Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Causes of Difference in Cash Book and Pass Book

- Definition: Time Difference

- Causes of Time Difference

- Possible Errors and Omissions Made by Bank or Business

- Key Takeaways

Maharashtra State Board: Class 11

Causes of Difference in Cash Book and Pass Book

Maharashtra State Board: Class 11

Definition : Time Difference

Time difference means that some transactions show up in the cash book before they appear in the passbook, or vice versa, because the bank and the account holder record them at different times.

Maharashtra State Board: Class 11

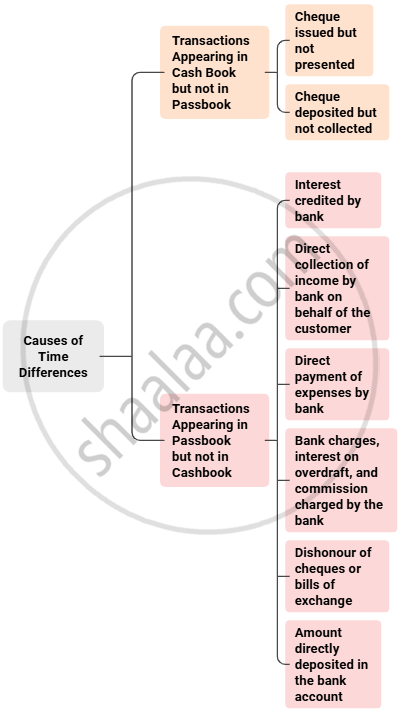

Causes of Time Difference

Explanation of Terms:

- Cheque issued but not presented: When a cheque is written and recorded in the Cash Book as payment, but the receiver has not yet taken it to the bank, so it hasn't been deducted from the passbook.

- Cheque deposited but not collected: When a cheque is received, it is immediately recorded in the cash book, but the bank takes time to collect (and clear) it, so it's not reflected in the passbook yet.

- Interest credited by bank: The bank adds interest to the account, seen in the passbook first.

- Direct collection of income by the bank on behalf of the customer: The bank collects and credits income (like dividends or refunds) straight to the passbook.

- Direct payment of expenses by bank: The bank pays bills or EMIs directly from the account, reflected in the passbook before the cashbook.

- Bank charges, interest on overdraft, and commission charged by the bank: The bank deducts charges and fees directly, so they show up in the Pass Book before the cashbook is updated.

- Dishonour of cheques or bills of exchange: If a cheque or bill that was previously credited gets dishonoured, the deduction is shown in the passbook first.

- Amount directly deposited in the bank account: Money deposited directly by someone else is recorded in the passbook before being entered in the cashbook.

Maharashtra State Board: Class 11

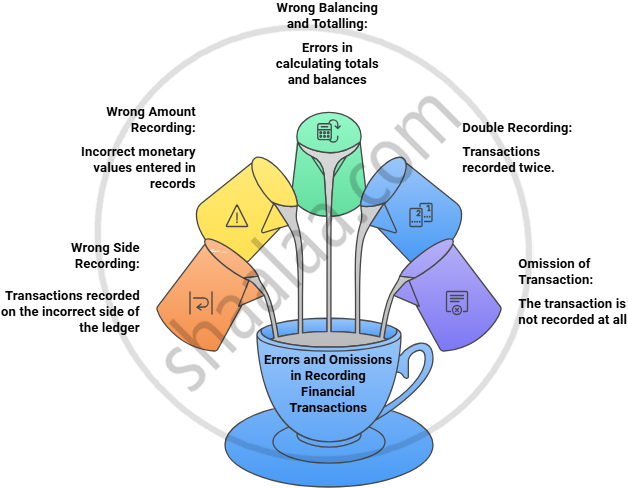

Possible Errors and Omissions Made by Bank or Business

Maharashtra State Board: Class 11

Key Takeaways

-

The cash book is maintained by the account holder to record all cash and bank transactions, while the passbook is updated by the bank to show all transactions in the account.

-

Differences between the two usually happen because transactions are recorded at different times, direct bank entries (like charges or interest), and possible mistakes or omissions by either party.

-

Regularly checking and reconciling both books helps spot any missing or incorrect entries and keeps your account records accurate.