Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Suspense Account

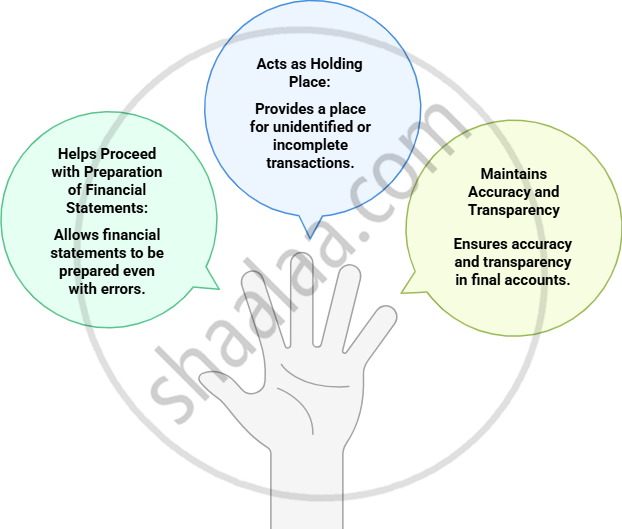

- Importance

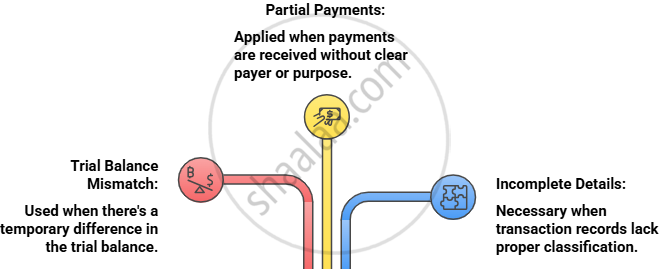

- Situations Requiring a Suspense Account

- Rules and Facts Regarding Suspense Account

- Real-life Analogy

- Example: Opening Suspense Account

- Process of Closing Suspense Account

- Key Takeaways

Maharashtra State Board: Class 11

Definition : Suspense Account

A suspense account is a temporary account created when the trial balance does not tally because of unknown errors.

Maharashtra State Board: Class 11

Importance

Maharashtra State Board: Class 11

Situations Requiring a Suspense Account

Maharashtra State Board: Class 11

Rules and Facts Regarding Suspense Account

- If credit total > debit total, the difference is placed on the debit side of the Suspense Account.

- If debit total > credit total, the difference is placed on the credit side.

- The account remains open until all one-sided errors are identified and rectified.

- Once corrections are complete, the Suspense Account automatically closes.

- The suspense account exists only till errors are corrected.

- This account never carries a balance to the next accounting year.

Maharashtra State Board: Class 11

Real-life Analogy

- Imagine a temporary locker in a shop’s cash counter — if the cashier is unsure about which department should get the money, it’s kept there temporarily until clarification.

- The Suspense Account serves this same purpose for accountants.

Maharashtra State Board: Class 11

Example : Opening Suspense Account

Transactions

-

Cash of ₹2,000 received from Ramesh was not posted to his account.

-

Purchase Returns Book was undercast by ₹400.

-

Rent of ₹1,500 paid was wrongly posted to the debit side of Rent A/c by ₹500 only.

-

Discount allowed ₹100 was not posted to the Discount Allowed A/c.

-

Wages of ₹800 paid were posted twice to the Wages A/c.

| No. | Journal Entry | Debit (₹) | Credit (₹) | Narration | Explanation |

|---|---|---|---|---|---|

| 1 | Suspense A/c Dr. | 2,000 | (Being omission of posting to Ramesh’s A/c now rectified.) |

|

|

| To Ramesh’s A/c | 2,000 | ||||

| 2 | Suspense A/c Dr. | 400 | (Being Purchase Returns Book undercast, now rectified.) |

|

|

| To Purchase Return A/c | 400 | ||||

| 3 | Rent A/c Dr. | 1,000 | (Being short debit to Rent A/c now rectified.) |

|

|

| To Suspense A/c | 1,000 | ||||

| 4 | Discount Allowed A/c Dr. | 100 | (Being omission of discount allowed now rectified.) |

|

|

| To Suspense A/c | 100 | ||||

| 5 | Suspense A/c Dr. | 800 | (Being wages posted twice to Wages A/c, now rectified.) |

|

|

| To Wages A/c | 800 |

Dr. Suspense Account Cr.

| Date | Particulars | L.F | Amount (₹) | Date | Particulars | L.F | Amount (₹) |

|---|---|---|---|---|---|---|---|

| To Ramesh’s A/c | 2,000 | By Rent A/c | 1,000 | ||||

| To Wages A/c | 800 | By Discount Allowed A/c | 100 | ||||

| To Purchase Returns A/c | 400 | By balance c/d | 2,100 | ||||

| 3,200 | 3,200 |

- Here, there is a debit balance in the suspense account, which will be posted to the trial balance to make both sides equal, temporarily.

- After rectification of errors, the trial balance will tally and the suspense account will be closed.

Maharashtra State Board: Class 11

Process of Closing Suspense Account

- All rectification entries either debit or credit the suspense account, stepwise reducing its balance with each fixing.

- Upon completion, the suspense account becomes zero, meaning every error has been properly allocated to its correct ledger.

- This process restores full accuracy and balance to the books.

Maharashtra State Board: Class 11

Key Takeaways

- A suspense account is a temporary holding account used when the trial balance does not agree or when the correct ledger for a transaction is unknown, allowing books to stay balanced while errors are found and fixed.

- It is commonly used to rectify one-sided errors, such as missing postings, undercasts, or wrong entries affecting only one side of an account.

- Correction involves passing journal entries with the suspense account as the temporary offset, and after all corrections, the suspense account’s balance becomes zero, restoring agreement in the trial balance and confirming all errors are resolved.

Test Yourself

Related QuestionsVIEW ALL [4]

From the following balances, prepare trial balance of Baskar as on 31st March, 2017. Transfer the difference, if any, to the suspense account.

| Name of the account | ₹ | Name of the account | ₹ |

| Opening stock | 40,000 | Debtors | 25,000 |

| Capital | 90,000 | Carriage inwards | 16,500 |

| Sales | 1,77,200 | Bills receivable | 20,000 |

| Salaries | 12,000 | Commission received | 5,550 |

| Bills payable | 9,450 | Cash at bank | 17,000 |

| Telephone charges | 2,350 | Furniture | 19,000 |

| Creditors | 16,000 | Plant and Machinery | 55,800 |

| Purchases | 85,000 | Repairs | 550 |