Topics

National Income and Related Aggregates

- Macroeconomics Vs Microeconomics

- Representative Goods and Sectors

- Macroeconomic Agents and Government Role

- Emergence of Macroeconomics

- Context of the Present Book of Macroeconomics

- Meaning of Economic Wealth and Final Goods

- Stocks, Flows, and Depreciation

- Capital Formation, Trade-off & Circular Flow of Income

- Circular Flow of Income and Methods of Calculating National Income

- Output Method/Product Method

- Expenditure Method

- Income Method

- Factor Cost, Basic Prices and Market Prices

- Some Macroeconomic Identities

- National Disposable Income

- Private Income

- National Income Aggregates

- Real GDP and Nominal GDP

- GDP and Welfare

Introductory Macroeconomics

Introduction

- A Simple Economy

- Central Problems of an Economy

- Concepts of Production Possibility Frontier

- Organisation of Economic Activities

- Positive and Normative Economics

- Macroeconomics Vs Microeconomics

Development Experience (1947-90) and Economic Reforms since 1991

- India's Economy Before Independence

- Low Level of Economic Development Under the Colonial Rule

- Agricultural Sector in India

- Industrial Sector

- Foreign Trade of India

- Demographic Condition

- Occupational Structure

- Infrastructure

- Post-Independence Economic Systems and Planning

- Five Year Plans (FYP)

- Agriculture

- Industry and Trade

- Trade Policy: Import Substitution

- The 1991 Economic Crisis and Reforms

- Background of the New Economic Policy

- Liberalisation

- Privatisation

- Globalisation

- World Trade Organisation (WTO)

- Impact of the Economic Reforms

Theory of Consumer Behaviour

- Consumer Behaviour: The Problem of Choice

- Basic Concepts of Microeconomics > Utility

- Cardinal Approach (Utility Analysis)

- Derivation of Demand Curve in the Case of a Single Commodity

- Ordinal Utility Analysis/Indifference Curve Analysis

Indian Economic Development

Current Challenges Facing Indian Economy

- Concept of Human Capital

- Sources of Human Capital

- Human Capital and Economic Growth

- Human Capital and Human Development

- State of Human Capital Formation in India

- Growth of Education Sector in India

- Challenges and Future Prospects in Education

- Rural Development in India

- Credit and Marketing in Rural Areas

- Agricultural Market System

- Diversification into Productive Activities

- Sustainable Development and Organic Farming

- The Nature and Importance of Work in Society

- Workers and Employment

- Participation of People in Employment

- Self-employed and Hired Workers

- Employment in Firms, Factories and Offices

- Growth and Changing Structure of Employment

- Informalisation of Indian Workforce

- Concept of Unemployment

- Government and Employment Generation

- Environment and Sustainable Development in India

- State of India’s Environment

- Concept of Sustainable Development

- Strategies for Sustainable Development

Money and Banking

- Concept of Money

- Functions of Money

- Demand for Money and Supply of Money

- Money Creation by Banking System

- Limits to Credit Creation and Money Multiplier

- Policy Tools To Control Money Supply

- Demand and Supply for Money : A Detailed Discussion

- The Transaction Motive

- The Speculative Motive

- Various Measures of Supply of Money

- Narrow and Broad Money

- Demonetisation

Development Experience of India – a Comparison with Neighbours

Introductory Microeconomics

Production and Costs

- Production Function

- Basics of Production Theory

- Variation of Output in the Short-Run Returns to a Factor

- Relation Between Total, Average and Marginal Product

- Law of Variable Proportions

- Average and Marginal Physical Products

- Changes in Production

- Cost - Fixed Cost

- Cost -variable Cost

- Behaviour of Cost in the Short - Run

- Relationship Between Average Variable Cost and Average Total Cost and Marginal Cost

- Concept of Opportunity Cost

- Marginal Revenue

- Producer's Equilibrium

- Law of Supply

- Market Supply Schedule

- Distinguish between Stock and Supply

- Determinants of Supply

- Movements Along and Shifts in Supply Curve

- Measurement of Elasticity of Supply > Percentage Method

- Methods of Measurement of National Income

- Cost Concepts > Marginal Cost

- The Law of Diminishing Marginal Product

- Shapes of Product Curves

- Costs in Long Run Period

- Returns to Scale

Determination of Income and Employment

- Aggregate Demand and Its Components

- Consumption

- Investment

- Determination of Income in Two-sector Model

- Determination of Equilibrium Income in the Short Run

- Macroeconomic Equilibrium with Price Level Fixed

- Effect of an Autonomous Change in Aggregate Demand on Income and Output

- The Multiplier Mechanism

- Paradox of Thrift

- Equilibrium Output and Employment

The Theory of the Firm Under Perfect Competition

- Concept of Market

- Market Equilibrium

- Determination of Market Equilibrium

- Effects of Changes (Shifts) in Demand on Equilibrium Price and Equilibrium Quantity

