Topics

Introduction to Book-Keeping and Accountancy

- Accounting

- Book-Keeping

- Accountancy

- Book-Keeping vs. Accountancy

- Basis (Methods) of Accounting System

- Qualitative Characteristics of Accounting Information

- Basic Terms in Accounting

- Transaction

- Capital and Drawings

- Debtors, Creditors and Bad Debts

- Expenditure and Its Types

- Discount and Its Types

- Solvent Person vs. Insolvent Person

- Accounting Year

- Trading Concerns vs. Not for Profit Concerns

- Concept of Goodwill

- Fundamentals of Business Earnings

- Concepts of Assets, Liabilities and Net Worth

- Accounting Principles

- Accounting Concepts

- Core Accounting Concepts

- Accounting Standards

Meaning and Fundamentals of Double Entry Book-Keeping

Journal

- Accounting Documents

- Goods and Service Tax(GST)

- Types of Accounting Documents

- Voucher

- Tax Invoice (Under GST)

- Credit Memo

- Receipt

- Cheque

- Types of Cheques

- Books of Accounts

- Books of Accounts > Journal

- Journal Entries

- Journal Entries > Goods Account

- Journal Entries > Recording Discount in Journal

- Journal Entries > Other Important Journal Entries

Ledger

Subsidiary Books

- Concept of Subsidiary Books

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Two Column Cash Book (With Cash and Bank Columns)

- Cash Book > Petty Cash Book

- Simple Petty Cash Book

- Analytical Petty Cash Book

- Purchase Book

- Purchase Return Book

- Sales Book

- Sales Return Book

- Journal Proper

Bank Reconciliation Statement

- Accounting Documents Used in Banking

- Accounting Documents Used in Banking

- Pay-in-Slip

- Withdrawal Slip

- Bank Pass Book

- Bank Statement

- Bank Advice

- Concept of Virtual Banking

- Bank Reconciliation Statement(BRS)

- Cash Book vs Pass Book : Causes of Differences

- Time Difference(Regarding BRS)

- Errors and Omission Made by Bank or Businessman

- Formats of BRS

- Preparation of BRS

- Cash Book and Pass Book Comparison for Common Period

- Cash Book and Pass Book Balances for Different Periods

- Bank Balance as per Cash Book (Favourable / Debit Balance)

- Bank Balance as per Pass Book (Favourable / Credit Balance)

- Overdraft as per Cash Book (Unfavourable / Credit Balance)

- Overdraft as per Pass Book (Unfavourable/Debit balance)

- Reconciliation of Debtors and Creditors

Depreciation

Rectification of Errors

Final Accounts of a Proprietary Concern

Single Entry System

- Concept of Single Entry System

- Single Entry System vs. Double Entry System

- Parts of Single Entry System

- Statements of Affairs

- Statement of Profit or Loss

- Statement of Profit or Loss > Net Worth Method

- Practical Problems on Single Entry System

- Definition: Document

- Definition: Accounting Document

- Some Common Accounting Documents

- Importance of Accounting Documents

- Steps in Recording Transactions

- Real-Life Examples

- Key Takeaways

Maharashtra State Board: Class 11

Definition : Document

A document is any paper, file, or digital record that gives information about something.

Maharashtra State Board: Class 11

Definition : Accounting Document

In accounting, a document is a paper or digital record that proves a business transaction has happened.

Maharashtra State Board: Class 11

Some Common Accounting Documents

| Document | When Used |

|---|---|

| Cash Memo | Buying/selling goods for cash |

| Receipt | Receiving money from someone |

| Invoice | Selling goods on credit |

| Cheque | Payment by bank |

| Debit Note | Returning goods to supplier |

| Credit Note | Seller accepts returned goods |

Maharashtra State Board: Class 11

Importance of Accounting Documents

| Point | Explanation |

|---|---|

| Legal Proof | They prove transactions are real and can be shown in audits or courts or to the government |

| Accurate Recording of Transactions | Only transactions with documents get recorded in the books. |

| Required by Law | Needed by certain authorities to check the collection and usage of funds by organisations. |

| Easy Reference | Kept in files for checking or solving disputes later. |

What is an Audit?

- An audit is a careful check of a company's financial records.

- The person performing an audit is called an auditor

- Its main purpose is to make sure that the company’s accounts and statements are correct, honest, and complete.

- Audits help find and prevent mistakes or fraud and build trust of owners, investors, and government officials.

Maharashtra State Board: Class 11

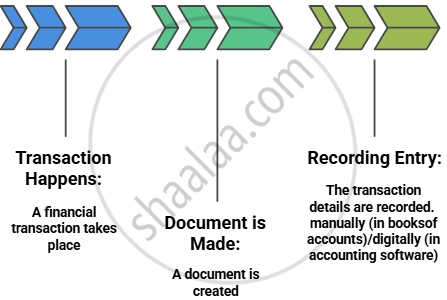

Steps in Recording Transactions

Maharashtra State Board: Class 11

Real-Life Examples

| Point/Concept | Example |

|---|---|

| Document | School report card, Aadhar card, or an electricity bill that gives you important information |

| Accounting Document | A cash memo showing the payment for a new computer |

| Importance of Accounting Documents | |

| Legal Proof | Showing a receipt in court to prove you actually paid for a service |

| Recording Transactions | Entering a rent expense in books when the landlord's rent receipt is received |

| Required by Law | A charity gives donation receipts to the charity commissioner for checking. |

| Easy Reference |

|

| Types of Accounting Documents | |

| Cash Memo | The store gives you a bill after buying shoes with cash |

| Receipt | You get a receipt when you pay your school or tuition fees |

| Invoice | The mobile store gives an invoice when you buy a phone on credit |

| Cheque | Writing a cheque to pay your hostel’s monthly rent |

| Debit Note | Returning damaged books to the supplier and sending them a debit note |

| Credit Note | Receiving a note from a supplier after returning goods purchased earlier |

| Steps in Recording Transaction |

|

Maharashtra State Board: Class 11

Key Takeaways

-

Every entry in account books is based on a document.

-

Accounting documents include memos, receipts, invoices, cheques, and notes.

-

These documents ensure accuracy, transparency, and legal safety for the business.

Related QuestionsVIEW ALL [11]

Complete the following table:

| Sr. No. | Transactions | Debit Amount (₹) | Credit Amount (₹) |

|

1 |

Paid Income Tax ₹ 5,000 by cheque | ? | Bank A/c |

| 2 | Received from Sonali ₹ 20,000 by RTGS | Bank A/c | ? |

| 3 | Sanjay became insolvent and not received ₹ 500 | ? | Sanjay A/c |

| 4 | Purchased Horse for ₹ 10,000 |

? |

Cash A/c |

| 5 | Transferred from Fixed deposit A/c of proprietor to business Bank A/c ₹ 50,000 | Bank A/c | ? |

Complete the following table:

| Reasons | When Normal balance as per Cash Book is given Add/Less | When Normal balance as per Pass Book is given Add/Less |

| 1) Interest debited in Pass Book only. | ||

| 2) Direct deposit made by customer in bank recorded in Pass Book | (+) | |

| 3) Cheque deposited into bank but not yet collected by bank | ||

| 4) Cheque deposited into bank is dishonoured | (+) | |

| 5) Cheque issued but not presented for payment. | (-) |