Advertisements

Chapters

2: Marketing and Sales

3: Advertising and Sales Promotion

4: Consumer Protection

5: E-Commerce

▶ 6: Capital and Revenue Expenditure/Income

7: Final Accounts of Sole Proprietorship

8: Fundamental Concepts of Cost

9: Budgeting

10: Sources of Finance

11: Recruitment, Selection and Trading

12: Industrial Relations, Trade Union and Social Security

13: Logistics and Insurance

14: Banking

15: Government Indicatives in Environment Protection

![Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE chapter 6 - Capital and Revenue Expenditure/Income - Shaalaa.com](/images/commercial-studies-english-class-10-icse_6:37e256b2e71b45edb2901d6e733a1c87.jpg "Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE chapter 6 - Capital and Revenue Expenditure/Income")

Advertisements

Solutions for Chapter 6: Capital and Revenue Expenditure/Income

Below listed, you can find solutions for Chapter 6 of CISCE Goyal Brothers Prakashan for Commercial Studies [English] Class 10 ICSE.

Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE 6 Capital and Revenue Expenditure/Income EXERCISES [Pages 84 - 90]

OBJECTIVE TYPE QUESTIONS

Legal expenses incurred to purchase land are ______.

Capital expenditures

Recurring expenditures

Revenue expenditures

None of these

Which of the following is a capital transaction?

Purchase of goods

Payment of wages

Sale of goods

Purchase of machinery

Expenditures incurred to acquire fixed assets are called ______.

Revenue expenditures

Prepaid expenses

Capital expenditures

Outstanding expenses

An expenditure is Revenue expenditure if ______.

It neither affects liabilities nor assets.

It either affects liabilities or assets.

Either it neither affects liabilities nor assets, or it either affects liabilities or assets.

None of these.

Capital expenditure is incurred for ______.

Acquisition of fixed assets.

Day-to-day conduct of business.

Maintaining the existing earning capacity.

All of these.

Money received by sale of machine is a ______.

Capital receipt

Revenue receipt

Deferred revenue receipt

None of these

Revenue expenditure is incurred ______.

To improve the efficiency of an asset.

To maintain the efficiency of an asset.

To buy a fixed asset.

It involves withdrawal of capital.

An expenditure is a capital expenditure when ______.

It relates to sale fixed assets.

It arises due to abnormal reasons.

It involves withdrawal of capital.

It relates to maintain the efficiency of an asset.

Period of benefit of capital expenditure is ______.

Only to the current accounting year

More than one year

One month

One weak

Premium received on issue of shares is a ______.

Capital receipt

Revenue receipt

Deferred revenue receipt

None of these

Fees and commission received for services rendered, interest and dividend received an investment are examples of ______.

Revenue receipts

Capital receipts

Deferred revenue expenditure

None of these

Carriage, freight, octroi duty, customs duty, clearing charges, dock dues, and excise duty paid on machinery are examples of ______.

Capital expenditure

Capital loss

Revenue expenditure

Revenue loss

Expenditures incurred to acquire fixed assets are called ______.

Revenue expenditures

Prepaid expenses

Capital expenditures

Outstanding expenses

This expenditure relates to normal functioning of the government departments and provision of various government services. The main examples of such expenditures are salaries, pensions, interest, subsidies, grants to the state governments, etc.

Revenue expenditure

Capital expenditure

Regular expenditure

None of these

Capital receipts are usually obtained in case of a company from:

From issue of shares, debentures

Borrowings

Sale of fixed assets or investments

All of the above

Purchased a computer for office is which type of expenditure?

Revenue expenditure

Capital expenditure

Deferred revenue expenditure

Regular expenditure

A receipt is a capital receipt:

If it satisfies any one of the two conditions: The receipts must create a liability for the government. The receipts must cause a decrease in the assets.

Borrowings are capital receipts as they lead to an increase in the liability of the government.

Both If it satisfies any one of the two conditions: The receipts must create a liability for the government. The receipts must cause a decrease in the assets, and Borrowings are capital receipts as they lead to an increase in the liability of the government.

None of these

An expenditure is Deferred revenue expenditure because ______.

Amount spent to buy assets.

The benefit of such expenditure is enjoyed by the business over a number of years.

