Topics

Introduction to Partnership and Partnership Final Accounts

- Concept of Partnership

- Partnership Deed

- Provisions of the Indian Partnership Act, 1932

- Special Aspects of Partnership Accounts> Partner's Capital Account

- Partner's Capital Account> Fixed Capital Account

- Partner's Current Account

- Partner's Capital Account> Fluctuating Capital Account

- Examples on Partners’ Capital Accounts

- Partnership Final Accounts

- Trading Account

- Profit and Loss Account

- Balance Sheet

- Adjustments in Final Account

- Examples on Partnership Final Accounts

Introduction to Partnership

Accounts of ‘Not for Profit’ Concerns

Partnership Final Accounts

- Partnership Final Accounts

- Adjustments - Income Receivable

- Interest on Capital and Current Accounts

- Adjustments - Interest on Investment and Loans

- Adjustments - Goods Destroyed by Fire Or Accident (Insured Or Uninsured)

- Adjustments - Goods Stolen

- Adjustments of Financial Statements - Goods Distributed as Free Samples and Manager's Commission

- Adjustments - Goods Withdrawn by Partners

- Adjustments - Unrecorded Purchases and Sales

- Adjustments - Capital Expenditure Included in Revenue Expenses and Vice-versa

- Adjustments - Bills Receivable Dishonoured

- Adjustments - Bills Payable Dishonoured

- Adjustments - Deferred Expenses

- Adjustments - Capital Receipts Included in Revenue Receipts and Vice-versa

- Adjustments - Commission to Working Partner Managers on the Basis of Gross Profit Net Profit, Sales, Etc

Reconstitution of Partnership (Admission of Partner)

- Reconstitution of Partnership

- Admission of Partner

- New Profit Sharing Ratio

- Sacrificing Ratio

- Admission of Partner> Accounting Treatment of Goodwill

- Average Profit Method

- Super Profit Method

- Admission of Partner> Reserves and Accumulated Profit/Losses

- Admission of Partner> Revaluation of Assets and Liabilities

- Admission of Partner> Adjustment of Capital

- Examples on Admission of Partner

Reconstitution of Partnership

- Modes of Reconstitution of a Partnership Firm

- Admission of Partner

- New Profit Sharing Ratio

- Methods of Valuation of Goodwill

- Admission of Partner> Adjustment of Capital

- Admission of Partner> Revaluation of Assets and Liabilities

- Admission of Partner> Accounting Treatment of Goodwill

- Retirement of Partner

- Needs of Retirement Or Death of a Partner

- Retirement/Death of a Partner> Treatment of Goodwill

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Retirement/Death of a Partner> New Profit Sharing Ratio

Dissolution of Partnership Firm

Reconstitution of Partnership (Retirement of Partner)

- Retirement of Partner

- Retirement/Death of a Partner> New Profit Sharing Ratio

- Retirement/Death of a Partner> Gaining Ratio

- Retirement/Death of a Partner> Treatment of Goodwill

- Hidden Goodwill

- Retirement/Death of a Partner> Reserves and Accumulated Profits/Losses

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Retirement/Death of a Partner> Adjustment of Capitals

- Computation of Amount Due to the Retiring Partner

- Payment of Amount due to Retiring Partner

- Examples on Retirement of Partner

Accounts of “Not for Profit” concerns

- Concept of Non-Profit Concerns

- Receipts and Payments Account

- Additional Information - Prepaid Expenses of the Current and Previous Year

- Additional Information - Subscription Received in Advance

- Additional Information - Subscription Outstanding of the Current and Previous Year

- Additional Information - Capitalisation of Entrance Fees

- Additional Information - Creation of Special Funds Out of Donations

- Additional Information - Stock of Stationery

- Additional Information - Opening Balances of Assets and Liabilities

- Income and Expenditure Account

Reconstitution of Partnership (Death of Partner)

- Death of Partner

- Retirement/Death of a Partner> New Profit Sharing Ratio

- Retirement/Death of a Partner> Gaining Ratio

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Determination of Amount due to the Deceased Partner

