Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Importance

- Real-Life Examples

Introduction

What are Accounting Concepts?

Accounting concepts are the basic ideas or assumptions that form the foundation of accounting.

They answer the question, “What should we include in the accounts, and why?”

Think of concepts as the 'why'—the reasons for recording and reporting transactions in a certain way.

Importance

Real-Life Examples

Example of Accounting Concept

Going Concern Concept

Imagine you open a stationery shop. Even if you have not sold all your goods this year, you don’t try to sell them off quickly at a lower price by the year-end. That’s because accounting assumes your business will keep running next year and beyond. So, you record assets like stock at normal value, not at forced-sale (distress) prices.

In simple words:

We prepare accounts assuming the business will continue for the foreseeable future (near future), not close down soon.

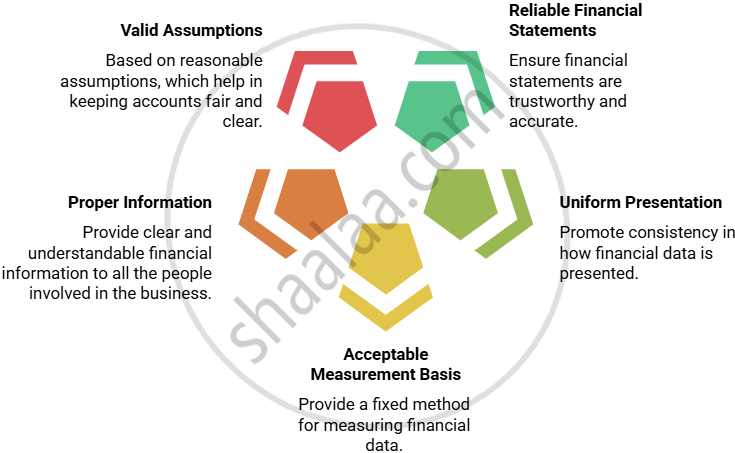

Examples on Importance of Accounting Concepts

|

Reason/Concept |

Explanation |

Example from Real Life |

|---|---|---|

|

Reliable Financial Statements |

Makes reports accurate and trustworthy. |

ABC Ltd buys a machine for ₹1,50,000. The machine is shown in the books at ₹1,50,000 (historical cost). |

|

Uniformity in Presentation |

Ensures all businesses show their accounts in the same way. |

Both Company X and Company Y use the same rules to create their balance sheets, making comparison easy. |

|

Generally Acceptable Measurement |

Uses standard methods for valuing and measuring transactions. |

All incomes and expenses are recorded in rupees (money measurement concept), not using items or hours. |

|

Proper Information for All |

Only useful and relevant information is shown to all users of financial statements. |

The business reports only business transactions, e.g., office rent paid; the owner's personal rent is excluded. |

|

Valid and Appropriate Assumptions |

Some rules are based on logic/assumptions accepted by all. |

ABC Enterprises creates accounts assuming their business will continue for the foreseeable future (going concern). |