Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction to Final Accounts

- Importance

- Journey of a Transaction: From Journal to Final Accounts

- Definition: Proprietary Concern

- Definition: Final Accounts of a Proprietary Concern

- Overview: Final Accounts of a Proprietary Concern

- Direct Expenses vs. Indirect Expenses

- Examples: Direct Expenses vs. Indirect Expenses

- Direct Income vs. Indirect Income

- Examples: Direct Income vs. Indirect Income

- Key Takeaways

Introduction to Final Accounts

- Each time a business event occurs (like a purchase or sale), it is first recorded.

- After recording all transactions, the process ends with the preparation of final accounts, showing how much profit/loss occurred and what the business owns or owes.

Importance

| Point | Explanation |

|---|---|

| Determine Profit or Loss | Show gross and net profit or loss earned during the financial year through the Trading and Profit & Loss Account. |

| Reveal Financial Position | The balance sheet presents assets, liabilities, and capital, representing the firm’s financial health. |

| Help in Decision Making | Provide essential data for management to plan, control, and take financial and policy decisions. |

| Ensure Legal Compliance | Required by law for taxation, auditing, and regulatory purposes |

| Builds Transparency | Promote trust among stakeholders such as investors, lenders, employees, and government authorities. |

| Assist in Financial Analysis | Form the basis for ratio analysis and trend analysis to measure profitability and stability. |

| Help in Resource Planning | Indicate how effectively resources were utilized, guiding improvements for the next accounting period. |

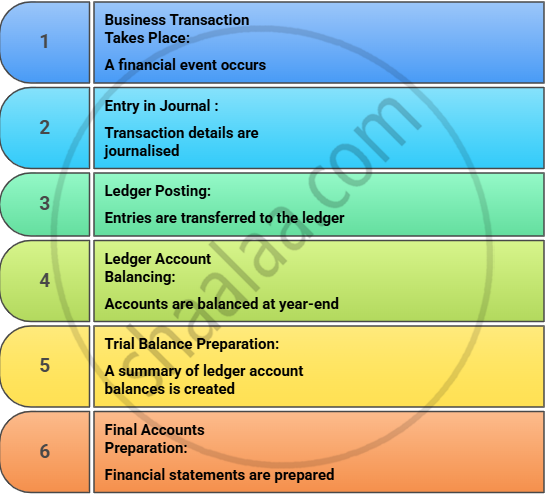

Journey of a Transaction : From Journal to Final Accounts

Definition : Proprietary Concern

A proprietary concern is a business owned, controlled, and managed by one person, who alone enjoys all profits and bears all losses of the business.

Definition : Final Accounts of a Proprietary Concern

Final Accounts are the last step of the accounting process,prepared at the end of the financial year to find out profit or loss and to know the financial position of a business owned by one person (proprietor).

Overview : Final Accounts of a Proprietary Concern

Final accounts are prepared using the trial balance and include:

| Part of Final Account | Description | Main Purpose |

|---|---|---|

| Trading Account | Shows details of direct income (sales) and direct expenses (purchases, wages, carriage inward, etc.). | To calculate the gross profit or gross loss of the business. |

| Profit and Loss Account | Includes all indirect incomes and expenses (like rent, salaries, depreciation, advertisement, etc.). | To ascertain the net profit or net loss after considering all indirect business activities. |

| Balance Sheet | Lists all assets, liabilities, and capital as on a specific date. It is not an account but a statement. | To show the financial position of the business—what it owns (assets) and what it owes (liabilities). |

Manufacturing Account (Additional for Manufacturing Businesses)

When the business produces goods instead of purchasing them, a manufacturing account is prepared before the trading account.

-

It shows the total cost of goods produced during the year.

-

Includes direct materials used, factory wages, and factory overheads (like power, factory rent, fuel, and machinery maintenance).

-

The total manufacturing cost is transferred to the trading account as the cost of goods manufactured.

Direct Expenses vs. Indirect Expenses

| Basis of Difference | Direct Expenses | Indirect Expenses |

|---|---|---|

| Meaning | Expenses directly related to the production, purchase, or manufacturing of goods and services. | Expenses related to running the business as a whole but not directly linked to production. |

| Purpose | Incurred to bring goods to a saleable state. | Incurred to manage and operate the business efficiently. |

| Stage of Occurrence | Arise during the production or purchase stage. | Arise after goods are produced or purchased. |

| Traceability | Can be directly traced to a specific product, department, or job. | Cannot be traced to a specific product or job. |

| Place Where it is Recorded | Recorded on the debit side of the trading account. | Recorded on the debit side of the Profit & Loss Account. |

| Impact on Profit | Help in calculating gross profit or gross loss. | Help in calculating net profit or net loss. |

Examples : Direct Expenses vs. Indirect Expenses

| Type | Examples |

|---|---|

| Direct Expenses |

|

| Indirect Expenses |

|

Direct Income vs. Indirect Income

| Basis of Difference | Direct Income | Indirect Income |

|---|---|---|

| Meaning | Income directly earned from the core business activities, such as the sale of goods or rendering of services. | Income earned from activities not directly related to the main business operations. |

| Nature | Recurring and regular—part of normal trading activity. | Usually non-recurring or supplementary income. |

| Relation to Business | Closely linked to the main operations of the business. | Generated from side or incidental activities. |

| Account Placement | Recorded on the credit side of the trading account. | Recorded on the credit side of the Profit & Loss Account. |

| Purpose | Help in calculating gross profit or gross loss. | Help in calculating net profit or net loss. |

Examples : Direct Income vs. Indirect Income

| Type of Income | Examples |

|---|---|

| Direct Income |

|

| Indirect Income |

|

Key Takeaways

- Final accounts form the concluding stage of the accounting process and reveal a business’s overall performance and financial standing at the end of an accounting period.

- Final accounts are important because they help determine profitability, measure financial stability, ensure accuracy and transparency, comply with tax and legal standards, and guide management decisions and business planning.

- Direct income and expenses aid in finding gross profit

- Indirect income and expenses help derive net profit

- Final accounts include the trading account, profit & loss account, and balance sheet, which together display the gross profit or loss, net profit or loss, and true financial position of a proprietary concern.

- In a manufacturing business, a Manufacturing Account is prepared first to determine the total cost of goods produced, which is then carried into the Trading Account.

- Trading Account records direct income and direct expenses connected with purchases and sales

- The profit & loss account records indirect income and indirect expenses linked to administration, selling, and other operations.

- The balance sheet finally presents all assets, liabilities, and capital to show the firm’s financial health.