Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Voucher

- Types of Vouchers

- Important Points Regarding Voucher Types

- Examples for Each Voucher Type

- Importance of Vouchers

- Information Given by a Voucher

- How to Prepare a Voucher

- Key Takeaways

Maharashtra State Board: Class 11

Definition : Voucher

A voucher is a formal written document that supports and records a financial transaction in business or accounting.

Maharashtra State Board: Class 11

Types of Vouchers

| Voucher | Use |

|---|---|

| Cash Voucher | Used to record all cash (notes/coins) transactions (payment or receipt). Has the following subtypes:

|

| Journal Voucher | Used to record adjustments, corrections, or entries not involving direct cash |

| Non-Cash / Transfer Voucher | A type of journal voucher used only to transfer balances between accounts, with no cash or bank involved |

| Contra Voucher | Used to record transactions that involve the transfer of funds between cash and bank accounts, or between two bank accounts within the same business. |

| Compound Voucher | Records multiple debits and credits in a single transaction. Here, only one side (debit or credit) has multiple accounts; the other side has just one account. |

| Complex Voucher | Used when multiple parties are involved with multiple debits and credits. Both sides (debit or credit) can have multiple accounts each. |

| Internal Voucher | Created by the business itself without any external document |

| External Voucher | Received from an agency (outside business) as proof of transaction |

| Purchase Voucher | Records all purchase transactions |

| Sales Voucher | Records all sales transactions |

| Bank Voucher | Records all bank-related (cheque, NEFT, DD) transactions. Has the following subtypes:

|

| Debit Note | Used when goods are returned to the supplier (purchase return) or to request a reduction in the amount owed. |

| Credit Note | Used when goods are returned by a customer (sales return) or when the business needs to credit the customer for an overcharge or adjustment. |

Maharashtra State Board: Class 11

Important Points Regarding Voucher Types

1. Purchase and Sale Vouchers vs. Payment/Debit and Receipt/Credit Vouchers

| Voucher Type | Purpose |

|---|---|

| Purchase/Sale Vouchers | Record the actual transaction of buying or selling goods |

| Payment/Receipt Vouchers | Record the cash or bank settlement of the transaction |

Note: Payment and receipt vouchers are used to show money movement, not the commercial activity

2. Bank Vouchers vs. Payment/Debit and Receipt Vouchers

| Voucher Subtype | Direction of Money | Mode of Transaction |

|---|---|---|

| Cash Payment / Cash Receipt | Outflow/Inflow | Cash |

| Bank Payment / Bank Receipt | Outflow/Inflow | Bank |

Note: Subtypes help avoid confusion by showing both direction and mode of transaction

3. Why main voucher types (cash, bank) exist when there are clear subtypes (cash receipt, bank receipt, etc.):

| Main Voucher Type | Purpose |

|---|---|

| Cash/Bank Vouchers | Instantly show whether the transaction involved physical cash or a bank. |

| Payment/Receipt | Show direction of funds (inflow or outflow) |

Note: Both mode and direction are needed for accurate record-keeping and auditing

4. Journal Vouchers vs. Transfer Vouchers

| Voucher Type | Used For |

|---|---|

| Journal Vouchers | Adjustments, corrections, provisions, and transfers (broad category) |

| Transfer Vouchers | Only for internal account-to-account transfers |

Note: Transfer vouchers provide sharper classification within journal entries

5. Voucher Name Logic: Debit/Payment Vouchers and Credit/Receipt Vouchers

| Voucher Type | Rule Applied | Reason for Name / Name Logic |

|---|---|---|

| Credit/Receipt | Credit the Giver (Personal Account) Debit what comes in (Real account). |

The account of the person giving cash is credited—proof that money was received. Income is credited, hence the name "credit" voucher, and cash is received, so it is also called a "receipt" voucher. |

| Debit/Payment | Debit the Receiver (Personal Account) Credit what goes out (Real account). |

The receiving account is debited, confirming that money was paid out. Expense is debited, hence the name "debit" voucher, and cash is paid, so it is also called a "payment" voucher. |

Maharashtra State Board: Class 11

Examples for Each Voucher Type

| Voucher Type | Example |

|---|---|

| Cash Voucher | Cash paid for office supplies or cash received from sales |

| Bank Voucher | Payment to supplier by cheque or cash deposited into bank |

| Contra Voucher | Cash withdrawn from bank for office use or cash deposited in bank |

| Journal Voucher | Recording depreciation or accrued salary (no cash involved) |

| Transfer Voucher | Moving funds from travel expenses to administration expenses |

| Purchase Voucher | Buying raw materials from a supplier (cash/credit/bank) |

| Sales Voucher | Selling goods to a customer (cash/credit/bank) |

| Compound Voucher | Paid electricity bill ₹2,000 and telephone bill ₹1,000 in cash (electricity expenses and telephone expenses accounts are debited and only cash account is credited) |