- Settlement of Amount Payable to the Deceased Partner

- Examples on Death of Partner

Single Entry System

- Concept of Single Entry System

- Statements of Affairs

- Additional Information - Additional Capital

- Effects of Adjustments-Drawings

- Concept of Depreciation

- Additional Information - Undervaluation of Assets and Liabilities

- Additional Information - Overvaluation of Assets and Liabilities

- Interest on Capital and Current Accounts

- Additional Information - Partners Salary

- Illustrations of Single Entry System

Dissolution of Partnership Firm

- Concept of Dissolution of Partnership Firm

- Difference Between Dissolution of Partnership and Dissolution of Firm

- Accounting at the Time of Dissolution of a Firm

- Types of Firm Dissolution> Simple Dissolution

- Accounting Entries To Close The Books Of Accounts

- Transfer Stage

- Realisation/Disposal Stage

- Distribution Stage

- Treatment of Unrecorded (Undisclosed) Assets and Liabilities

- Process of Dissolution> Valuation of Goodwill

- Process of Dissolution> Realisation Account

- Examples on Simple Dissolution

- Types of Firm Dissolution> Dissolution under Insolvency Situation

- When One Partner Becomes Insolvent

- When Two Partners Become Insolvent

- When All Partners Are Insolvent

Bills of Exchange

- Credit Transactions

- Concept of Bills of Exchange

- Acceptance

- Due Date

- Promissory Note

- Honouring and Dishonouring of Bill of Exchange

- Classification of Bills for Accounting

- Accounting Treatment> Retaining the Bill till the Due Date

- Accounting Treatment> Discounting the Bill of Exchange

- Accounting Treatment> Endorsement of Bill of Exchanges

- Accounting Treatment > Bills Sent to Bank for Collection

- Renewal Bill of Exchange

- Retirement of Bill under Rebate

- Insolvency of Drawee

- Examples on Bills of Exchange

Bill of Exchange (Only Trade Bill)

- Necessity of Bill of Exchange (Only Trade Bill)

- Acceptance

- Concept of Bills of Exchange

- Honouring and Dishonouring of Bill of Exchange

- Accounting Treatment> Discounting the Bill of Exchange

- Accounting Treatment> Retaining the Bill till the Due Date

- Accounting Treatment> Endorsement of Bill of Exchanges

- Accounting Treatment > Bills Sent to Bank for Collection

- Insolvency of Drawee

- Retirement of Bill under Rebate

- Accounting at the Time of Dissolution of a Firm

- Examples on Bills of Exchange

Company Accounts

- Concept of Shares

- Shareholder's Fund> Share Capital of a Company

- Private Placement of Shares

- Terms of Issue of Shares> Issue of Shares at Par

- Under Subscription of Shares

- Over Subscription of Shares

- Types of Share Issue

- Forfeiture of Shares

- Concept of Debentures

- Terms of Issue of Debentures> Issue of Debentures at Par

- Issue of Debentures for Consideration Other than Cash

- Interest on Debentures

Company Accounts - Issue of Shares

- Joint Stock Company

- Concept of Shares

- Kinds of Shares> Equity Shares

- Kinds of Shares> Preference Shares

- Shareholder's Fund> Share Capital of a Company

- Treatment of Share Capital in Balance Sheet

- Methods of Issue of Share Capital

- Terms of Issue of Shares> Issue of Shares at Par

- Terms of Issue of Shares> Issue of Shares at Premium

- Terms of Issue of Shares> Issue Shares at Discount

- Over Subscription of Shares

- Pro-rata Allotment

- Under Subscription of Shares

- Calls-In-Arrears

- Calls-In-Advance

- Issue of Shares for Consideration other than Cash

- Forfeiture of Shares

- When Shares Were Originally Issued at a Premium

- When Shares Were Originally Issued at Discount

- Reissue of Forfeited Shares

Analysis of Financial Statements

- Concept of Financial Statements

- Concept of Financial Statement Analysis

- Formats of Financial Statement Analysis

- Tools of Analysis of Financial Statements

- Comparative Financial Statement

- Comparative Balance Sheet

- Comparative Income Statement

- Common-Size Statement

- Common Size Balance Sheet

- Common-Size Income Statement

- Concept of Cash Flow Statement

- Preparation of Cash Flow Statement

- Concept of Ratio Analysis

- Current Ratios/Working Capital Ratios

- Quick Ratio/Acid Test Ratio/Liquid Ratio

- Gross Profit Ratio

- Net Profit Ratio

- Operating Profit Ratio

- Operating Ratio

- Return on Investment

- Return on Capital Employed

Analysis of Financial Statements

- Comparative Financial Statement

- Common-Size Statement

- Concept of Cash Flow Statement

- Quick Ratio/Acid Test Ratio/Liquid Ratio

- Classification of Ratios> Income Statement Ratio

- Classification of Ratios> Combined/Mixed Ratio

- ROCE

Computer In Accounting

- Introduction

- Definition: Depreciation

- Origin and Meaning of the Word “Depreciation”