Amount spends in investment.

None of the above.

Which of the following type of expenses are included in Revenue expenditure?

Depreciation on fixed assets

Expenses incurred for day to day running of business

Loss from sale of fixed assets

All of the above

Expenses incurred to repair a second-hand machine, purchase by the firm, to make it usable are treated under which expenditure?

Revenue

Capital

Deferred revenue

Capital loss

Which of the following type of expenses are included in capital expenditure?

Depreciation on fixed assets

Expenses incurred for day-to-day running of business

Sale of fixed assets

Raw material and stores

Rent received and commission received are examples of ______.

Capital Expenditure

Revenue Expenditure

Capital Receipts

Revenue Receipts

______ expenditure is incurred for meeting day to day expenses of business and its benefit is exhausted within the current accounting year.

Capital

Revenue

Deferred Revenue

Capital Receipts

The accounting treatment for revenue expenditure like rent paid insurance etc. is ______.

Income in Trading and Profit and Loss account.

Expense in Trading and Profit and Loss account.

Asset in the Balance Sheet.

Liability in the Balance Sheet.

______ is an example of Capital Expenditure.

Purchase of a machine

Cleaning and greasing office fans

Goods purchased for resale

Money paid as taxes

Heavy advertising expenses, heavy repairs, expenditure to move the business to a more convenient location are examples of ______.

Capital expenditure

Revenue expenditure

Deferred revenue expenditure

Capital receipts

______ involves creation of liability and is shown on the liabilities side of the balance sheet.

Capital expenditure

Revenue expenditure

Capital receipts

Revenue receipts

Non-recurring receipts like additional capital, loan, etc. are ______.

Capital receipts

Revenue receipts

Capital expenditure

Revenue expenditure

Match the Column I and Column II:

| Column - I | Column - II | ||

| (a) | Capital Expenditure | i | Repairs costing ₹ 600 carried out on a boiler. |

| (b) | Revenue Expenditure | ii | Advertising expenses ₹ 25,000 incurred for launching a new product in the market. |

| (c) | Deferred Revenue Expenditure | iii | Interest received. |

| (d) | Revenue Receipts | iv | A sum of ₹ 15,000 spent on the overhauling of a second-hand delivery van. |

(a) i, (b) ii, (c) iii, (d) iv

(a) iii, (b) ii, (c) iv, (d) i

(a) i, (b) iii, (c) iv, (d) ii

(a) iv, (b) i, (c) ii, (d) iii

Match the Column I and Column II:

| Column - I | Column - II | ||

| (a) | Preliminary expenses of ₹ 5,000 | i | Capital Expenditure |

| (b) | Purchase of old machine for ₹ 9,500 | ii | Revenue Expenditure |

| (c) | Wage paid ₹ 1,500 for carriage for goods | iii | Deferred Revenue Expenditure |

| (d) | Loan received from Banks ₹ 10,00,000 | iv | Capital Receipts |

(a) i, (b) ii, (c) iv, (d) iii

(a) i, (b) ii, (c) iii, (d) iv

(a) iii, (b) i, (c) ii, (d) iv

(a) iv, (b) iii, (c) ii, (d) i

Match the Column I and Column II:

| Column - I | Column - II | ||

| (a) | Sale of Assets | i | Capital Expenditure |

| (b) | Interest paid on loan | ii | Capital receipt |

| (c) | Purchased land | iii | Revenue expenditure |

| (d) | Interest received | iv | Revenue receipt |

(a) i, (b) ii, (c) iv, (d) iii

(a) iii, (b) iv, (c) i, (d) ii

(a) ii, (b) iii, (c) i, (d) iv

(a) iv, (b) ii, (c) i, (d) iii

______ is an example of Capital Expenditure.

Land and building

Rent

Repairs and maintenance

Interest on loan

Heavy expenditure on advertisement is classified as ______.

Revenue Expenditure

Capital Expenditure

Deferred Revenue Expenditure

Miscellaneous Expenditure

ASSERTION: Capital receipts neither create a liability nor involve a reduction in the value of fixed assets.

REASONING: Capital receipts are shown on the liabilities side of the Balance Sheet.

A is true, and R is the incorrect explanation for A.

A is true, and R is not the correct explanation for A.