| Complex Voucher | Paid salaries to staff (₹20,000) and rent (₹10,000) by cash and received commission income (₹5,000) by cheque—all in one transaction. (Salaries and rent accounts are debited. Cash, commission, and bank accounts are credited.) |

| Credit Note | Goods returned by a customer (issuing a credit note) |

| Debit Note | Returning defective goods to supplier (sending a debit note) |

| Internal Voucher | Preparing a slip for taxi fare paid (no external receipt) |

| External Voucher | Supplier’s invoice for goods purchased |

Maharashtra State Board: Class 11

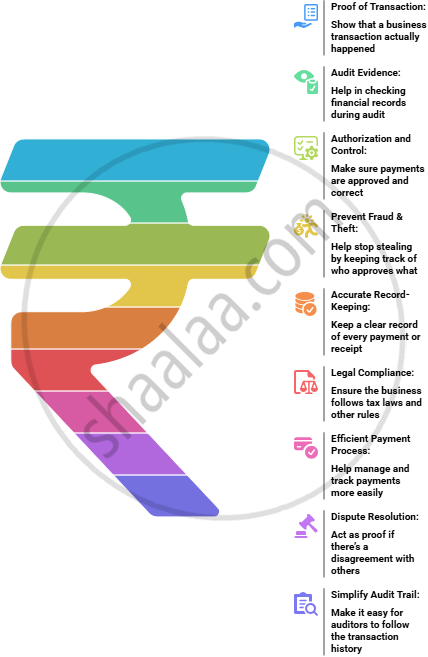

Importance of Vouchers

Maharashtra State Board: Class 11

Information Given by a Voucher

Common Details in All Vouchers

| Detail | Description |

|---|---|

| Voucher Number/Serial Number | Unique for tracking and audit |

| Date | When the voucher is prepared/transaction occurred |

| Amount | Full amount (with taxes/deductions if needed) |

| Account Codes | Relevant ledger accounts debited/credited |

| Name of Party | Supplier, customer, payee, or receiver |

| Description/Narration | Purpose and details of transaction |

| Supporting Documents | Bills, invoices, receipts, contracts, delivery notes, etc. |

| Prepared By | Name/signature of creator |

| Approved By | Name/signature of approver or authorized person |

Additional Details as per Voucher Type

| Voucher Type | Additional Details |

|---|---|

| Payment/Debit | Payment method (cash, cheque, bank transfer), reason for payment, payee details |

| Receipt/Credit | Mode of receipt (cash, bank), customer info, reference to invoice/sale |

| Journal Voucher | Adjustment/correction details: reason for entry, accounts affected (no cash/bank involved) |

| Contra Voucher | Accounts involved (cash, bank, or both); reference to bank/cash book; slip of fund movement. |

| Purchase Voucher | Item details, quantity, purchase order/invoice number, supplier info, payment terms |

| Sales Voucher | Product/service sold, quantity, invoice number, customer info, sales terms |

| Bank Voucher | Bank name, cheque/NEFT/DD number, bank account details, transaction reference |

| Transfer Voucher | Accounts being transferred from/to, purpose of transfer, supporting internal memo |

| Compound/Complex | Multiple debits/credits listed, combined amounts, linked accounts, reason for group entry |

| Debit Note Voucher | Reason for return/adjustment, item and quantity returned, reference to original purchase |

| Credit Note Voucher | Reason for adjustment, item returned by customer, reference to original sale |

Maharashtra State Board: Class 11

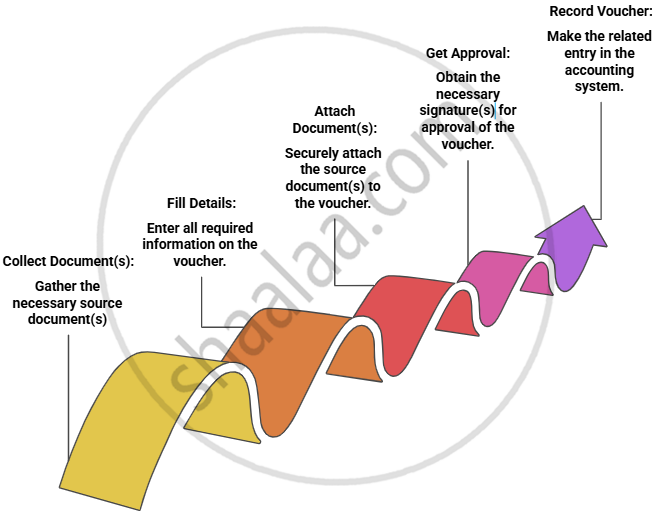

How to Prepare a Voucher

Maharashtra State Board: Class 11

Key Takeaways

-

A voucher is proof of a business transaction.

-

There are many voucher types, e.g., cash, bank, journal, etc.

- Separate voucher types make accounting clear, accurate, and reliable.

-

Always attach documents and have signatures for every voucher.

-

Neatly filed vouchers help during audits and queries