Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Introduction

- Definition: Accounting

- Flowchart Showing Evolution of Accounting

- Stages of Evolution

- Real-Life Examples for Each Stage

- Key Takeaways

Introduction

Accounting is how people and businesses keep track of their money. It’s like keeping a diary or a notebook for all the money that comes in and goes out. Accounting helps answer questions such as:

-

How much money do we have?

-

What do we own?

-

What do we owe?

-

Are we making a profit or a loss?

Definition: Accounting

Prof. Robert N. Anthony has defined accounting as “Nearly every business enterprise has an accounting system. It is a means of collecting, summarizing, analyzing and reporting in monetary terms information about the business transactions."

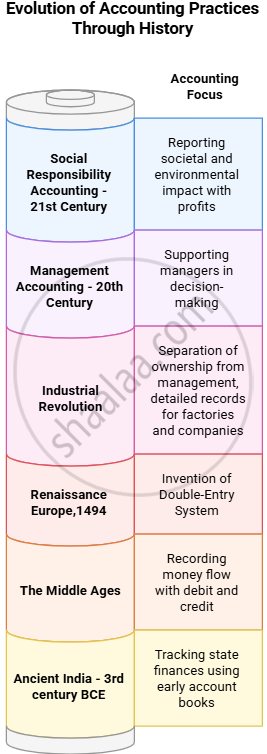

Flowchart Showing Evolution of Accounting

Stages of Evolution

1. Ancient India: Arthashastra & Early Systems

-

Who? Kautilya (Chanakya), advisor to Emperor Chandragupta Maurya (3rd century BCE).

-

What? “Arthashastra” described how to record and manage state finances.

-

How? Used early forms of account books (like "Bahi-khata") to track income and expenses.

2. Middle Ages: Agents and Bookkeeping

-

Wealthy landowners employed agents to manage property and money.

-

Records showed money “in” (credit) and “out” (debit).

-

By the 12th century, written accounts became common.

3. Renaissance Europe: Double-Entry Bookkeeping

-

Who? Luca Pacioli, “Father of Accounting” (Italy, 1494).

-

What? Developed the double-entry system—every transaction is recorded as both a debit and a credit.

-

Why? Ensures all accounts balance and reduces chances of mistakes and fraud.

4. Industrial Revolution: Companies Grow

-

Factories and joint stock companies required detailed, accurate records.

-

Large-scale business separated owners (shareholders) from managers.

-

Why? Needed reliable reports to safeguard investments and monitor company performance.

5. 20th Century: Management Accounting

-

Focus shifted to supporting managers in decision-making.

-

Included cost analysis, budgeting, and planning for business efficiency.

6. 21st Century: Social Responsibility Accounting

-

Modern companies report not only profits but also their impact on society and the environment.

-

Involves Corporate Social Responsibility (CSR) activities and transparent reporting.

Real-life Examples for Each Stage

| Stage/Era | Example |

|---|---|

| 1. Ancient India: Arthashastra & Early Systems | Imagine you keep a notebook to write down your pocket money—what you receive and spend on snacks. Ancient officials did something similar for running the kingdom. |

| 2. Middle Ages: Agents and Bookkeeping | Suppose your parents ask someone to manage the rent from several houses they own. The agent writes down what rent is collected (credit) and what is paid for repairs (debit), reporting back regularly. |

| 3. Renaissance Europe: Double-Entry Bookkeeping | You buy a book for ₹200. You record ₹200 less in your cash account (debit) and ₹200 more in your books account (credit). |

| 4. Industrial Revolution: Companies Grow | A large factory makes hundreds of products every day. The owners live in another city, so managers keep detailed records of all sales, purchases, and employee wages. This helps check profits and expenses. |

| 5. 20th Century: Management Accounting | A chocolate company calculates exactly how much it costs to make each bar so managers can decide on the best price to earn profit and minimize waste. |

| 6. 21st Century: Social Responsibility Accounting | A company keeps track of how much it spends on planting trees and supporting local schools. These figures are reported publicly, showing the business cares for society—not just making money. |

Key Takeaways

-

Accounting has evolved from simple note-keeping to complex, analytical, and socially responsible systems.

-

Double-entry book-keeping is the foundation of modern accounting.

-

As business grew, so did accounting: now it is used for financial decisions and to measure social impact.