Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Fixed Instalment Method

- Overview

- Advantages and Disadvantages

- Formula: When Scrap Value is Given

- Example: When Scrap Value is Given

- Formula: When Rate of Depreciation is Given

- Example: When Rate of Depreciation is Given

- Key Takeaways

Definition : Fixed Instalment Method

It is a method of depreciation where the same (fixed) amount is reduced from an asset’s value every year until it reaches its scrap value or end of life.

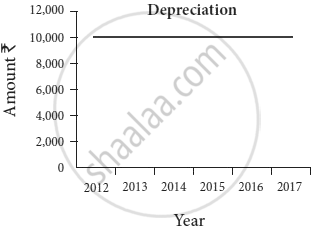

Overview

Because the depreciation amount stays constant, the graph of depreciation forms a straight line, parallel to the X-axis, as shown in the below image.

This method is also known as

-

Straight-Line Method (SLM)

-

Original Cost Method

-

Equal Instalment Method

Advantages and Disadvantages

Advantages

- Simple and easy to calculate.

- Equal charges each year make comparison of profits easy.

- Best for assets with uniform use, such as furniture, computers, and buildings.

Disadvantages

- Does not account for increasing repair costs over time.

- Unsuitable for assets that lose most of their value in early years (like vehicles).

Formula : When Scrap Value is Given

\[\mathrm{Depreciation~(p.a.)~=~\frac{Original~cost~-~Scrap~Value}{Estimated~life~of~the~asset~(in~years)}}\]

Original cost of Asset = Purchasing price of an Asset + Incidental charges, etc.

Example : When Scrap Value is Given

A machine costs ₹15,000, installation ₹3,000, scrap value ₹2,000, and estimated life = 10 years.

Depreciation = \[\frac{(15,000+3,000)-2,000}{10}\]

Formula : When Rate of Depreciation is Given

\[\text{Depreciation (p.a.)}=\frac{\text{Cost of the Asset × Rate of depreciation}}{100}\]

Note: If the asset is used for only part of the year, charge depreciation in proportion to the time used.

Example : When Rate of Depreciation is Given

A company purchased machinery for ₹80,000.

Depreciation rate = 10% p.a.

| Year | Original Cost (₹) | Depreciation (₹) | Closing Book Value (₹) |

|---|---|---|---|

| 1 | 80,000 | 8,000 | 72,000 |

| 2 | 80,000 | 8,000 | 64,000 |

| 3 | 80,000 | 8,000 | 56,000 |

| 4 | 80,000 | 8,000 | 48,000 |

Here, depreciation is constant (₹8,000) each year.

Key Takeaways

-

The Fixed Instalment Method (also called the Straight-Line or Original Cost Method) charges the same amount of depreciation every year on the original cost of an asset until its value drops to zero or scrap value.

-

This method is easy to calculate and allows easy profit comparisons since the annual charge remains constant.

-

Best suited for assets with steady usage like furniture, buildings, or computers; not ideal for assets that lose value quickly or require more repairs over time (such as vehicles).

-

The depreciation graph forms a straight horizontal line parallel to the X-axis, showing equal expense each year—hence the name Straight-Line Method.