Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Purchase Return Book

- Definition: Debit Note

- Purchase Return Book: Format and Contents

- Sample Debit Note, with Contents

- Definition: Credit Note

- Process of Purchase Return

- Debit and Credit Notes: Names Explained

- Example: Recording Transactions in Purchase Return Book

- Key Takeaways

Definition : Purchase Return Book

A purchase return book is a special accounting book where a business records goods sent back to suppliers because they are the wrong quality, damaged, or not needed—only returns from credit purchases are included.

Definition : Debit Note

A debit note is a brief statement prepared by the buyer when returning goods, showing the details and amount of goods returned, and letting the supplier know to reduce the buyer’s amount owed.

Purchase Return Book : Format and Contents

Format:

| Date | Name of Supplier | Debit Note No. | L.F. | Amount (₹) |

|---|---|---|---|---|

Explanation of Columns:

-

Date: This column records the date on which goods are returned to the supplier. It helps track when each transaction happened.

-

Name of Supplier:This column lists the supplier to whom the goods are returned. It helps identify which supplier’s account is affected by the return.

-

Debit Note No.: This column is for the reference number of the debit note issued to the supplier.

-

L.F. (Ledger Folio): This is the page number or code of the ledger where the supplier’s account can be found. It helps cross-reference entries for accuracy.

-

Amount (₹): This column shows the value (in rupees) of the goods returned in each transaction.

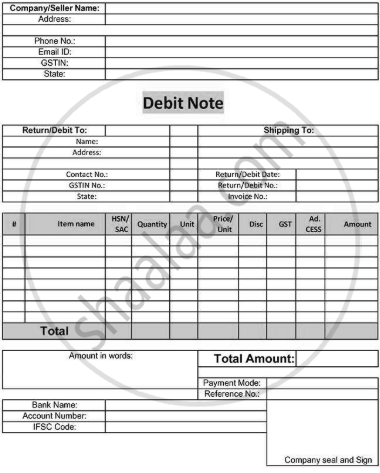

Sample Debit Note,with Contents

Explanation of Contents

Top Section: Seller/Company Details

-

Company/Seller Name, Address, Phone No., Email ID, GSTIN, State:

Identifies the issuer of the debit note—usually the buyer returning goods. These details provide necessary legal and contact information.

Debit Note Title

-

Clearly labels the document as a "Debit Note" for clarity and legal validity.

Return/Debit To & Shipping To

-

Return/Debit To:

Details of the supplier/vendor to whom goods are returned (name, address, contact, GSTIN, state). -

Shipping To:

Address details of where the goods are actually being shipped if different from the supplier’s address.

Transaction Details

-

Return/Debit Date and Invoice No., Invoice Date:

Keeps record of the associated transaction (when the goods were bought and when they are being returned).

Main Table (Itemized Details)

-

Serial number for easy reference.

-

Item Name: Product name returned.

-

HSN/SAC: Harmonized System Nomenclature/Services Accounting Code for goods or services.

-

Quantity/Unit/Price per Unit:How many items, in what units, and their price.

-

Disc: Any discount applied.

-

GST, Ad. CESS: Tax columns as required by GST rules.

-

Amount: The total (per item or per line).

Totals

-

Total: The sum of all amounts for returned items.

Bottom Section

-

Amount in words/Total Amount:

Prevents errors and fraud. -

Payment Mode/Reference No.:

If any payment or adjustment needs to be tracked. -

Bank Details:

Bank name, account number, and IFSC code for payment processing or records. -

Company Seal and Sign:

For authenticity and verification.

Definition : Credit Note

A credit note is a document given by a seller to a buyer when goods are returned, showing the amount to reduce or cancel what the buyer has to pay; it acts like a “refund slip” that adjusts the buyer’s account and proves the return happened.

Sample Credit Note,with Contents

Explanation of Contents

Top Section: Company/Seller Details

-

Company/Seller Name, Address, Phone No, Email ID, GSTIN, State:

Identifies who is issuing the note (usually the seller). These details establish legality and enable contact or verification for tax purposes.

Return/Credit From & Shipping From

-

Return/Credit From:

Lists details of the party returning goods (name, address, contact no., GSTIN, state). Useful for identifying the sender. -

Shipping From:

Adds shipping details if the location is different from the party's address.