A is true, but R is false.

A is false, but R is true.

Which of the following is not an example of Revenue Receipts:

- Amount received by way of loans

- Cost of overhauling second-hand machines

- Fees and commission received for services rendered

- Rent received from tenant

I & II

II & III

III & IV

I & IV

Expenses incurred for putting an asset into a working condition. Identify the type of expenditure.

Revenue Expenditure

Capital Expenditure

Revenue Receipts

Capital Receipts

Which of the following is NOT an example of Revenue Expenditure?

Research expenses.

Expenses incurred for the upkeep of fixed assets.

Expenses incurred to remove the business to a more convenient place.

Depreciation on fixed assets.

All expenses incurred on day-to-day administration of a firm and the effect of which is completely exhausted within the current accounting are called revenue receipt.

True

False

Mr. Shyam has issued shares and debentures to commence his business. Under which category will this expenditure be classified?

Revenue Expenditure

Capital Expenditure

Deferred revenue expenditure

Capital Receipts

Development costs in opening a new mine is Capital expenditure as it is incurred to develop an asset.

True

False

Cleaning and greasing office fans. It will not increase the earning capacity as it is incurred for maintaining an existing asset. Therefore, it is ______.

Revenue Expenditure

Capital Expenditure

Deferred revenue expenditure

Capital Receipts

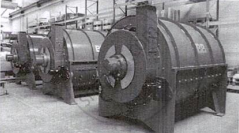

Observe the image and state the type of expenditure.

Revenue Expenditure

Capital Expenditure

Deferred revenue expenditure

Capital Receipts

Observe the given image and identify the type of receipt.

Revenue Expenditure

Capital Expenditure

Deferred revenue expenditure

Capital Receipts

Expenses incurred in connection with the purchase of land or building such as fees paid to lawyer or registration fee is Revenue expenditure.

True

False

Revenue expenditure is shown in the Trading Account or Profit and Loss Account.

True

False

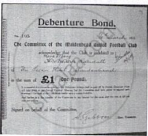

Observe the image and identify the type of Capital/Revenue item.

Revenue Receipts

Capital Expenditure

Deferred Revenue Expenditure

Capital Receipts

ASSERTION: Capital receipts are shown in the Profit and Loss account.

REASONING: Capital expenditure is shown in the Balance Sheet.

A is true, and R is the correct explanation for A.

A is true, and R is not the correct explanation for A.

A is true, but R is false.

A is false, but R is true.

If Carriage and Freight expenses are paid on the transportation of a newly acquired fixed asset, these are treated as capital expenditure.

True

False

Observe the image and state the reason why it is Capital Expenditure.

As it is incurred for maintaining an existing asset.

As there is an increase in the value of a fixed asset.

It is incurred for erection of a fixed asset.

It results in increasing the working life of the plant.

ASSERTION: Painting and lettering the new office car is Capital expenditure.

REASONING: A replacement engine fitted to the delivery van is Revenue expenditure.

A is true, and R is the correct explanation for A.

A is true, and R is not the correct explanation for A.

A is true, but R is false.

A is false, but R is true.

Which of the following is NOT capital receipts?

- Capital raised by an issue of shares and debentures.

- Rent received from tenant.

- Amount received by way of loans.

- Interest and dividends received on investments.

II & IV

II & III

III & IV

ONLY I

Heavy expenditure on advertisement is classified as ______.

Revenue Expenditure

Capital Expenditure

Deferred Revenue Expenditure

Miscellaneous Expenditure

Sharma and Company is planning to spend 5,00,000 on advertising. Under which type of expense can it be classified?

Capital Expenditure

Revenue Expenditure

Capital Receipts

Deferred Revenue Expenditure

Expenses incurred by the firm to purchase a second-hand machine and make it ready for use, are treated as ______.

Capital Expenditure

Revenue Expenditure

Capital Receipts

Revenue Receipts

Identify the type of expenditure incurred in building temporary huts for workers engaged in construction of a factory building.

Revenue Expenditure

Deferred Revenue Expenditure

Capital Expenditure

Capital Receipts

ASSERTION(A): Capital expenditure increases the earning capacity of the business.

REASON(R): Capital expenditure is incurred for day-to-day conduct of the business.

