Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Definition: Accounting Standards

- International Financial Reporting Standards (IFRS)

- Examples of IFRS

- Accounting Standards in India

- How Accounting Standards in India Are Made

- AS vs. Ind AS vs. IFRS

- Explanation of Certain AS

- Examples of Accounting Standards in India

- Key Takeaways

Introduction

1. What Are Accounting Standards (AS)?

They are detailed written rules issued by an official authority that tell businesses exactly how they should record, measure, and report different kinds of business transactions in their financial statements. These rules remove confusion by telling every company to prepare their accounts in the same, standardized way.

2. How are AS Different from Accounting Principles?

-

Accounting Principles are broad, general guidelines (like “be honest”, “record everything,” “match costs with revenues”).

-

Accounting Standards (AS) are specific, detailed instructions (like “for inventories, value at the lower of cost and net realizable value”).

3. Why Do We Need Accounting Standards?

-

They make financial statements simpler and easier to understand.

-

All accountants use the same methods.

-

They let us compare results from different companies fairly.

-

They make the accounts more trustworthy.

-

They help businesses follow the law.

4. Who Issues Accounting Standards?

Globally (World Level):

-

The main group that creates global accounting standards is the International Accounting Standards Board (IASB).

-

IASB is part of the IFRS Foundation (a non-profit organization).

-

IASB develops the International Financial Reporting Standards (IFRS), used by most countries worldwide.

-

The goal is to make accounts easy to compare and understand in any country.

In Each Country:

-

Each country usually has its own official accounting body or government authority that makes national accounting standards.

-

These local boards may follow global standards or create their own, sometimes mixing both.

Definition: Accounting Standards

In the words of Kohler: “Accounting standards are codes of conduct imposed by customs, laws or professional bodies for the benefit of public accountants and accountants generally.”

International Financial Reporting Standards (IFRS)

These are rules made by an international group so businesses around the world report their financial numbers in the same way. This makes it easy for people and companies in any country to understand and compare accounts.

Examples of IFRS

|

IFRS Number & Name |

What It Means/Includes |

Real-Life Example |

|---|---|---|

|

IFRS 1 First-time Adoption |

Rules for companies using IFRS for the very first time |

A company in India moves from Indian AS to IFRS for its reporting |

|

IFRS 2 Share-based Payment |

How to record giving shares to employees as part of their salary |

A company rewards workers with company shares in addition to pay |

|

IFRS 3 Business Combinations |

How to show accounts when two companies merge or one buys another |

Facebook buying Instagram—their numbers are combined using IFRS 3 |

|

IFRS 5 Assets Held for Sale |

What to do if a company plans to sell a big asset or business segment |

A car company decides to sell one of its factories |

Accounting Standards in India

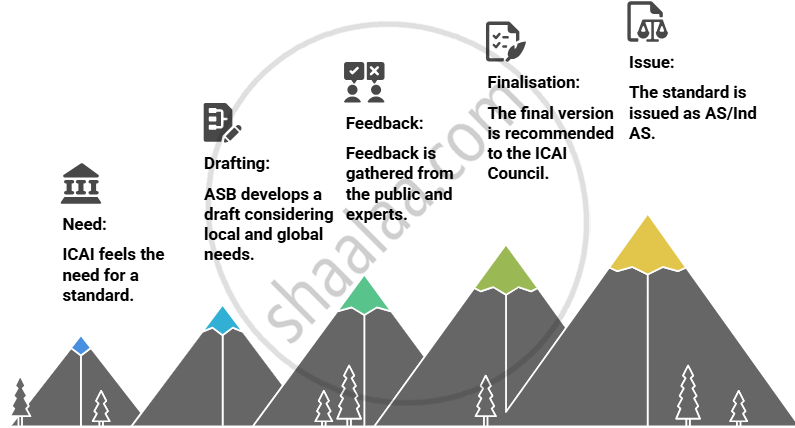

In India, the rules for preparing accounts (Accounting Standards) are made by the Institute of Chartered Accountants of India (ICAI). A special group in ICAI, called the ASB, writes these standards after thinking about Indian laws and international best practices.

As business becomes global, Indian companies need to prepare accounts that look similar to those in other countries. So, India created Ind AS, which are Indian versions of IFRS adjusted to Indian conditions. Big companies use Ind AS, while small ones can still follow older standards. In the future, all will use Ind AS.

