Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Definitions : Book-keeping

- Features

- Objectives

- Importance

- Utility

- Process

- Real-Life Example

- Key Takeaways

Introduction

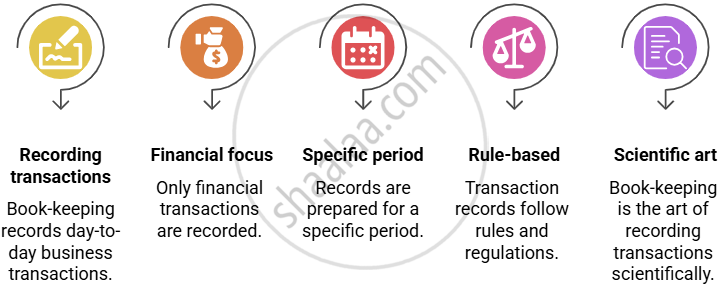

Book-keeping means carefully writing down every business money transaction, in order, every day. Think of it as a detailed “money diary” for the business.

Whenever money comes in (like sales) or goes out (like buying goods), it goes in the books immediately. This helps the business easily track its profit, loss, and financial health at any time.

Definitions: Book-keeping

- Richard E. Strahelm: “The art of analyzing and recording business transactions, reporting results of business operations through periodic statements and interpreting such results for purposes of effective control of future operations.”

- J. R. Batliboi : “Book-keeping is the art of recording business dealings in a set of books.”

- Nocth Cott : “Book-keeping is the art of recording in the books of accounts the monetary aspects of commercial or financial transactions.”

- R.N. Carter : “Book-keeping is the science and art of correctly recording in the books of accounts,all those business transactions that result in the transfer of money or money’s worth.”

Features

Objectives

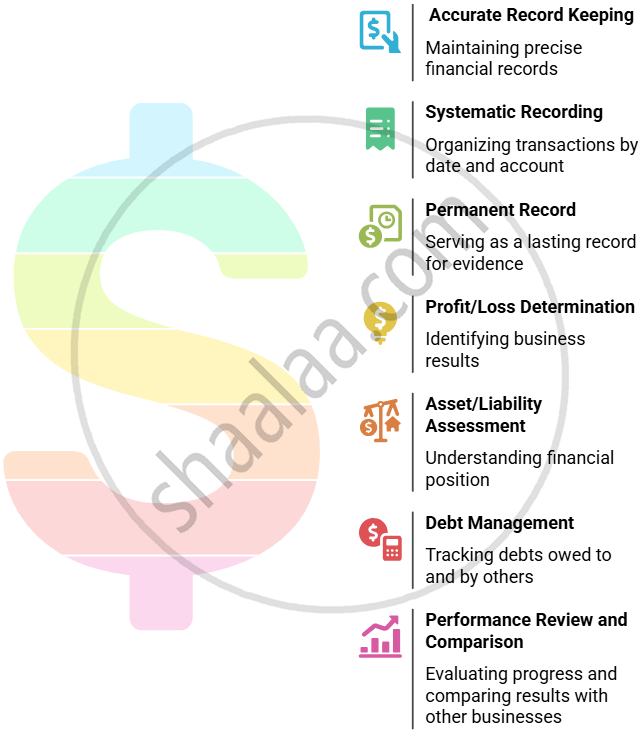

Importance

| Point | Meaning |

|---|---|

| Record | Helps keep a permanent and organized record of all money transactions so you don’t have to remember them. |

| Financial Information | Gives details about profits, losses, assets, debts, investments, and stock anytime. |

| Decision-Making | Provides useful money-related data to help owners make good business decisions. |

| Controlling | Helps business managers keep track of activities and control business operations effectively. |

| Evidence | Acts as proof in court if there’s a business dispute. |

| Tax Liability | Helps in calculating and paying correct taxes like Income Tax, Property Tax, GST, etc. |

Utility

| User | How Book-keeping Helps Them |

|---|---|

| Owner | Can easily know the profit, loss, assets, and debts of the business anytime. |

| Management | Helps in planning, decision-making, and controlling business activities. |

| Investors | Helps them decide whether to invest in the business or not. |

| Customers | Can understand the company’s financial health and feel assured about the regular supply of goods. |

| Government | Can find out and collect the correct amount of taxes. |

| Lenders | Can check the business’s ability to repay before giving loans. |

| Development | Helps businesses grow and expand through proper financial tracking. |

Process

Business Transaction Happens

↓

Recorded in Journal (day-by-day)

↓

Posted to Ledger Accounts (grouped by type)

↓

Trial Balance Prepared (checking totals)

↓

Financial Statements Made (Profit & Loss, Balance Sheet)

Real-life Example

A small business sells cupcakes:

-

July 1: Sells cupcakes for ₹1,500 (Money in)

-

July 2: Buys ingredients for ₹400 (Money out)

-

July 3: Pays for electricity ₹100 (Money out)

The owner writes each transaction in a cashbook. At the end of the week, she can see if she’s made a profit and prepare for taxes.

Key Takeaways

-

Book-keeping = Writing down all business money transactions every day.

-

Keeps business organized, helps with decision-making and taxes.

-

Used by owners, managers, government, and more.

-

Makes finding mistakes and tracking performance much easier.