A is true, and R is the correct explanation of A.

A is true, but R is not the correct explanation of A.

A is true, but R is false.

A is false, but R is true.

SHORT ANSWER QUESTIONS

Define capital expenditure.

Give four examples of capital expenditure.

What is meant by Revenue Expenditure?

What is meant by Deferred Revenue Expenditure?

Give six examples of revenue expenditure becoming capital expenditure.

Write a short note on revenue receipts.

Distinguish between Capital Expenditure and Revenue Expenditure.

Distinguish between Capital Receipts and Revenue Receipts.

Define capital expenditure.

Define Capital receipts.

LONG ANSWER QUESTIONS

Why is it necessary to differentiate between capital and revenue items in accounting?

Give four examples of capital expenditure.

Give five examples of revenue expenditure.

What is meant by Deferred Revenue Expenditure?

How is deferred revenue expenditure treated in accounts? Give examples.

Distinguish between Capital Expenditure and Revenue Expenditure.

“Whether an expenditure is of a revenue or capital nature is a question of fact and must depend on the circumstances of each case.” Comment, giving appropriate examples.

A portion of this type of expenditure is debited to the Profit and Loss Account in the current year, and the remaining portion is shown as an asset in the Balance Sheet.

Identify the type of expenditure. Give two examples.

Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE 6 Capital and Revenue Expenditure/Income PRACTICAL PROBLEMS [Pages 90 - 91]

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

₹ 20,000 spent on dismantling, removing and reinstalling plant and machinery.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Legal expenses ₹ 5,000 on defending a suit for breach of contract to supply goods.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Premium ₹ 8,000 given for a lease.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

₹ 10,000 paid as commission on the issue of debentures.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Temporary huts built at a cost of ₹ 3,000 for construction of factory buildings. The huts were demolished when the factory building was ready.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

₹ 15,000 paid for obtaining a mortgage.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Preliminary expenses.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Replacement of old machine by a new one.

Classify the following into Capital, Revenue and Deferred Revenue Expenditures, reasons for your answer.

Wage paid for extension of office premises.

State whether the following expense is Capital or Revenue.

Cost of raising a loan.

State whether the following expense is Capital or Revenue.

Excise duty paid to the Government.

State whether the following expense is Capital or Revenue.

Charges paid for registration of a trade mark.

State whether the following expense is Capital or Revenue.

Commission paid to agents.

State whether the following expense is Capital or Revenue.

Legal expenses incurred for defending a suit of income tax.

State whether the following expense is Capital or Revenue.

Purchase of postage and stationery.

State whether the following expense is Capital or Revenue.

Purchase of typewriters for resale.

State whether the following expense is Capital or Revenue.

Interest paid on bank overdraft.

State whether the following expense is Capital or Revenue.

Fire insurance premium on premises.

State whether the following expense is Capital or Revenue.

Purchase of a computer for the office.

Classify the following into Capital and Revenue receipts.

₹ 18,000 received from the sale of old office furniture.

Classify the following into Capital and Revenue receipts.

Insurance claim received for ₹ 13,500 for damages to machinery.

Classify the following into Capital and Revenue receipts.

Commission received for ₹ 2,500 by a real estate agent.

Classify the following into Capital and Revenue receipts.

Income tax refund received for ₹ 11,250 from tax authority.

Classify the following into Capital and Revenue receipts.

Government grant received for ₹ 1,50,000 for setting up a new factory.

Classify the following into Capital and Revenue receipts.

₹ 30,000 received from issuing equity shares.

Classify the following into Capital and Revenue receipts.

₹ 5,000 interest earned on a fixed deposit with a bank.

Classify the following into Capital and Revenue receipts.

Loan received from a financial institution to expand the business.

Classify the following into Capital and Revenue receipts.

Rental income received from a property owned and leased out to tenants.

Classify the following into Capital and Revenue receipts.

