Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Tax Invoice

- Importance of Tax Invoice, with Examples

- Types of Tax Invoices with Examples

- Details in a Tax Invoice

- Key Takeaways

Notes

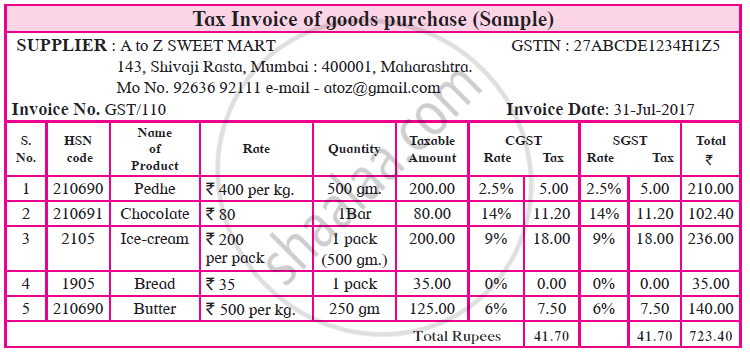

Ved : In the invoice we see some new words, please explain them.

Teacher : CGST and SGST are two components of GST. CGST is Central Goods and Service Tax which is to be paid to the central government. Whereas SGST is State Goods and Service Tax which is to be paid to the state government.

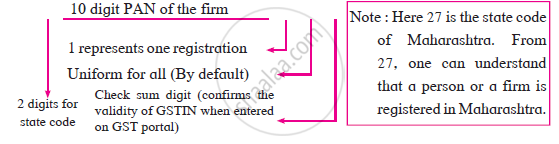

Ria : What is in the right most corner with a long queue of numbers and alphabets?

Teacher : It is GSTIN, dealer’s indentification number. (GSTIN- Goods and Service Tax Identification Number). GSTIN is mandatory for the dealer whose annual turn over in previous financial year exceeds rupees 20 lacs. You know that PAN has 10 alpha-numerals, similarly GSTIN has 15 alphanumerals. It includes 10 digit PAN of the dealer.

e.g. : 27 A B C D E 1 2 3 4 H 1 Z 5

Jennie : There is a word HSN code in the tax invoice.

Teacher : All Goods are classified by giving numerical code called HSN code. It is to be quoted in the tax invoice. Full form of HSN is Harmonized System of Nomenclature.

Joseph : As usual there is name of the shop, address, state, date, invoice number, mobile number and e-mail ID also in the tax invoice.

Teacher : Now we will see how the GST is charged for each product (Goods) in the bill. Observe the given bill and fill in the boxes with the appropriate number. Price of 1 kg of Pedhe is 400, therefore cost of 500 gm. of Pedhe is 200.

- CGST at the rate of 2.5% is Rs. _____and SGST at the rate of ______% is Rs. 5.00.

- It means that the rate of GST on Pedhe is 2.5+2.5=5% and hence the total GST is Rs.10.

- The rate of GST on chocolate is % and hence the total GST is____Rs.

- Rate of GST on Ice-cream is %, hence the total cost of ice-cream is_____

- On butter CGST rate is % and SGST rate is also %. So GST rate on butter is ____%.

Aditya : Rate of GST on bread is 0 %. The rate of CGST and SGST is same for each product.

Ninad : Rates of GST are different for diferent products such as 0%, 5%, 12%, 18% and 28%.

Teacher : These rates are fixed and prescribed by the government. Now let us observe the tax invoice of services provided. Fill in the blanks with the help of given information.

Definition : Tax Invoice

In India, a tax invoice is an official bill the seller gives to the buyer when selling goods or services taxable under GST.

Importance of Tax Invoice,with Examples

| Point of Importance | Explanation | Example |

|---|---|---|

| Legal Compliance | Businesses must issue tax invoices to comply with GST rules. | A Mumbai electronics shop issues a GST invoice to avoid government penalties during an audit. |

| Claiming Input Tax Credit (ITC) | A tax invoice lets buyers get credit for GST paid on purchases. ITC = GST collected through sales - GST paid on purchases |

A marketing agency in Delhi claims ITC on ₹18,000 GST shown in vendor invoices for office supplies. |

| Proof of Transaction | Acts as legal evidence of a sale/purchase between parties. | A Kolkata wholesaler uses a tax invoice to prove the sale of goods if a customer disputes delivery. |

| Accurate Tax Reporting | Required to show collected GST and file correct tax returns. | A Jaipur retailer files monthly GST returns, using tax invoices to accurately report all sales. |

| Payment Tracking | Helps sellers keep records of what was sold and track pending dues. | A grocery business in Chennai checks invoice records to follow up on a customer’s overdue payment. |

| Dispute Resolution | Helps settle disagreements using detailed transaction data. | A trader in Bangalore refers to invoice details to resolve a dispute about wrong quantities delivered. |

| Builds Trust & Reputation | Shows professionalism and transparency, encouraging repeat business. | An IT firm in Pune builds lasting client relationships by issuing clear GST-compliant invoices. |