How Accounting Standards in India Are Made

AS vs. Ind AS vs. IFRS

|

Feature/Point |

AS (Accounting Standards) |

Ind AS (Indian Accounting Standards) |

IFRS (International Financial Reporting Standards) |

|---|---|---|---|

|

What are they? |

Old Indian rules (standards) for accounts |

Updated Indian standards, based on global IFRS |

Worldwide rules for preparing accounts |

|

Who makes them? |

ICAI (India) |

ICAI (India), matching IFRS with tweaks |

IASB (Global organization) |

|

Where are they used? |

Small Indian companies |

Large & listed Indian companies |

Most companies worldwide (except USA, a few others) |

|

Based on |

Indian laws and needs |

IFRS + Indian adjustments |

International/global business practices |

|

Complexity |

Simpler, cover basics |

More detailed, cover modern cases |

Most detailed, cover all modern business types |

|

Key Areas |

Limited topics, less on group accounts or new financial products |

Include group companies, leases, modern contracts |

All latest accounting topics (leases, groups, etc.) |

|

Why are they important? |

Meet Indian legal needs |

Help Indian companies match global standards |

Standardize financial info worldwide |

Explanation of Certain AS

|

AS No. |

Name |

What It Says |

|---|---|---|

|

AS-1 |

Disclosure of Accounting Policies |

Clearly state which methods or rules you used in your accounts in one place |

|

AS-2 |

Valuation of Inventories |

Show your inventories (goods) at the lower of cost or possible sale price |

|

AS-3 |

Cash Flow Statements |

Prepare a statement showing all money coming in and going out,during an accounting period |

|

AS-6 |

Depreciation Accounting |

Spread the cost of an asset over the years you use it |

|

AS-8 |

Research & Development |

Count research & development spending as an expense of the accounting period in which you spend it |

|

AS-9 |

Revenue Recognition |

When and how to show “revenue” |

|

AS-10 |

Accounting for Fixed Assets |

Include all costs incurred to make an asset ready to use,in the cost of an asset, and remove asset from books of accounts when sold or no benefit is expected from it |

|

AS-12 |

Accounting for Government Grants |

Only show government grant money as income if you’re sure that the company will follow the conditions attached to that grant. |

|

AS-13 |

Accounting for Investments |

Show short-term and long-term investments separately in accounts |

AS 22 — Accounting for Taxes on Income

What Is It About?

AS 22 tells businesses how to handle the fact that profits shown in their accounts (notebooks) are often different from the profits on which they have to pay tax (as per the government’s tax rules). This difference leads to two things:

-

Current Tax: The tax you pay right now, based on taxable income this year.

-

Deferred Tax: Tax you will either pay or save in the future, due to temporary differences between your accounts and the government's calculation.

AS 22 is all about making sure your accounts show not just the tax you paid now (current tax), but also any tax you will have to pay (or get back) later because your profits for accounts and for the tax bill don’t match this year—so you don’t get a shock in the future!

Examples of Accounting Standards in India

|

Topic |

Related Ind AS |

Related |

Example |

Key Difference: Ind AS vs AS |

|---|---|---|---|---|

|

Revenue |

Ind AS 115: Revenue from Contracts |

AS 9: Revenue Recognition |

When a telecom company provides yearly service—how to show income |

Ind AS 115 is more detailed and covers complex contracts |

|

Inventories |

Ind AS 2: Inventories |

AS 2: Valuation of Inventories |

A store valuing goods at year-end |

Ind AS is stricter about costs included |

|

Leases (Rentals) |

Ind AS 116: Leases |

(No direct AS; was partly in AS 19) |

Pizza Hut must record rented shops as assets |

Ind AS 116 requires showing leases on balance sheet |

|

Fixed Assets |

Ind AS 16: Property, Plant & Equipment |

AS 10: Accounting for Fixed Assets |

Showing a factory’s machines in books |

Ind AS includes more assets, improved depreciation |

Key Takeaways

-

Accounting Standards (AS) in general:

Give a set of clear rules so every company records and reports its financial data in the same way. This makes financial statements easy to understand, compare, and trust.

-

AS (Accounting Standards – India):

Are official rules set by Indian authorities (ICAI) that cover how to treat different items like stock, sales, or assets in your accounts.

-

IFRS (International Financial Reporting Standards):

Are worldwide rules for preparing accounts so financial information is understood and accepted globally. This helps investors and businesses compare companies from different countries easily.

-

Ind AS (Indian Accounting Standards):

Are updated Indian standards—almost the same as IFRS but adapted to Indian conditions. Used by only large Indian companies as of now and soon by all Indian companies.