Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Features

- Disadvantages

- Conventional System vs. Double‑Entry System

- Real-life Example

- Key Takeaways

Maharashtra State Board: Class 11

Introduction

-

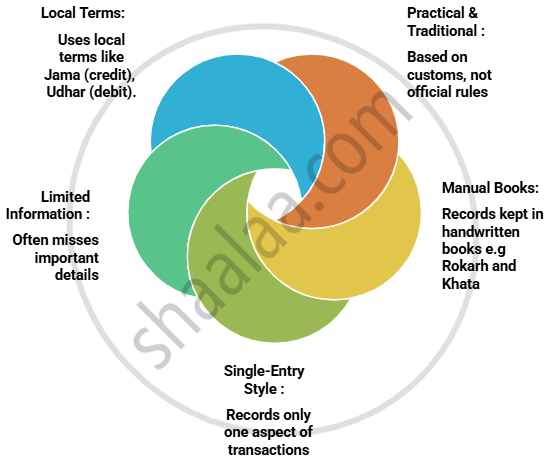

What's it? A simple, old method of keeping business records.

-

Based on accounting conventions (practical rules followed for a long time by common agreement.)

-

Common in small shops and traders before modern accounting became common.

Maharashtra State Board: Class 11

Features

Maharashtra State Board: Class 11

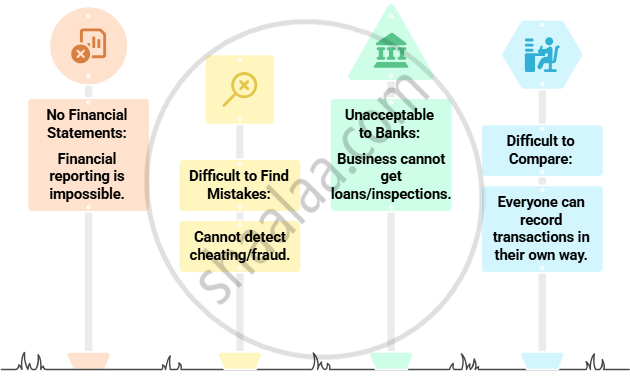

Disadvantages

Maharashtra State Board: Class 11

Conventional System vs. Double‑Entry System

| Feature | Conventional System | Double‑Entry System |

|---|---|---|

| Basis of Recording | Practical customs | Accounting principles |

| Aspects in a Transaction | Single or partial | Always two (debit & credit) |

| Types of Accounts Covered | Cash, personal only | All (personal, real, nominal) |

| Financial Statements | Not possible | Easily prepared |

| Error Detection | Hard | Possible via trial balance |

| Users | Small traders | All organisations |

Maharashtra State Board: Class 11

Real-life Example

A kirana (grocery) shop owner writes in a notebook:

-

"Received ₹1,000 cash from sales"

-

But doesn’t record:

-

Which items were sold

-

How much stock reduced

-

Who the customer was

-

Result → Knows how much cash he has, but not the full profit made or stock left.

Maharashtra State Board: Class 11

Key Takeaways

-

The Conventional Accounting System is simple but incomplete.

-

Follows conventions (practical rules) rather than strict concepts.

-

Replaced by Double‑Entry System in all formal businesses.