Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Journal

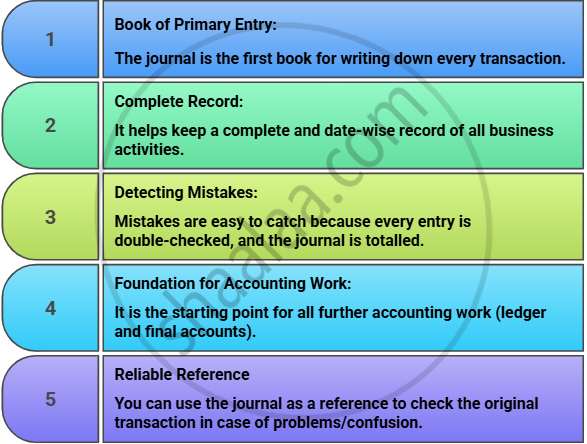

- Importance and Utility

- Format and Contents

- Example: Recording a Transaction in the Journal

- Definition: Casting

- Reasons for Casting of Journal

- Steps in Journal Casting

- Definition: Journalising

- Process of Journalising

- Key Takeaways

Definition : Journal

A journal is a book where every business transaction is recorded as soon as it happens.

Importance and Utility

Format and Contents

| Date | Particulars | L.F. | Debit Amount ₹ | Credit Amount ₹ |

|---|---|---|---|---|

|

Year |

Account debited Dr. To (Account credited) (Being...) |

xxx |

xxx |

-

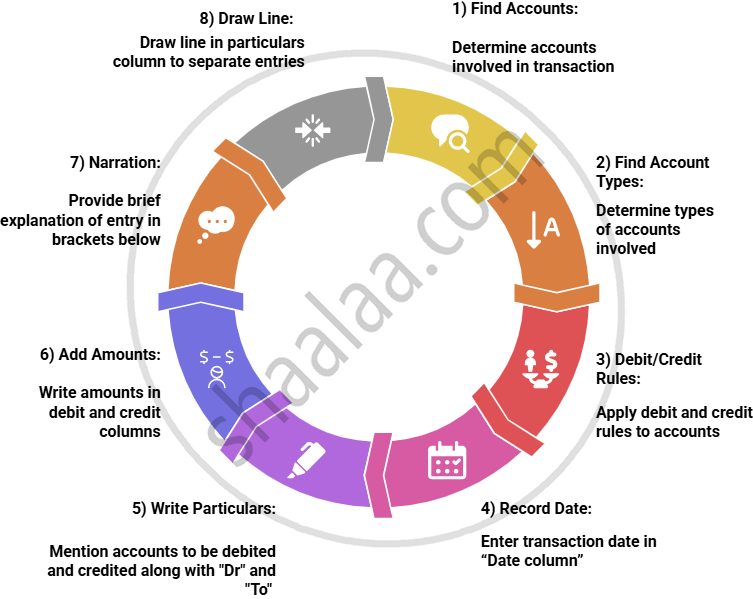

Date: The day the transaction happened.

-

Particulars: The accounts involved. Debit first, then credit with “To.”

-

L.F.: Page number in ledger (it is left blank if not posted yet).

-

Debit & Credit: Amount to be debited and credited for each account.

-

Narration: Short description of the entry inside brackets. It must start with the word "Being".

Example of a Journal Entry

Transaction: ₹5,000 rent paid in cash on 9th September, 2025

| Date | Particulars | L.F. | Debit Amount ₹ |

Credit Amount ₹ |

|---|---|---|---|---|

| 2025.09.09 | Rent A/c Dr. To Cash A/c (Being rent paid in cash) |

5,000 |

5,000 |

Definition : Casting

Casting means totalling up the amounts in the debit and credit columns of the journal—usually at the end of each page or section.

Reasons for Casting of Journal

-

You can confirm that the sum of all debits equals the sum of all credits (a basic rule in double-entry bookkeeping).