Types of Tax Invoices with Examples

| Type of Tax Invoice | Explanation | Example |

|---|---|---|

| Full Tax Invoice | The standard invoice is issued for all taxable sales and includes detailed information required by GST law. | A manufacturer sells machines to a distributor and provides an invoice listing items, prices, and GST. |

| Simplified Tax Invoice | A condensed invoice for smaller transactions (often below ₹200); it contains only basic details. | A coffee shop gives a retail customer a bill showing the total, tax, and item description for a coffee. |

| Electronic Tax Invoice | A tax invoice is issued and received electronically (e-invoicing is mandatory for large businesses). | An online electronics store emails a GST-compliant invoice to a buyer for a laptop purchase. |

| Bill of Supply | Used when selling exempted goods/services or by composition scheme taxpayers—no tax charged. | A handloom artisan (under the composition scheme) selling fabric issues a bill of supply, not a tax invoice |

| Credit Note | Issued if extra charges are applied in the original tax invoice or when goods are returned. | A textile shop refunds GST after a customer returns defective shirts, issuing a credit note. |

| Debit Note | Issued when the original invoice understated the tax or value of goods/services supplied. | After a price revision, a dealer issues a debit note for additional GST on a previous supply. |

| Consolidated Tax Invoice | A single invoice for multiple small transactions (≤ ₹200 each) issued to unregistered buyers. | A stationery store merges all uninvoiced sales of the day into one consolidated invoice. |

- What is the composition scheme under GST?

The GST Composition Scheme is a tax option for small businesses in India, where those with sales up to ₹1.5 crore can pay GST at a fixed lower rate and do much less paperwork. Businesses using this scheme cannot charge GST on their bills—they must use a simple “bill of supply” instead of a regular tax invoice. - Debit notes and credit notes are both voucher types in accounting and are also recognized as special tax invoice types under GST in India.

As Voucher Types:

- Debit Note: Used when goods are returned to a supplier or when the taxable value/tax on an invoice is less than what should be paid—issued by the buyer in accounting but by the supplier under GST for corrections.

- Credit Note: Used to reduce the amount payable by the buyer due to goods returned, overcharging, or corrections—issued by the seller, both in business accounts and under GST.

As Tax Invoice Types:

- Debit Note: Issued by a supplier to increase the taxable value or GST charged on a previously issued tax invoice. It legally amends the original tax invoice upward.

- Credit Note: Issued by a supplier to decrease the taxable value or GST amount of an original tax invoice due to returns, overcharges, or after-sale discounts.

Both must reference the original tax invoice and be reported in GST returns.

Details in a Tax Invoice

| Invoice Type | Basic (Common) Details | Additional (Type-Specific) Details |

|---|---|---|

| Full Tax Invoice | Invoice no. & date, seller & buyer name/address/GSTIN, item/service description, quantity/unit, HSN/SAC code, price, total/taxable value, GST rate/amount, signature, place of supply | For B2B, the buyer’s GSTIN is mandatory. For ≥₹50,000 to an unregistered buyer, the buyer’s name, address, delivery address, state & code are needed. |

| Simplified Tax Invoice | Same as above, but fewer fields:can often omit buyer details; only total value and summary GST breakdown required | Used for B2C supplies ≤ ₹200 per transaction, most customer fields can be omitted. |

| Bill of Supply | Seller & buyer info, item/service description, quantity/unit, HSN/SAC, value, signature, date | No GST rate or amount displayed (since for exempt/composition dealers); must state “composition/exempt” if applicable |

| Consolidated Tax Invoice | Summarizes multiple small sales: seller info, sale dates, product summary, total value, minimal buyer info | For multiple B2C unregistered sales ≤ ₹200 each, issued at day's end with transaction summary |

| E-invoice | Same as full tax invoice + electronic IRN, digital signature, QR code, GSTN acknowledgment | Generated and verified online via GSTN for large businesses |

| Credit Note | Seller & buyer info, reference to original invoice, date, product/service details, GST if applicable, value, signature | Clarifies reason for issuing (return, overcharge, discount), original invoice reference, and tax credit reversal |

| Debit Note | Seller & buyer info, reference to original invoice, date, product/service details, GST if applicable, value, signature | Explains the reason for the extra charge (underbilling, extra supplies); must give reference to the original invoice. |

Important Points:

- B2B stands for Business to Business and refers to a sale made by one GST-registered business to another GST-registered business; the buyer must have a GSTIN and can claim input tax credit.

- B2C stands for Business to Consumer and refers to a sale made by a registered business to an unregistered end consumer (ordinary customer); no GSTIN is required for the buyer.

- IRN stands for Invoice Reference Number and refers to a unique number generated for each e-invoice by the GST portal, which verifies and tracks electronic tax invoices for compliance

- GSTIN stands for Goods and Services Tax Identification Number—a unique 15-digit code assigned to every GST-registered business or taxpayer in India, used to identify them for all GST-related compliance and transactions.

Key Takeaways

- A tax invoice is a legal GST document listing sold goods/services, price, and tax.

- It is required for all taxable sales in India and must follow GST rules.

- Key types: tax invoice, bill of supply, simplified invoice, consolidated invoice, credit/debit note, and e-invoice.

- Common details: seller/buyer info, invoice number/date, item details, HSN/SAC code, price, tax rate and amount, total, and signature.

- Some invoices need extra details, like delivery addresses for large sales, transport info, or special formats for composition dealers.

- Importance: Needed for Input Tax Credit (ITC), legal proof, GST reporting, payment tracking, building trust, and solving disputes.

- Always issue or collect a proper tax invoice for GST credit and legal compliance.