- Exceptions to Depreciation

- Causes of Depreciation

- Examples: Causes of Depreciation

- Importance of Charging Depreciation

- Examples: Importance of Charging Depreciation

- Conditions for Charging Depreciation

- Depreciation vs. Provisions vs. Reserves

- Examples: Depreciation vs. Provisions vs. Reserves

- Key Takeaways

Maharashtra State Board: Class 11

Introduction

- In business, many assets like buildings, machinery, vehicles, and computers are used for several years.

- Over time, these assets lose value because of use, age, or new technology.

- This reduction in value is called depreciation.

- In accounting, depreciation means distributing the cost of an asset over the years it is used.

- Instead of recording the whole cost of a machine at once, a part of its cost is charged every year as an expense.

- This helps show the true profit of the business for each year and reflects the real value of assets on the balance sheet.

Maharashtra State Board: Class 11

Definition : Depreciation

Depreciation means a gradual decrease in the value of fixed assets like buildings, machinery, furniture, and equipment due to their use, passage of time, or technological changes.

Maharashtra State Board: Class 11

Origin and Meaning of the Word “Depreciation”

- The word “depreciation” comes from the Latin term depretiare, which means to lower in price (from “de” = down and “pretium” = price).

- Originally, it referred to the reduction in the value or price of something over time.

- In accounting, it means reducing the value of an asset every year as it’s used.

Maharashtra State Board: Class 11

Exceptions to Depreciation

Some assets do not depreciate in value. Instead, they may remain stable or even appreciate (increase in value) over time.

| Asset | Reason for Exception |

|---|---|

| Land | It does not wear out or get used up. In many cases, its value increases with demand. |

| Antiques and Artworks | Their value often increases with time due to rarity and appreciation. |

| Livestock and Plantations | These are living assets and are valued differently. |

| Assets held for investment | Such assets (like shares) are not used for operations and hence not depreciated. |

Note: Depreciation applies mainly to tangible fixed assets that have a limited useful life — like machinery, equipment, vehicles, or furniture.