Document Details

-

Return/Credit Date, Return/Credit No., Invoice No.:

These fields help track the transaction date, the unique number assigned to this debit/credit note, and the invoice related to the transaction. This ensures easy reference and auditing.

Main Table (Item Details)

| # | Item Name | HSN/SAC | Quantity | Unit | Price/Unit | Disc | GST | Ad. CESS | Amount |

|---|

-

** Serial number for organization.

-

Item Name: Name of the returned or credited product.

-

HSN/SAC: Standard product/service code for tax purposes.

-

Quantity, Unit, Price/Unit: Specifies number, unit type, and product price.

-

Disc: Any discounts applied.

-

GST, Ad. CESS: Tax information relevant under GST regime.

-

Amount: Final amount for each line item.

Financial Summary Section

-

TOTAL: Total amount for all items, before tax/discounts.

-

Amount in Words: Total amount written out, reduces error/fraud.

-

TOTAL AMOUNT: Grand total including all adjustments.

Payment & Banking Details

-

Payment Mode, Reference Number:

Method and confirmation of payment, useful for recordkeeping. -

Bank Name, Account Number, IFSC Code:

For facilitating or confirming electronic payments, or for refunds.

Authentication

-

Company Seal and Sign:

Signature and official seal validate and authorize the document.

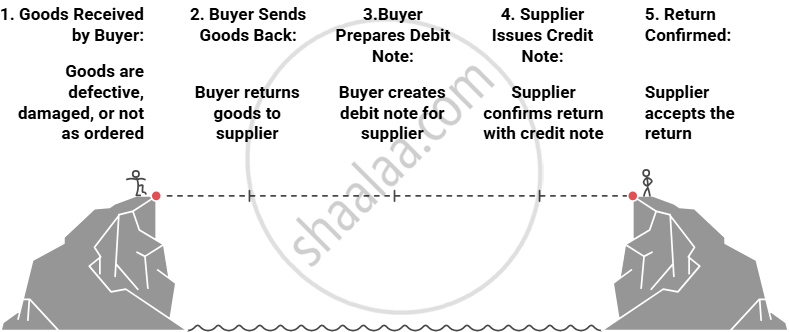

Process of Purchase Return

Debit and Credit Notes : Names Explained

-

The term "debit note" is used because, from the buyer’s perspective, the supplier’s account (a liability) is debited in the buyer’s books, reducing what the buyer owes

-

The term "credit note" is used because, from the supplier’s perspective, the buyer’s account (an asset - debtor) is credited in the supplier's books, reducing what the supplier expects to receive.

Example : Recording Transactions in Purchase Return Book

List of transactions to be recorded in the purchase book of UVW Enterprises for February 2025

| Date | Name of Supplier | Debit Note No. | L.F. | Amount (₹) |

|---|---|---|---|---|

| Feb. 8 | Bala Ji | DN01 | 101 | 1,900 |

| Feb. 12 | Kishan Traders | DN02 | 102 | 1,400 |

In the books of UVW Enterprises

Purchase Return Book

| Date | Name of Suppliers | Debit Note No. | L.F. | Amount (₹) |

|---|---|---|---|---|

| 2025 Feb. 8 | Bala Ji | DN01 | 101 | 1,900 |

| Feb. 12 | Kishan Traders | DN02 | 102 | 1,400 |

| 3,300 |

Posting in Ledger:

Dr. Purchase Return Account Cr.

| Date | Particulars | L.F. | Amt (₹) | Date | Particulars | L.F. | Amt (₹) |

|---|---|---|---|---|---|---|---|

| 2025 | |||||||

| Feb. 28 | By Sundries as per Purchase Return Book | 3,300 |

Key Takeaways

-

The Purchase Return Book records goods a business returns to suppliers, mainly for items bought on credit that are defective, excess, or not as ordered.

-

A debit note is sent by the buyer to the supplier, showing what goods are returned and by how much to reduce the amount owed.

-

A credit note is issued by the supplier to confirm and adjust the buyer’s account after receiving returned goods.

-

Main Purchase Return Book columns: Date, Supplier Name, Debit Note No., Ledger Folio, Amount.

-

The basic purchase return process: Identify items to return → issue debit note → update the purchase return book → receive credit note → adjust accounts.

-

The process helps keep both parties’ accounts accurate and transparent, preventing payment mistakes and disputes.