Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

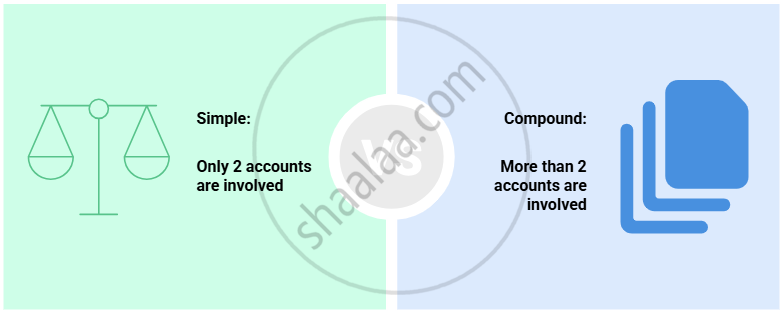

- Definition : Journal Entry

- Types

- Examples

Definition : Journal Entry

A journal entry is a short written record of a business transaction in the accounting books, showing which account is debited and which is credited, always following the double-entry system.

Types

Examples

| Type of Journal Entry | Transaction | Journal Entry |

|---|---|---|

| Simple Entry | Purchased goods for cash ₹10,000 on 9th September, 2025. | Date: 2025/09/09 Purchases A/c Dr. ₹10,000 To Cash A/c ₹10,000 (Being goods purchased for cash) |

| Compound Entry | Paid rent of ₹5,000 and an electricity bill of ₹2,000 by cash on 10th September, 2025. | Date: 2025/09/10 Rent A/c Dr. ₹5,000 Electricity Expense A/c Dr. ₹2,000 To Cash A/c ₹7,000 (Being rent and electricity bill paid) |

Related QuestionsVIEW ALL [8]

Enter the following transactions in the journal of Manohar who is dealing in textiles:

| 2018 March | Particulars | ₹ |

| 1 | Manohar started business with cash | 60,000 |

| 2 | Purchased furniture for cash | 10,000 |

| 3 | Bought goods for cash | 25,000 |

| 6 | Bought goods from Kamalesh on credit | 15,000 |

| 8 | Sold goods for cash | 28,000 |

| 10 | Sold goods to Hari on credit | 10,000 |

| 14 | Paid Kamalesh | 12,000 |

| 18 | Paid rent | 500 |

| 25 | Received from Hari | 8,000 |

| 28 | Withdrew cash for personal use | 4,000 |

Mary is a rice dealer having business for more than 5 years. Pass journal entries in her books for the period of March, 2018.

| March | Particulars | ₹ |

| 1 | Cement bags bought on credit from Sibi | 20,000 |

| 2 | Electricity charges paid through net banking | 500 |

| 3 | Returned goods bought from Sibi | 5,000 |

| 4 | Cement bags taken for personal use | 1,000 |

| 5 | Advertisement expenses paid | 2,000 |

| 6 | Goods sold to Mano | 20,000 |

| 7 | Goods returned by Mano | 5,000 |

| 8 | Payment received from Mano through NEFT | 15,000 |

Pass journal entries in the books of Sasi Kumar who is dealing in automobiles.

| 2017 Oct | Particulars | ₹ |

| 1 | Commenced business with goods | 40,000 |

| 3 | Cash introduced in the business | 60,000 |

| 4 | Purchased goods from Arul on credit | 70,000 |

| 6 | Returned goods to Arul | 10,000 |

| 10 | Paid cash to Arul on account | 60,000 |

| 15 | Sold goods to Chandar on credit | 30,000 |

| 18 | Chandar returned goods worth | 6,000 |

| 20 | Received cash from Chandar in full settlement | 23,000 |

| 25 | Paid salaries through ECS | 2,000 |

| 30 | Sasi Kumar took for personal use goods worth | 10,000 |

From the following transactions of Shyam, a stationery dealer, pass journal entries for the month of August 2017.

| Aug. | Particulars |

| 1 | Commenced business with cash ₹ 4,00,000, Goods ₹ 5,00,000 |

| 2 | Sold goods to A and money received through RTGS ₹ 2,50,000 |

| 3 | Goods sold to Z on credit for ₹ 20,000 |

| 5 | Bill drawn on Z and accepted by him ₹ 20,000 |

| 8 | Bill received from Z is discounted with the bank for ₹ 19,000 |

| 10 | Goods sold to M on credit ₹ 12,000 |

| 12 | Goods distributed as free samples for ₹ 2,000 |

| 16 | Goods taken for office use ₹ 5,000 |

| 17 | M became insolvent and only 0.80 per rupee is received in final settlement |

| 20 | Bill of Z discounted with the bank is dishonoured |

Raja has a hotel. The following transactions took place in his business. Journalise them.

| Jan. | Particulars | ₹ |

| 1 | Started business with cash | 3,00,000 |

| 2 | Purchased goods from Rajiv on credit | 1,00,000 |

| 3 | Cash deposited with the bank | 2,00,000 |

| 20 | Borrowed loan from bank | 1,00,000 |

| 22 | Withdrew from bank for personal use | 800 |

| 23 | Amount paid to Rajiv in full settlement through NEFT | 99,000 |

| 25 | Paid club bill of the proprietor by cheque | 200 |

| 26 | Paid electricity bill of the proprietor’s house through debit card | 2,000 |

| 31 | Lunch provided at free of cost to a charity | 1,000 |

| 31 | Bank levied charges for locker rent | 1,000 |

Journalise the following transactions in the books of Ramesh who is dealing in computers:

| 2018 March | Particulars |

| 1 | Ramesh started business with cash ₹ 3,00,000, Goods ₹ 80,000 and Furniture ₹ 27,000. |

| 2 | Money deposited into bank ₹ 2,00,000 |

| 3 | Bought furniture from M/s Jayalakshmi Furniture for ₹ 28,000 on credit. |

| 4 | Purchased goods from Asohan for ₹ 5,000 by paying through debit card. |

| 5 | Purchased goods from Guna and paid through net banking for cash ₹ 10,000 |

| 6 | Purchased goods from Kannan and paid through credit card ₹ 20,000 |

| 7 | Purchased goods from Shyam on credit for ₹ 50,000 |

| 8 | Bill drawn by Shyam was accepted for ₹ 50,000 |

| 9 | Paid half the amount owed to M/s Jayalakshmi Furniture by cheque |

| 10 | Shyam’s bill was paid |