Maharashtra State Board: Class 11

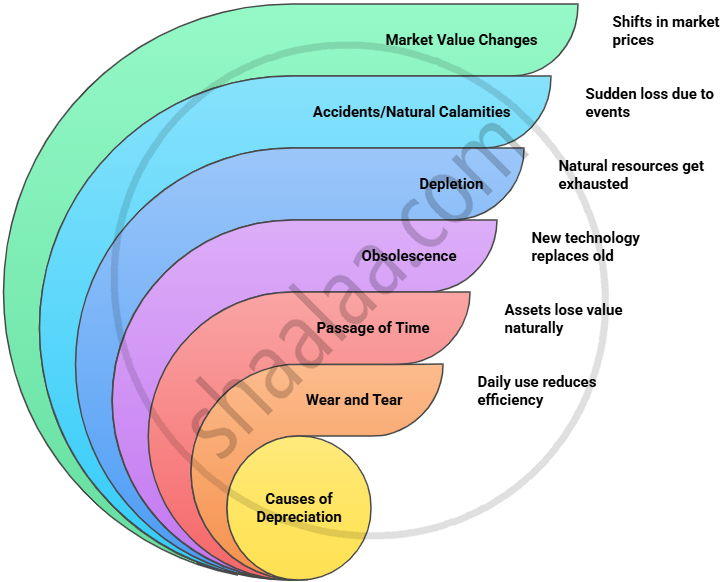

Causes of Depreciation

Maharashtra State Board: Class 11

Examples : Causes of Depreciation

| Cause | Example |

|---|---|

| Wear and Tear | Machine parts wearing out due to friction. |

| Passage of Time | Patents expiring after their term. |

| Obsolescence | Old computers replaced by faster ones. |

| Depletion | Mines, oil wells, forests. |

| Accidents/Natural Calamities | Machinery damaged in a fire. |

| Market Value Changes | Fall in land or building prices. |

Maharashtra State Board: Class 11

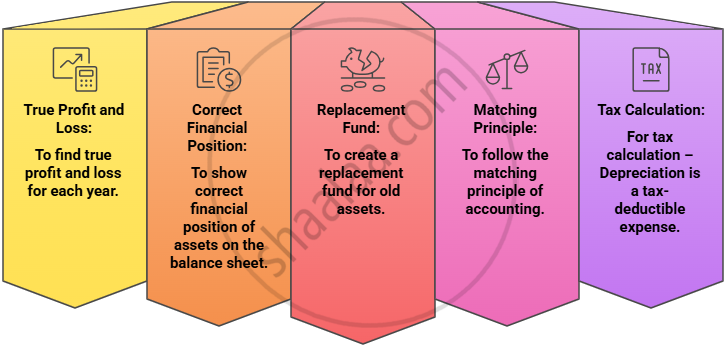

Importance of Charging Depreciation

Maharashtra State Board: Class 12

Examples : Importance of Charging Depreciation

| Point | Example |

|---|---|

| To find true profit and loss | A bakery buys an oven for ₹1,00,000. Every year, it records part of its value as an expense, so profits aren’t overstated. |

| To show correct financial position | A school's bus gets older and loses value over time. This is shown in the accounts, so assets aren’t inflated. |

| To create a replacement fund | A delivery company sets aside money by charging depreciation so it can buy new vehicles when old ones wear out. |

| To follow the matching principle | A shop uses a computer for three years. The cost is spread over three years to match the revenue earned each year. |

| For tax calculation | A factory claims depreciation as an expense, which reduces taxable income and saves on taxes. |

Maharashtra State Board: Class 11

Conditions for Charging Depreciation

| Condition | Explanation | Reason |

|---|---|---|

| The asset should have a measurable cost | Includes purchase price, transport, and installation costs. | Without knowing the cost, we can’t calculate how much value decreases over time. |

| It should have a limited useful life | It will wear out or become obsolete over time. | Only assets that eventually wear out or become outdated need depreciation. |

| The reduction in value must be permanent and gradual | Not temporary or accidental. | Depreciation is for long-term loss, not for short-term damage or one-time events. |

| Depreciation must be charged every year | Whether the business earns profit or incurs a loss. | Asset value falls every year, no matter how the business performs. |

| The asset must be used in business operations | Depreciation cannot be claimed on unused or personal assets. | Only assets used to earn business income should be depreciated. |

Maharashtra State Board: Class 12

Depreciation vs. Provisions vs. Reserves

| Basis | Depreciation | Provision | Reserve |

|---|---|---|---|

| Meaning | Fall in asset value | Amount kept for known liability | Amount from profits for general purpose |

| Type | Expense | Liability | Appropriation of profit |

| Accounting Entry | Charged to expense | Deducted before profit | Deducted after profit determination |

Maharashtra State Board: Class 12

Examples : Depreciation vs. Provisions vs. Reserves

| Concept | Example |

|---|---|

| Depreciation | A school buys a bus for ₹5,00,000. Each year, its value decreases due to use, so the school records depreciation to show the bus is getting older and less valuable. |

| Provision | A shop expects that some customers will not pay their bills. Each year, it sets aside money (provision for bad debts) to cover these possible losses. |

| Reserve | After earning profit, a business keeps aside part of it (general reserve) so they can use it later for expansion or emergencies, like opening a new branch. |

Maharashtra State Board: Class 11

Key Takeaways

- Depreciation is the gradual decrease in the value of assets like machinery or vehicles due to use, time, or technology changes.

- The word "depreciation" comes from Latin and means "to lower in price."

- Land, antiques, and investments are not depreciated because their value typically doesn’t fall with use.

- Depreciation is applied only if the asset has a measurable cost, a limited useful life, and is used in business operations, with loss in value being permanent and gradual and charged every year.

- Charging depreciation helps show true profit or loss, accurate asset values, replacement fund creation, matching cost to revenue, and proper tax calculation.

- Depreciation must be charged annually as assets lose value regardless of business performance.

- Depreciation, provision, and reserve are different: depreciation is an expense for asset value loss; provision is money set aside for expected liabilities; reserve is saved profit for future use.