount paid or received in each transaction. |

| Printing & Stationery | Amount spent on items like paper, pens, photocopying, etc. |

| Postage | Amount spent on postal services such as stamps, courier, or speed post. |

| Carriage | Expenses for transporting goods, delivery, or moving packages. |

| Travelling Expenses | Money spent on transport or travel, such as bus or taxi fares. |

| Miscellaneous Expenses | Other petty expenses that don’t fit regular categories. |

| Telephone Charges | Amount paid for telephone- or mobile-related expenses. |

| L.F. | Ledger Folio: a reference to the page in the ledger where the account is posted. |

| Ledger Account | Amount posted to the specific ledger account; keeps track of final balances/records. |

Definition : Imprest System

The imprest system is an accounting method where a fixed amount of money is set aside in a petty cash fund to pay for small, routine expenses. The fund is regularly replenished so that it always returns to its original set amount after expenses are checked and recorded, making this system easy to monitor and control.

Imprest System : Related Concepts

| Concept | Explanation |

|---|---|

| Petty Cash Fund | A small reserve of money kept on hand for minor, everyday expenditures (like postage, transport, and refreshments). |

| Custodian (Petty Cashier) | The person responsible for managing the fund and collecting supporting receipts for each payment. |

| Replenishment | At the end of each period (week/month), used cash is restored up to the fixed imprest amount, based on receipts/vouchers submitted. |

| Receipts/Vouchers | Proof of all payments made from petty cash,is needed for controlling and replenishing the fund. |

| Monitoring and Control | Regular checking of actual cash versus recorded cash prevents misuse or errors and increases accuracy in petty cash handling. |

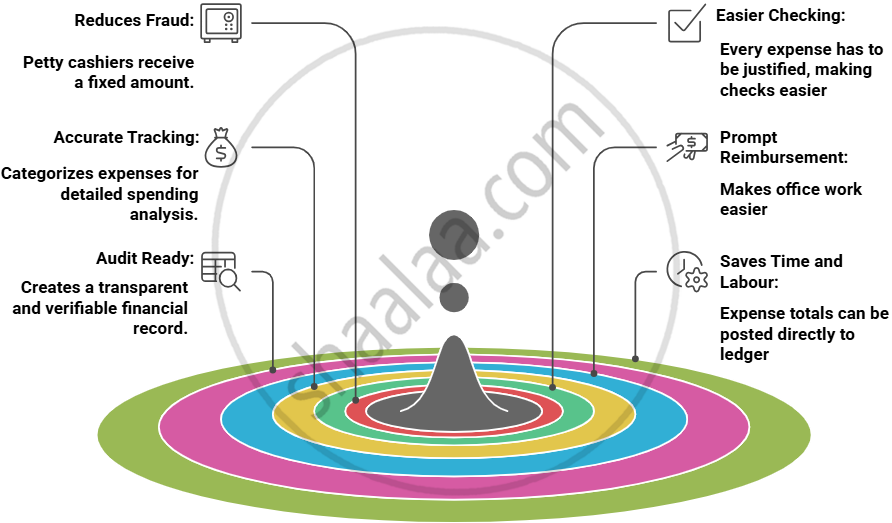

Reasons for Using Imprest System in Analytical Petty Cash Book

Example : Recording Transactions in Analytical Petty Cash Book

S, the petty cashier, received ₹2,000 from the head cashier.

List of transactions to be recorded in the analytical petty cash book of PQR Traders for April 2025.

| Date | Particulars | Amount (₹) |

|---|---|---|

| 01-Apr-25 | Paid Cartage | 50 |

| 02-Apr-25 | Telephone Charges | 40 |

| 03-Apr-25 | Bus Fare | 20 |

| 04-Apr-25 | Postage | 30 |

| 05-Apr-25 | Snacks for Employees | 80 |

| 06-Apr-25 | Courier Charges | 30 |

| 07-Apr-25 | Purchased Stationery | 65 |

| 08-Apr-25 | Xerox Charges | 30 |

| 09-Apr-25 | Repairs on Furniture | 105 |

| 10-Apr-25 | Cleaning Expenses | 115 |

In the books of PQR Traders

Analytical Petty Cash Book

| Amount Received ₹ | Date | Particulars | Voucher No. | Total Amount Paid ₹ | Courier/Postage ₹ | Telephone Expenses ₹ | Travelling & Conveyance Expenses ₹ | Printing & Stationery ₹ | Misce. Expenses ₹ | L.F. | Ledger |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2,000 | 2025 April 01 | To Cash A/c | - | ||||||||

| 01 | By Cartage | - | 50 | 50 | |||||||

| 02 | By Telephone Charges | - | 40 | 40 | |||||||

| 03 | By Bus Fare | - | 20 | 20 | |||||||

| 04 | By Postage | - | 30 | 30 | |||||||

| 05 | By Refreshment to Employees | - | 80 | 80 | |||||||

| 06 | By Courier Charges | - | 30 | 30 | |||||||

| 07 | By Stationery | - | 65 | 65 | |||||||

| 08 | By Xerox charges | - | 30 | 30 | |||||||

| 09 | By Furniture repairs | - | 105 | 105 | |||||||

| 10 | By Cleaning Expenses | 115 | 115 | ||||||||

| Total Exp | - | 565 | 60 | 40 | 70 | 95 | 300 | ||||

| 30 | By Balance c/d | - | 1,435 | ||||||||

| 2,000 | 2,000 | ||||||||||

| 1,435 | May 01 | To Balance b/d | 1,435 |

Key Takeaways

- The analytical petty cash book is a type of petty cash book that records small cash payments in separate columns for each expense category (postage, stationery, travel, etc.), providing clear analysis and better control.

- The system saves time by allowing totals for each expense type to be posted directly to ledgers rather than entering each payment separately.

- Common analytical columns found in the petty cash book include Printing & Stationery, Postage, Travelling Expenses, Telephone Charges, and Miscellaneous Expenses.

- The imprest system involves giving the petty cashier a fixed amount at the start of each period; after checking receipts, only the amount spent is reimbursed, restoring the balance to the original level.

- Using the imprest system in the analytical petty cash book ensures transparency, accuracy, convenience, and strict financial discipline in managing frequent, small transactions.