- Perfect Competition

- Imperfect Competition

- Classification of Market Structure

- Oligopoly

- Market Forms - Perfect Oligopoly

- Market Forms - Imperfect Oligopoly

- Equilibrium Price

- Applications of Tools of Demand and Supply Price Control

- Price Ceiling

- Price Floor

- Revenue Concepts

- Profit Maximisation Objective

- Determinants of a Firm’s Supply Curve

- Market Supply Schedule

- Price Elasticity of Supply

Government Budget and the Economy

Balance of Payments

- Open Economy and Its Linkages

- Concept of Balance of Payments

- Current Account

- Capital Account

- Balance of Payments Surplus and Deficit

- Foreign Exchange Market

- Foreign Exchange Rate

- Determination of the Exchange Rate

- Merits and Demerits of Flexible and Fixed Exchange Rate Systems

- Managed Floating Exchange Rate System

Market Equilibrium

- Simple Monopoly in the Commodity Market

- Other Non - Perfectly Competitive Markets

- Introduction

- Definition: Long Run

- Definition: Long Run Total Cost

- Long Run Total Cost

- Definition: Long Run Average Cost

- Long Run Average Cost

- Names for LAC

- Relationship: LAC and SAC

- Definition: Long Run Marginal Cost

- Long Run Marginal Cost

- Relation Between LMC and LAC

- Key Points: Costs in Long Run Period

CISCE: Class 12

Introduction

- The long run is a period in which a firm can change all its inputs—including machines, buildings, and workers. No input is fixed; everything can be adjusted to change output.

- Example: If a bakery wants to bake more bread in the long run, it can buy new ovens, hire more staff, or move to a bigger location.

CISCE: Class 12

Definition: Long Run

- "In the long-run, all the factors of production are assumed to be variable." - Koutsoyiannis

- "It will be helpful to think of the long run situation into any one in which the firm can move." - Leftwich

CISCE: Class 12

Definition: Long Run Total Cost

"The long run total cost of production is the least possible cost of producing any given level of output when all inputs are variable." - Libhafasky

CISCE: Class 12

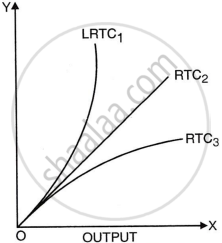

Long Run Total Cost

- LRTC: The lowest possible total cost for making any amount of goods when all inputs can vary.

- In the long run, there are no fixed costs—if nothing is produced, total cost is zero.

CISCE: Class 12

Defnition: Long Run Average Cost

"The long run average cost curve shows the lowest average cost of producing output when all inputs can be varied freely." - Robert Awh

CISCE: Class 12

Long Run Average Cost

- Formula:

\[\overline{\mathrm{LAC}=}\frac{\mathrm{LRTC}}{\text{Quantity of Output}}\] - LAC curve shows the lowest average cost per unit when all factors can be chosen.

- Analogy: Think of LAC as the “cheapest possible menu” you could pick to feed your group, if you could freely select all ingredients and cooking tools.

CISCE: Class 12

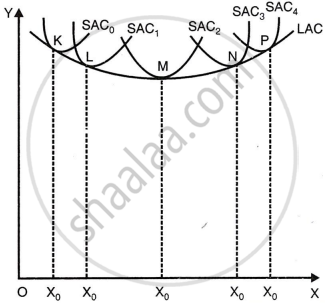

Names for LAC

- Envelope Curve: LAC surrounds all the short-run average cost (SAC) curves; it never rises above them, just touches them.

- Planning Curve: Helps firms decide which plant size is best for different output levels.

CISCE: Class 12

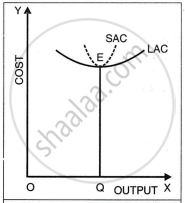

Relationship: LAC and SAC

- SAC is for a single plant; LAC is for the best of all possible plant choices.

- Both are usually U-shaped, but LAC is flatter, showing costs change less sharply in the long run.

- LAC touches only one SAC at its lowest point; for others, tangency is not at their minimum.

CISCE: Class 12

Definition: Long Run Marginal Cost

"Long-run marginal cost curve is that which shows the extra cost incurred in producing one more unit of output when all inputs can be changed." - Robert Awh

Long Run Marginal Cost

- LMC: Extra cost for making one more unit when all inputs can be changed.

- Formula:

\[\overline{\mathrm{LMC}=\frac{\Delta\mathrm{LTC}}{\Delta Q}}\]

CISCE: Class 12

Relation Between LMC and LAC

The connection between long run marginal cost (LMC) and long run average cost (LAC) works just like the short-run case:

- When LAC is falling: LMC is below LAC, and it falls faster than LAC.

- At the minimum point of LAC: LMC and LAC are equal. This is where both curves meet.

- When LAC is rising: LMC is above LAC and increases faster than LAC.

CISCE: Class 12

Key Points: Costs in Long Run Period

- In the long run, firms can change all production factors for least cost.

- LAC curve helps in selecting the best way to produce for each output.

- LMC tells us how much extra cost is needed to raise output by one unit.

- Understanding cost curves helps firms plan profitably for both present and future production.