Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Tax

- Direct Tax vs. Indirect Tax

- Some Examples of Direct and Indirect Taxes in India

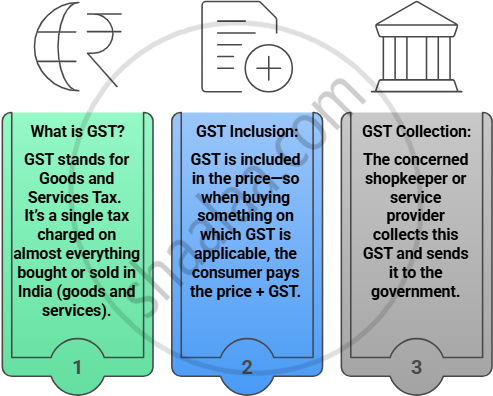

- Basics of GST

- Purpose of GST, with Examples

- Types of GST

- Example: Types of GST

- GST Rates

- Codes Used in GST, with Examples

- Key Takeaways

Notes

- Many Indirect Taxes are subsumed under GST.

- No dispute between Goods and Services.

- Statewise Registration for traders.

- GSTIN holder needs to keep all the records and should pay GST in time.

- Transparency in transactions.

- This tax system is simple and easy to understand .

- Removal of cascading effect of taxes hence the prices are controlled

- Increase in Quality of Goods and Services as they are globally competetive.

- Boost to ‘Make in India’ project.

- Technology driven tax system leads to speedy decisions.

- Goods and Service Tax system is a Dual model, as equal amount of tax is levied

by Central and State governments.

Notes

1. CGST-SGST (UTGST): Tax levied for trading within state (Intra state).

2. Composition Scheme : For those GSTIN holders whose annual turnover is between 20 lacs to 1.5 crore. They pay CGST and SGST with special rates.

3. IGST : Tax levied by central government for Inter state trading.

Maharashtra State Board: Class 11

Definition:Tax

A tax is money that people and businesses must pay to the government. The government uses this money to pay for things like schools, hospitals, roads, defense, and other public services.

Maharashtra State Board: Class 11

Direct Tax vs. Indirect Tax

| Feature | Direct Tax | Indirect Tax |

|---|---|---|

| To whom is it paid? | Paid straight to the government | Paid to

|

| Based on | What people earn (income/wealth) | What people buy or use |

| Can it be passed to others? | No, only the person earning pays | Yes, sellers add to the price, and buyers pay |

| How is it paid? | Direct payment by individual/business | Included in price of goods/services |

Maharashtra State Board: Class 11

Some Examples of Direct and Indirect Taxes in India

| Type of Tax | Example | Meaning | Where You See It in Real Life |

|---|---|---|---|

| Direct Tax | Income Tax | Tax taken from the money people earn | Family pays from salary or business income |

| Direct Tax | Property Tax | Extra payment for owning a house or land | Parents pay for owning a house |

| Direct Tax | Capital Gains Tax | Tax on profits from selling things like shares or property | Paid if someone earns profit selling property/shares |

| Indirect Tax | GST | Tax added to the price of goods/services you buy | Added to prices when shopping or eating out |

| Indirect Tax | Customs Duty | Tax charged on goods brought from other countries | Makes imported products costlier in stores |

| Indirect Tax | Excise Duty | Tax included in the price of specific items, like petrol | Increases price of petrol, alcohol, etc. |

Maharashtra State Board: Class 11

Basics of GST

Maharashtra State Board: Class 11

Purpose of GST,with Examples

| Purpose of GST | What It Means | Simple Example |

|---|---|---|

| Replace Many Old Taxes | One main tax (GST) instead of many state/central taxes like VAT, excise, service tax | Earlier, a shopkeeper paid VAT to the state and service tax to the central government; now they pay just GST. |

| One Nation, One Tax | The same tax rules everywhere in India | A pen bought in Delhi and the same pen in Chennai have the same GST. |

| Stop “Tax on Tax” (Cascading) | Tax only on added value (sales/providing services), not on previous taxes already paid | Baker pays GST on flour bought by him, then only pays GST on extra value when selling bread—not double. |

| Make Business Easier | Easier tax compliance, digital records, unified returns | A company can sell across India with one GST number and one set of forms. |

| Reduce Tax Cheating | Computerized billing so sellers can’t hide sales | All bills must clearly show GST; it's easier for the government to track taxes. |

| Boost Economy | Lower prices, more trade between states, fewer barriers | Goods move between states with less paperwork and lower costs. |