-

It is easier to detect calculation mistakes early, ensuring both sides are balanced.

Steps in Journal Casting

-

At the bottom of each journal page, write the total of all debit amounts and the total of all credit amounts.

-

If continuing to the next page, the amounts are carried forward as “Total c/f (carried forward)” and brought in as “Total b/f (brought forward)” on the new page.

-

On the final page, the “Grand Total” is written, and debits and credits must always match.

Definition : Journalising

Journalising is the process of recording business transactions in the journal as soon as they happen.

Process of Journalising

Key Takeaways

- The journal is the starting point of accounting. It helps make sure every rupee in the business is tracked, explained, and easy to find later!

-

Always record transactions from original documents like bills, receipts, or invoices—these are called source documents.

-

Every transaction will always affect at least two accounts: one is debited, and one is credited.

-

Write each journal entry with the date, accounts involved, amounts, and a short explanation (narration).

-

Totalling (casting) the journal regularly helps catch mistakes early—credits and debits should always balance.

-

Journalising means writing down each transaction in the journal in the correct format, step by step.

-

Good journal entries are important for making ledgers and final accounts later..

Related QuestionsVIEW ALL [32]

Journalise the following transactions in the books of Anand General Merchants.

| 2019 May |

|

| 1 | Mr. Anand started business with cash ₹ 60,000. |

| 5 | Purchased goods for cash ₹ 30,000. |

| 7 | Sold goods of ₹ 10,000 to Suresh. |

| 10 | Purchased Furniture from Mr. Govind on credit ₹ 30,000. |

| 15 | Paid for Rent ₹ 3000 and paid by debit card. |

| 21 | Purchased goods from Urmila on credit ₹ 70,000. |

| 27 | Paid for Transport ₹ 1,000 to United Transport. |

| 30 | Paid to Urmila ₹ 20,000 on behalf of Sharmila. |

Journalise the following transactions in the books of Anand General Merchants.

|

2019 April |

|

| 1 | Mr. Anand started the business with cash ₹ 60,000. |

| 5 | Purchased goods for cash ₹ 30,000. |

| 7 | Sold goods of ₹ 10,000 to Suresh. |

| 10 | Purchased Furniture from Mr. Govind on credit ₹ 30,000. |

| 15 | Paid for Rent ₹ 3000 and paid by debit card. |

| 21 | Purchased goods from Urmila on credit ₹ 70,000. |

| 27 | Paid for Transport ₹ 1,000 to United Transport. |

| 30 | Paid to Urmila ₹ 20,000 on behalf of Sharmila. |

Journalise the following transactions in the books of Anand General Merchants.

|

2019 |

|

| 1 | Mr Anand started business with cash ₹60,000 |

| 5 | Purchased goods for cash ₹30,000. |

| 7 | Sold goods of ₹10,000 to Suresh. |

| 10 | Purchased Furniture from Mr. Govind on credit ₹30,000. |

| 15 | Paid for Rent ₹3000 and paid by debit card. |

| 21 | Purchased goods from Urmila on credit ₹70,000. |

| 27 | Paid for Transport ₹1,000 to United Transport. |

| 30 | Paid to Urmila ₹20,000 on behalf of Sharmila. |

Journalise the following transactions in the books of Anand General Merchants.

| 2019 April | |

| 1 | Mr. Anand started business with cash ₹ 60,000 |

| 5 | Purchased goods for cash ₹ 30,000. |

| 7 | Sold goods of ₹ 10,000 to Suresh. |

| 10 | Purchased Furniture from Mr. Govind on credit ₹ 30,000. |

| 15 | Paid for Rent ₹ 3000 and paid by debit card. |

| 21 | Purchased goods from Urmila on credit ₹ 70,000 |

| 27 | Paid for Transport ₹ 1,000 to United Transport. |

| 30 | Paid to Urmila ₹ 20,000 on behalf of Sharmila. |