Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Petty Cash Book

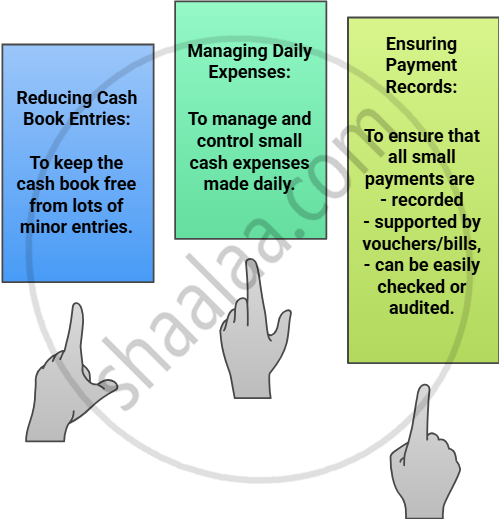

- Need to Maintain

- Definition: Petty Cashier

- Responsibilities of Petty Cashier

- Types of Petty Cash Book

Definition : Petty Cash Book

A petty cash book is a type of cash book in accounting that records all minor, routine cash payments and receipts separately from the main cash book.

Need to Maintain

Definition : Petty Cashier

A petty cashier is responsible for handling petty cash and maintaining the petty cash book.

Responsibilities of Petty Cashier

The petty cashier:

-

Receives the fixed petty cash amount from the main cashier.

-

Pays for small expenses and records each transaction in the book, with a supporting voucher for every entry.

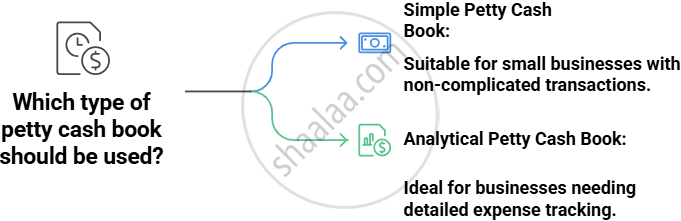

Types of Petty Cash Book

Related QuestionsVIEW ALL [32]

From the following information prepare Columnar Petty Cash Book kept on imprest system in the books of Manisha Books Stall, Beed.

| 2018 | Amt (₹) | |

| April 01 | Opening petty cash balance | 200 |

| 01 | Received a bearer cheque to make up the imprest amount | 1,200 |

| 03 | Gave a tips to peon | 40 |

| 04 | Purchased stationery | 150 |

| 05 | Paid Taxi Fare | 35 |

| 06 | Purchased Stamp pad | 140 |

| 07 | Paid Cartage | 40 |

| 08 | Paid Bus Fare | 30 |

| 11 | Paid to sweeper | 50 |

| 13 | Purchased a Box of pencils | 40 |

| 14 | Paid Mobile charges | 35 |

| 15 | Gave to Sohan on account | 250 |

| 19 | Paid for Refreshment to staff | 150 |

| 20 | Paid Railway Fare | 30 |

| 21 | Paid Carriage | 65 |

From the following information prepare Columnar Petty Cash Book kept on imprest system in the books of Manisha Books Stall, Beed.

| 2018 April | Amt (₹) | |

| 01 | Opening petty cash balance | 200 |

| 02 | Received a bearer cheque to make up the imprest amount | 1,200 |

| 03 | Gave a tips to peon | 40 |

| 04 | Purchased stationery | 150 |

| 05 | Paid Taxi Fare | 35 |

| 06 | Purchased Stamp pad | 140 |

| 07 | Paid Cartage | 40 |

| 08 | Paid Bus Fare | 30 |

| 11 | Paid to sweeper | 50 |

| 13 | Purchased a Box of pencils | 40 |

| 14 | Paid Mobile charges | 35 |

| 15 | Gave to Sohan on account | 250 |

| 19 | Paid for Refreshment to staff | 150 |

| 20 | Paid Railway Fare | 30 |

| 21 | Paid Carriage | 65 |

From the following information prepare Columnar Petty Cash Book kept on imprest system in the books of Manisha Books Stall, Beed.

| 2018 April | Amt (₹) | |

| 01 | Opening petty cash balance | 200 |

| 02 | Received a bearer cheque to make up the imprest amount | 1,200 |

| 03 | Gave a tip to peon | 40 |

| 04 | Purchased stationery | 150 |

| 05 | Paid Taxi Fare | 35 |

| 06 | Purchased Stamp pad | 140 |

| 07 | Paid Cartage | 40 |

| 08 | Paid Bus Fare | 30 |

| 11 | Paid to sweeper | 50 |

| 13 | Purchased a box of pencils | 40 |

| 14 | Paid Mobile charges | 35 |

| 15 | Gave it to Sohan on account | 250 |

| 19 | Paid for Refreshment to staff | 150 |

| 20 | Paid Railway Fare | 30 |

| 21 | Paid Carriage | 65 |

From the following information prepare Columnar Petty Cash Book kept on imprest system in the books of Manisha Books Stall, Beed.

| 2018 April | Amt (₹) | |

| 01 | Opening petty cash balance | 200 |

| 02 | Received a bearer cheque to make up the imprest amount | 1,200 |

| 03 | Gave a tips to peon | 40 |

| 04 | Purchased stationery | 150 |

| 05 | Paid Taxi Fare | 35 |

| 06 | Purchased Stamp pad | 140 |

| 07 | Paid Cartage | 40 |

| 08 | Paid Bus Fare | 30 |

| 11 | Paid to sweeper | 50 |

| 13 | Purchased a Box of pencils | 40 |

| 14 | Paid Mobile charges | 35 |

| 15 | Gave to Sohan on account | 250 |

| 19 | Paid for Refreshment to staff | 150 |

| 20 | Paid Railway Fare | 30 |

| 21 | Paid Carriage | 65 |

From the following information prepare Columnar Petty Cash Book kept on imprest system in the books of Manisha Books Stall, Beed.

| 2018 April | Amt(₹) | |

| 01 | Opening petty cash balance | 200 |

| 02 | Received a bearer cheque to make up the imprest amount | 1,200 |

| 03 | Gave a tips to peon | 40 |

| 04 | Purchased stationery | 150 |

| 05 | Paid Taxi Fare | 35 |

| 06 | Purchased Stamp pad | 140 |

| 07 | Paid Cartage | 40 |

| 08 | Paid Bus Fare | 30 |

| 11 | Paid to sweeper | 50 |

| 13 | Purchased a Box of pencils | 40 |

| 14 | Paid Mobile charges | 35 |

| 15 | Gave to Sohan on account | 250 |

| 19 | Paid for Refreshment to staff | 150 |

| 20 | Paid Railway Fare | 30 |

| 21 | Paid Carriage | 65 |