Amount received from the sale of a patent for a new technology.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

A sum of ₹ 40,000 was spent on a machine consisting of ₹ 30,000 for increasing its production capacity, ₹ 1,000 for repairs and ₹ 9000 for replacement of worn-out parts.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

A new machine is purchased for ₹ 25,000, ₹ 500 are spent on its carriage and ₹ 1,500 were paid as wages for its installation.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

₹ 5,000 paid as brokerage and ₹ 2,500 other expenses on issue of shares.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

Furniture of the book value of ₹ 15,000 was sold off at ₹ 10,000. New furniture was purchased for ₹ 20,000, and ₹ 100 was paid as cartage on it.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

A total expenditure of ₹ 50,000 was incurred on factory buildings, out of this 20% related to repairs and 80% related to extensions.

In the following case, indicate the amount to be debited as Capital Expenditure and Revenue Expenditure:

Second hand motor van worth ₹ 60,000 was purchased and repairing of this cost ₹ 8,000.

Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE 6 Capital and Revenue Expenditure/Income QUESTION BANK [Pages 91 - 93]

Define capital expenditure.

Give four examples of capital expenditure.

Define Capital receipts.

Give two examples of Capital receipts.

Give two examples of deferred revenue expenditure.

Give three examples of Revenue receipts.

Give one example of Capital Profit.

Classify the following into capital expenditure and revenue expenditure.

Wages paid for installation of a machine.

Classify the following into capital expenditure and revenue expenditure.

Money spent on incorporation of a company.

Classify the following into capital expenditure and revenue expenditure.

Money spent on overhauling of office van.

Classify the following into capital expenditure and revenue expenditure.

Repairs of office furniture.

Classify the following into capital expenditure and revenue expenditure.

Insurance premium of office building.

Classify the following into capital expenditure and revenue expenditure.

Travelling expenses paid to salesman.

Why is it necessary to differentiate between capital and revenue items in accounting?

Distinguish, with the help of example between Capital Losses and Revenue Losses.

Explain the rules for deciding whether any expenditure is of a capital or a revenue nature.

Give five examples of revenue expenditure.

Capital expenditure means the expenditure the benefit of which is not exhausted within the current year. Give examples.

Capital raised by an issue of shares and debentures is considered as Capital receipts. Justify this statement

Distinguish between Capital Receipts and Revenue Receipts.

Solutions for 6: Capital and Revenue Expenditure/Income

Goyal Brothers Prakashan solutions for Commercial Studies [English] Class 10 ICSE chapter 6 - Capital and Revenue Expenditure/Income

Shaalaa.com has the CISCE Mathematics Commercial Studies [English] Class 10 ICSE CISCE solutions in a manner that help students grasp basic concepts better and faster. The detailed, step-by-step solutions will help you understand the concepts better and clarify any confusion. Goyal Brothers Prakashan solutions for Mathematics Commercial Studies [English] Class 10 ICSE CISCE 6 (Capital and Revenue Expenditure/Income) include all questions with answers and detailed explanations. This will clear students' doubts about questions and improve their application skills while preparing for board exams.

Further, we at Shaalaa.com provide such solutions so students can prepare for written exams. Goyal Brothers Prakashan textbook solutions can be a core help for self-study and provide excellent self-help guidance for students.

Concepts covered in Commercial Studies [English] Class 10 ICSE chapter 6 Capital and Revenue Expenditure/Income are Distinction Between Capital and Revenue Receipts, Meaning of Capital Loss and Revenue Loss, Meaning of Capital Profit and Revenue Profit, Basic Terms in Accounting, Expenditure and Its Types, Distinction Between Capital and Revenue Receipts, Meaning of Capital Loss and Revenue Loss, Meaning of Capital Profit and Revenue Profit, Basic Terms in Accounting, Expenditure and Its Types.

Using Goyal Brothers Prakashan Commercial Studies [English] Class 10 ICSE solutions Capital and Revenue Expenditure/Income exercise by students is an easy way to prepare for the exams, as they involve solutions arranged chapter-wise and also page-wise. The questions involved in Goyal Brothers Prakashan Solutions are essential questions that can be asked in the final exam. Maximum CISCE Commercial Studies [English] Class 10 ICSE students prefer Goyal Brothers Prakashan Textbook Solutions to score more in exams.

Get the free view of Chapter 6, Capital and Revenue Expenditure/Income Commercial Studies [English] Class 10 ICSE additional questions for Mathematics Commercial Studies [English] Class 10 ICSE CISCE, and you can use Shaalaa.com to keep it handy for your exam preparation.