Maharashtra State Board: Class 11

Types of GST

| GST Type | Full Form | Who Charges/Collects It? | When is it Applied? | Where Does the Money Go? |

|---|---|---|---|---|

| CGST | Central Goods & Services Tax | Central Government | Sale within a state or Union Territory (UT) | Central Government |

| SGST | State Goods & Services Tax | State Government | Sale within a state (not UT) | Concerned (related) State Government |

| UTGST | Union Territory Goods & Services Tax | Union Territory Government | Sale within a Union Territory | Union Territory Government |

| IGST | Integrated Goods & Services Tax | Central Government | Sale between two states or to/from a UT | Later shared between Central Government and Destination State/UT |

Maharashtra State Board: Class 11

Example : Types of GST

| Scenario | Which GST? | Sale Value (₹) | GST Rate | Tax Split/Calculation | Who Gets How Much? |

|---|---|---|---|---|---|

| 1. Sale within a State (e.g., Gujarat to Gujarat) | CGST + SGST | 10,000 | 18% | CGST: 9% = ₹900, SGST: 9% = ₹900 | Central govt: ₹900, Gujarat govt: ₹900 |

| 2. Sale within a Union Territory (e.g., Delhi to Delhi) | CGST + UTGST | 10,000 | 18% | CGST: 9% = ₹900, UTGST: 9% = ₹900 | Central govt: ₹900, Delhi UT: ₹900 |

| 3. Sale between States (e.g., Maharashtra to Karnataka) | IGST | 10,000 | 18% | IGST: 18% = ₹1,800 (no split on invoice; Central Government later shares with destination state) | The central govt collects ₹1,800 and later shares ₹900 with Karnataka govt |

| 4. Sale from State to Union Territory (e.g., Gujarat to Delhi UT) | IGST | 10,000 | 18% | IGST: 18% = ₹1,800 | The central govt collects ₹1,800 and later shares half with Delhi UT |

How to read these examples:

- Within a state, GST is split half-half as CGST (Centre) and SGST (State).

- Within a Union Territory: GST is split as CGST (Centre) and UTGST (Union Territory).

- Between Different States or State-UT: IGST is charged as the full rate. The central government collects it first, then divides it with the state/UT where the goods finally arrive.

- How much GST: Multiply the sale value by the GST rate to get the total GST, then split as per type.

Calculation Example for Each:

- ₹10,000 sale at 18% GST within a state: 9% CGST = ₹900, 9% SGST = ₹900

- ₹10,000 sale at 18% GST within a UT: 9% CGST = ₹900, 9% UTGST = ₹900

- ₹10,000 sale at 18% GST between states/UTs: 18% IGST = ₹1,800 (shared between Centre and destination state/UT later)

Maharashtra State Board: Class 11

GST Rates

| GST Rate | Goods | Services |

|---|---|---|

| 0% | Milk, eggs, unpacked rice, fresh fruits/vegetables, children’s books, unbranded flour, salt, sanitary napkins | Educational services, basic health services |

| 5% | Tea, edible oils, domestic LPG, packed paneer, honey, train tickets, cashew, footwear (< ₹500), sugar, life-saving drugs | Public transport (rail, bus), economy hotels |

| 12% | Butter, ghee, cheese, packed coconut water, fruit juice, batteries, umbrellas, mobile phones, almonds, jam | Movie tickets (below certain price), some business consulting |

| 18% | Soaps, toothpaste, computers, printers, washing machines, ice-cream, pasta, industrial intermediaries, hair oil | Restaurants (AC/non-AC), IT services, banking services, telecom |

| 28% | Personal cars, motorcycles, AC, fridges, luxury goods, chocolates, high-end motorcycles, cigarettes | 5-star hotel stay, amusement parks, cinema (premium), gambling |

Maharashtra State Board: Class 11

Codes Used in GST,with Examples

- HSN (Harmonized System of Nomenclature) Code

| Code Type | Meaning | Example |

|---|---|---|

| HSN Code | A special number given to every kind of product/good | Pens: HSN code 9608 |

| Usage | Used on bills and by government for easy identification | Mobile, shirt |

- SAC (Services Accounting Code)

| Code Type | Meaning | Example |

|---|---|---|

| SAC Code | Special number for every service | Coaching classes: SAC 999293 |

| Usage | Helps identify and record GST for different services | Tuition, transport, legal fees |

Maharashtra State Board: Class 11

Key Takeaways

- Tax is money the government collects to pay for public services.

- Direct tax is paid straight to the government on income or property (like income tax).

- Indirect tax (like GST) is added to goods/services and paid by buyers; sellers pass it to the government.

- GST is a single indirect tax on most sales, replacing many old taxes.

- GST rates: 0%, 5%, 12%, 18%, and 28% (higher for luxuries).

- HSN/SAC codes: Number codes that help classify goods and services for GST.

- Types of GST:

- CGST: Centre, within a state

- SGST: State, within a state

- UTGST: Union territory

- IGST: For sales between states/to or from UTs