Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Bank Passbook

- Origin

- Comparison with Books of Accounts

- Contents

- Examples of Transactions Recorded in Passbook

- Advantages and Disadvantages

- Physical Passbook vs. Electronic Passbook

- Process of Recording Transactions in Passbook

- Key Takeaways

Definition : Bank Passbook

A bank passbook is a small book or a digital app that helps keep track of all the money coming in and going out of a bank account—like deposits, withdrawals, and current balance.

Origin

-

Passbooks first appeared in the 18th century, introduced by European banks as a way for customers to hold transaction information in their own hands for the first time.

-

Earlier, banks kept all transaction records only in their own ledgers, so customers had no direct access to their deposit or withdrawal history.

-

The passbook gave customers more control over their financial affairs and allowed them to verify that bankers followed instructions properly.

-

It was called a "passbook" because it regularly passed between the bank and the account holder for updates and identification.

-

In India, modern banking evolved during British colonial times, and passbooks became standard as the banking system matured with Presidency Banks and later the Reserve Bank of India.

-

The passbook system gave Indian bank customers easier access and more transparency about their accounts, a tradition that continues alongside digital banking today.

Comparison with Books of Accounts

| Point | Bank Passbook | Books of Accounts |

|---|---|---|

| Maintained By | Bank, for the account holder | Business or individual, for internal use |

| Perspective | Shows the bank’s view of the customer’s transactions | Shows the entity’s own view of its cash or bank transactions |

| Purpose | To keep the customer updated and confirm all bank transactions | To record and analyze all cash and bank transactions systematically |

| Main Entries | Deposits, withdrawals, bank charges, interest, etc.—from bank’s angle | Receipts, payments, transfers—entered by the business itself |

| Entry Recording | Updated by bank officials during visits or automatically through computerized systems | Entered regularly by the business |

| Shows Balance | Reflects customer’s actual account balance (can show overdraft) | Reflects cash and bank balances of business; overdraft handled separately |

| Legal Use | Accepted as documentary evidence for transactions and disputes | Used for audits, financial analysis, and reconciliation |

| Role in Matching Records | Basis for verifying and reconciling differences with own records | Used to check, adjust, and match against bank records (passbook) |

Contents

| Section/Entry | What It Shows | Reason for Inclusion |

|---|---|---|

| Bank Name & Branch | Identifies the bank and branch issuing the passbook | Authenticates account location and source |

| Branch Address & Phone/Email | Contact information of the branch | Helps customers reach the bank for queries or support |

| IFSC & MICR Code | Codes for electronic transactions and cheque clearance | Enables NEFT/RTGS transfers and cheque processing |

| Account Holder Name/Photo | Owner’s identity verification | Prevents misuse; bank can verify during transactions |

| Account Number & Customer ID | Unique identifiers for the account | Required for all account-related activities and error resolution |

| Date of Account Opening | When the account was started | Useful for history and eligibility (loans, schemes, etc.) |

| Nominee Details | Chosen beneficiary in case of emergencies | Ensures proper settlement and legal protection |

| Columns for Transactions: | ||

| - Date | Date of each transaction | Tracks activity and timing |

| - Particulars | Description of transaction (e.g., deposit, ATM withdrawal) | Shows the type of transaction for clarity |

| - Cheque No. | The number of payments/withdrawals involves a cheque | Allows verification and tracing |

| - Withdrawals (Dr.) | Amount debited from account | Shows outflows; helps monitor spending |

| - Deposits (Cr.) | Amount credited to account | Tracks income or savings added |

| - Balance | Running total after each entry | Shows current status and helps reconciliation |

| - Bank Officer’s Signature/Initials | Confirmation by a bank staff | Acknowledges transaction authenticity |

| Rules/Instructions Section | Usage guidelines, precautions, and dispute handling info | Helps customers use the passbook correctly and safely |

-

Identification: Prevents confusion or fraud by verifying branch, user, and account.

-

Regulatory Compliance: Laws/RBI require banks to record and present these details clearly for customer service and dispute resolution.

-

Transaction Monitoring: Transaction columns help customers keep personal records and catch errors early.

-

Transparency: Customers can verify entries, improving trust and financial management.

-

Electronic Banking Support: IFSC/MICR codes make online/digital banking easier and safer.

