Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Definition: Double Entry System

- Principles

- Elements

- Advantages

- Real-life Examples

Maharashtra State Board: Class 11

Introduction

- The Double Entry System is the most logical and scientific way to record business transactions.

- Every transaction has two sides:

-

- One account receives value (Debit)

- One account gives value (Credit)

Origin & Fun Fact

- Developed by Luca D. Bargo Pacioli, an Italian merchant, in 1494.

- 10th November is celebrated as International Accounting Day in his honour.

Maharashtra State Board: Class 11

Definition : Double Entry System

“Every business transaction has a twofold effect in that it affects two accounts in opposite directions and if a complete record is to be made of each such transaction, it would be necessary to debit one account and credit another account. It is this recording of the twofold effect of every transaction that has given rise to the term Double Entry.”– J.R. Batliboi.

Maharashtra State Board: Class 11

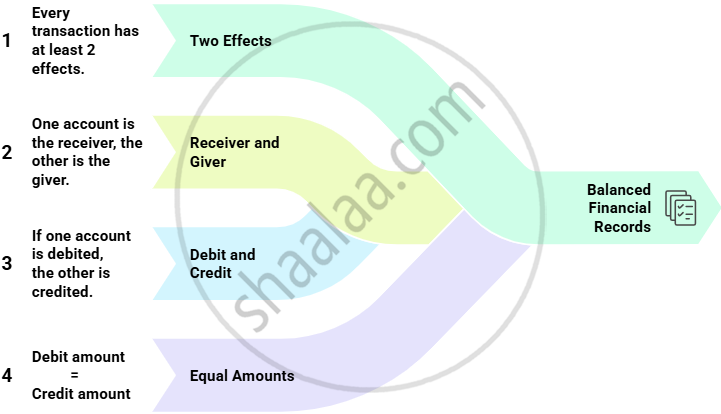

Principles

Maharashtra State Board: Class 11

Elements

| Element | Meaning/Role |

|---|---|

| 1. Dual Effect | Every transaction affects at least two accounts: one debit and one credit. This maintains the accounting equation (Assets = Liabilities + Equity) and ensures balance in the books. |

| 2. Journal | The primary book of entries where all transactions are recorded chronologically, showing which accounts are debited and credited. Each entry always involves at least two accounts and lists the amounts, debits first, followed by credits. |

| 3. Ledger | Contains classified accounts (Cash, Sales, Purchases, etc.). Each journal entry is posted (“transferred”) to the appropriate account in the ledger. It enables tracking balances of individual accounts. |

| 4. Balancing Ledger Accounts | At regular intervals, all debits and credits in each ledger account are totaled. The difference is put as either balance c/d (carried down) or b/d (brought down). This process ensures each account shows an up-to-date balance and aids accuracy. |

| 5. Trial Balance | A statement listing all ledger balances as of a specific date. All debit and credit totals should match, serving as a checkpoint for mathematical accuracy and as the foundation for preparing final accounts. |

| 6. Final Accounts | The last step of the accounting process. These include the Trading Account, Profit & Loss Account (to find profit or loss), and the Balance Sheet (showing financial position as of a date). They provide insight into profitability and financial health. |

Maharashtra State Board: Class 11

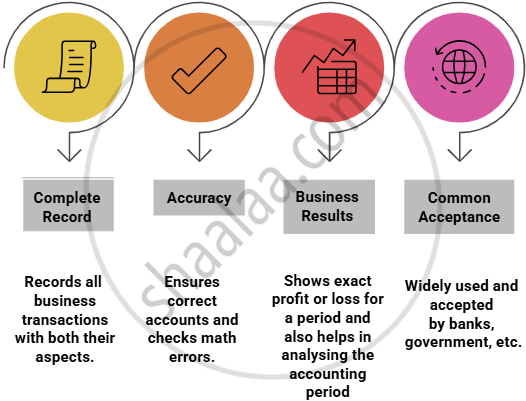

Advantages

Maharashtra State Board: Class 11

Real-life Examples

-

Double Entry System works like a seesaw – when one side goes up, the other goes down by the same amount.

-

For example, you pay ₹499 via Google Pay for a Netflix subscription:

Debit: Subscription Expense (expense ↑)

Credit: Bank Account (asset ↓)