Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Books of Accounts

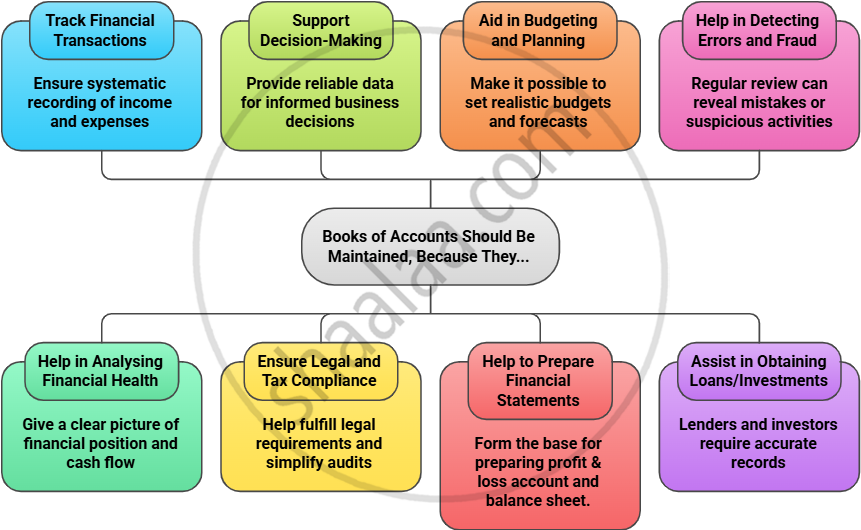

- Purpose

- Types

- How Books of Accounts Help People Involved with the Business

- Key Takeaways

Maharashtra State Board: Class 11

Definition: Books of Accounts

Books of accounts are records in which a business keeps a detailed log of all its financial transactions.

Maharashtra State Board: Class 11

Purpose

Maharashtra State Board: Class 11

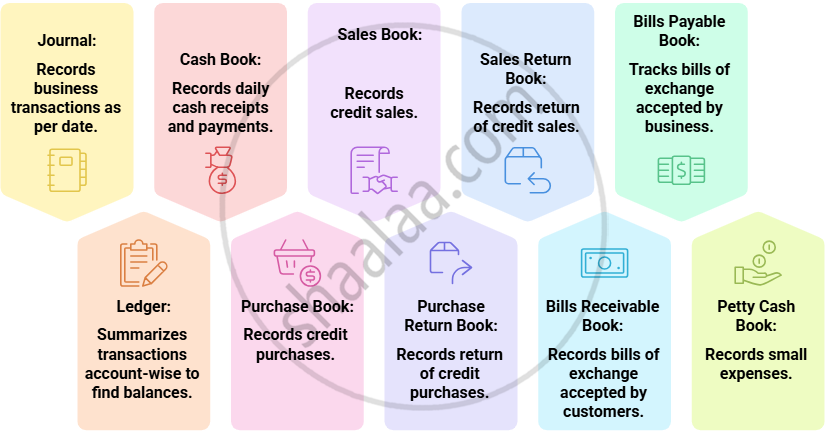

Types

Points to Remember:

- Bill of Exchange: A written document showing a debtor's promise to pay the creditor according to certain terms and conditions. It is accepted by the debtor by signing.

A bill of exchange is a "Bill Receivable" for the creditor because he will receive money.

A bill of exchange is a "Bill Payable" for the debtor because he will pay money. - Returns of cash purchases and sales are recorded in the cash book.

- Other registers for companies may include stock registers, cost records, securities registers, minute books, and contract registers for advanced record-keeping.

Maharashtra State Board: Class 11

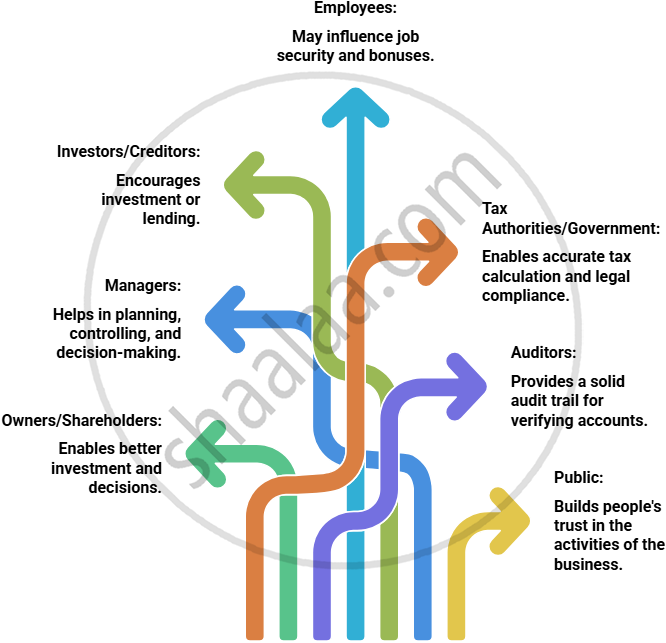

How Books of Accounts Help People Involved with the Business

What is an Audit Trail?

It is a step-by-step record that shows who did what, when, and how in a system or for a transaction. It helps you trace back every action—like payments, changes, or entries—to its source.

- It includes details like the user, date and time, and what was changed or done.

- Audit trails make it easy to spot mistakes or fraud and prove what happened during an audit.

Maharashtra State Board: Class 11

Key Takeaways

- Books of accounts are official records showing every financial transaction of a business.

- They track money inflow and outflow, helping avoid mistakes and mix-ups.

- Key books include the Journal (records by date), the Ledger (records by account), and special journals like Purchase and Sales books

- Maintaining books is mandatory by law (Companies Act, Income Tax Act, GST Act) if turnover or profit crosses set limits.

- Proper records help owners, managers, investors, employees, auditors, tax officers, and the public.

- Not keeping correct records can lead to legal trouble.

- Good record-keeping ensures transparency, supports business decisions, simplifies audits, and builds trust.