Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Transaction

- Types of Transactions

- Chart Showing Types

- Related Accounting Terms

- Chart Showing Related Accounting Terms

- Real-Life Examples

Maharashtra State Board: Class 11

Definition: Transaction

A transaction is when two people or parties exchange goods or services for money or something worth money.

Maharashtra State Board: Class 11

Types of Transactions

A. Monetary Transactions

These involve money (directly or indirectly) and are recorded in account books.

-

Cash Transactions: Money is paid or received on the spot.

-

Credit Transactions: Money is paid or received at a later date.

B. Non-Monetary Transactions (Barter)

-

No money involved! Things are exchanged with other things.

-

Not recorded in account books.

Maharashtra State Board: Class 11

Chart Showing Types

Maharashtra State Board: Class 11

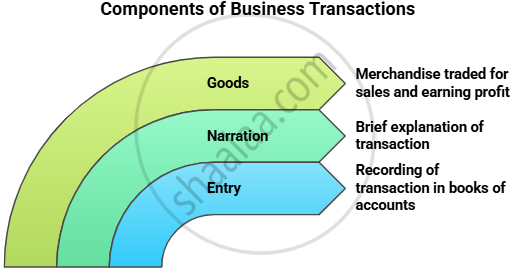

Related Accounting Terms

| Term | What it Means |

|---|---|

| Entry | Recording a transaction in the books |

| Narration | Short explanation below an entry (starts “Being...”) |

| Goods | Items a business buys and sells for profit |

Maharashtra State Board: Class 11

Chart Showing Related Accounting Terms

Maharashtra State Board: Class 11

Real-Life Examples

| Point/Concept | Example |

|---|---|

| Transaction | Buying goods from a supplier for ₹15,000 in cash |

| Cash Transaction | Paying salary of ₹5,000 to an employee (payment made at the time of transaction) |

| Credit Transaction | Selling goods to Aman on credit for ₹8,000 (payment received later) |

| Non-Monetary (Barter) Transaction | Exchanging wheat for rice (direct swap, no cash involved) |

| Entry | Writing a journal entry for 'Salary Paid' in the accounts |

| Narration | (Being rent paid in cash for May) written below the entry for "Rent Paid" |

| Goods | Medicines for a chemist, vegetables for a vegetable vendor, and cars for a car dealer |