-

Security & Legal Proof: Photos and account details help prevent unauthorized usage and serve as evidence in case of disputes.

Advantages and Disadvantages

| Advantages | Disadvantages |

|---|---|

| Provides a physical record of all transactions | Requires visiting the bank branch for regular updates |

| Easy to see all deposits, withdrawals, and balance | Passbook can be lost or damaged, risking information loss |

| Helps in tracking money and detecting errors | No online access or instant update like digital statements |

| Promotes savings discipline by limiting impulsive withdrawals | Updating may be slow, especially in busy banks |

| Accepted as official proof of transactions | Limited to banks that still maintain physical passbooks |

| No risk of cyber-theft or hacking | May not show real-time balance during the day |

| Encourages good financial habits for beginners | Can fill up and need replacement; handwriting can be unclear |

Physical Passbook vs. Electronic Passbook

| Aspect | Physical Passbook | Electronic Passbook (e-Passbook) |

|---|---|---|

| Format | Paper booklet | Mobile app or web platform |

| Update Method | Manual (bank staff enters transactions) | Automatic, real-time updates |

| Accessibility | Only at bank branch during working hours | 24/7 access from anywhere with internet |

| Transaction Search | Manual; flip through pages | Quick search and filter options |

| Security | Can be lost/damaged; privacy depends on user care | Digital security (password/OTP/2FA) |

| Environmental Impact | Uses physical paper | Eco-friendly, paperless |

| Cost | Possible fee for lost/damaged booklet | Usually free with digital banking |

| Entry Limit | Limited by pages; new booklet needed when full | Extensive history, typically months or years |

| Durability | Susceptible to wear, tear, water damage | Not affected by physical conditions |

| Internet Required | No | Yes |

| Tech Knowledge | Not needed | Basic digital literacy needed |

| Official Validity | Widely accepted as physical proof | Sometimes additional verification is needed. |

| Real-time Balance | Only when updated at bank | Always current, real-time balance |

| Extra Features | None | Analytics, budgeting tools, multiple accounts |

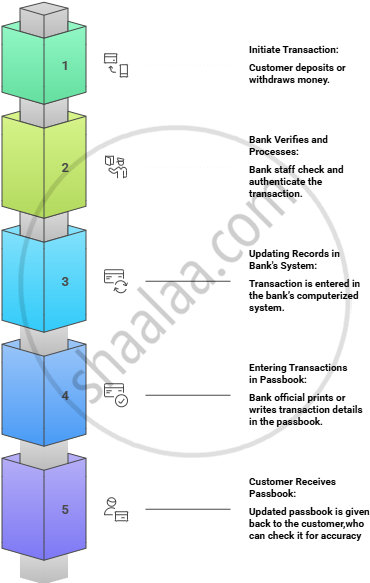

Process of Recording Transactions in Passbook

Examples of Transactions Recorded in Passbook

| Date | Particulars | Ch. No. | Withdrawals (Dr.) | Deposits (Cr.) | Balance | Officer’s Initials |

|---|---|---|---|---|---|---|

| 06/10/2025 | Salary Deposit | 98123 | 25,000 | 25,000 | SD | |

| 09/10/2025 | ATM Withdrawal | 2,000 | 23,000 | LK | ||

| 10/10/2025 | Interest Credit | 100 | 23,100 | RS |

Key Takeaways

-

A bank passbook is a physical booklet given by the bank recording all deposits, withdrawals, and balances in an account.

-

It originated in the 18th century to give customers direct access to transaction history, and became standard in Indian banking during colonial times.

-

Passbooks include bank name, branch, IFSC/MICR codes, account holder details, and a transaction table with date, particulars, cheque no., debit, credit, balance, and bank staff initials for verification.

-

Transactions are recorded when the customer makes transactions, bank updates its records, and prints them in the passbook during branch visits.

-

A passbook is maintained by the bank, while books of accounts like cashbooks are maintained by the account holder or business.

-

Pros of passbooks: easy verification, official proof, no digital fraud risk; Cons: manual updating required, can be lost/damaged, not always real-time.

-

An e-passbook is the digital version of a passbook, offering real-time updates and remote access via mobile or web.

-

Physical passbooks require branch visits and carry risk of damage; e-passbooks offer 24/7 access and search capabilities but require internet and some digital literacy.