Topics

Introduction to Micro and Macro Economics

- Branches of Economics

- Father of Econometrics: Ragnar Frisch

- Microeconomics

- Macroeconomics

- Macroeconomics Vs Microeconomics

Micro Economics

Introduction to Micro Economics

- Analysis of Market Structure

- Microeconomics

- Micro Economics - Slicing Method

- Use of Marginalism Principle in Micro Economics

- Micro Economics - Price Theory

- Micro Economic - Price Determination

- Micro Economics - Working of a Free Market Economy

- Micro Economics - International Trade and Public Finance

- Welfare Economics

- Micro Economics - Useful to Government

- Assumption of Micro Economic Analysis

Consumers Behavior

Analysis of Demand and Elasticity of Demand

Analysis of Supply

Types of Market and Price Determination Under Perfect Competition

Factors of Production

- Factors of Production - Feature of Capital

- Factors of Production

Macro Economics

Utility Analysis

- Basic Concepts of Microeconomics > Utility

- Commodities and Their Specific Utility for Individuals

- Total Utility and Marginal Utility

- Law of Diminishing Marginal Utility

- Paradox of Value

- Relationship Between Marginal Utility and Price

- Indifference Curve Analysis by Hicks and Allen

Introduction to Macro Economics

- Macroeconomics

- Allocation of Resource and Economic Variable

National Income

Determinants of Aggregates

- Total Demand for Good and Services

- Concept of Aggregate Demand and Aggregate Supply

- Consumption

- Investment Demand

- Government Demand

- Foreign Demand

- Difference Betweeen Export and Import

- Effect of Population of Consumption Expediture

- Types of Investment Expenditure

- Micro Eco-Equilibrium

Money

- Concept of Money

- Functions of Money

- Standard of Deferred Payment

- Standard of Transfer Payment

- Money - Store of Value

- Barter system

- Monetary Payments

- Concept of Good Money

Commercial Bank

Central Bank

- Central Bank

- Central Bank Function - Banker's Bank

- Central Bank as a Controller of Credit

- Monetary Function of Central Bank

- Non Monetary Function of Central Bank

- Methods of Credit Control

- Repo Rate and Reverse Repo Rate

- Central Bank Function - Goverment Bank

Public Economics

- Introduction of Public Economics

- Features of Public Economics

- Government Budget

- Objectives of Government Budget

- Features of Government Budget

- Public Economics - Budget (1 Year)(1 April to 31 March)

- Types of Budget

- Taxable Income

- Budgetary Accounting in India

- Budgetary Accounting - Consolidated , Contingency and Public Fund

- Components (Structure) of the Government Budget

- Factor Influencing Government Budget

Demand Analysis

- Concept of Demand

- Demand Schedule

- Individual Demand Schedule

- Market Demand Schedule

- Demand Curve

- Individual Demand Curve

- Market Demand Curve

- Reasons for the Downward Slope of the Demand Curve

- Types of Demand

- Determinants of Demand

- Law of Demand

- Exceptions to the Law of Demand

- Variations in Demand

- Changes in Demand

Elasticity of Demand

- Concept of Elasticity of Demand

- Types of Elasticity of Demand > Income Elasticity

- Types of Elasticity of Demand > Cross Elasticity

- Types of Elasticity of Demand > Price Elasticity

- Perfectly Elastic Demand

- Perfectly Inelastic Demand

- Unitary Elastic Demand

- Relatively Elastic Demand

- Relatively Inelastic Demand

- Methods of Measuring Price Elasticity of Demand

- Linear Demand Curve

- Non-Linear Demand Curve

- Factors Influencing the Elasticity of Demand

- Importance of Elasticity of Demand

- Determinants of Price Elasticity of Demand

Supply Analysis

- Concept of Supply

- Concept of Total Output

- Concept of Stock

- Distinguish between Stock and Supply

- Supply Schedule

- Individual Supply Schedule

- Market Supply Schedule

- Determinants of Supply

- Law of Supply

- Variations in Supply

- Changes in Supply

- Cost Concepts > Total Costs

- Cost Concepts > Average Cost

- Cost Concepts > Marginal Cost

- Revenue Concepts

- Total Revenue

- Average Revenue

- Marginal Revenue

Forms of Market

- Concept of Market

- Classification of Market > Based on Place

- Classification of Market > Based on Place

- Classification of Market > Based on Time

- Classification of Market > Based on Competition

- Perfect Competition

- Price Determination Under Perfect Competition

- Imperfect Competition

- Monopoly

- Concept of Monopsony

- Oligopoly

- Monopolistic Competition

Index Numbers

- Index Numbers

- Features of Index Numbers

- Types of Index Numbers

- Index Numbers Used by Government of India

- Significance of Index Numbers

- Rebasing of GDP, IIP, and WPI

- Construction of Index Numbers

- Methods of Constructing Index Numbers > Simple Index Number

- Price Index Number

- Quantity Index Number

- Value Index Number

- Methods of Constructing Index Numbers > Weighted Index Number

- Laaspeyre’s Price Index Number

- Paasche’s Price Index Number

- Concepts of Sensex and Nifty

- Crops in India's Agricultural and Industrial Production Index

- Limitations of Index Numbers

National Income

- Concept of National Income

- Features of National Income

- Circular Flow of National Income

- Two Sector Model of Circular Flow of National Income

- Three Sector Model of Circular Flow of National Income

- Four Sector Model of Circular Income

- Different Concepts of National Income

- Concept of Green GNP

- Methods of Measurement of National Income

- Output Method/Product Method

- Income Method

- Expenditure Method

- Concept of Mixed income

- Difficulties in the Measurement of National Income

- Importance of National Income Analysis

Public Finance in India

- Public Finance

- Difference Between Public Finance and Private Finance

- Structure of Public Finance > Public Expenditure

- Important Social Welfare Schemes by the Government

- Structure of Public Finance > Public Revenue

- Public Revenue > Taxes

- Types of Taxes

- Direct Tax

- Indirect Tax

- Public Revenue > Non-tax Revenue

- Structure of Public Finance > Public Debt

- Structure of Public Finance > Fiscal Policy

- Structure of Public Finance > Financial Administration

- GST(Economics)

- Government Budget

- Revenue and Capital Budgets

- Types of Budget

- Importance of Budget

Money Market and Capital Market in India

- Concept of Financial Market

- Money Market

- Structure of Money Market in India > Organized Sector

- Structure of Money Market in India > Organized Sector

- Reserve Bank of India (RBI)

- Commercial Banks

- Co-operative Banks

- Development Financial Institutions (DFIs)

- Discount and Finance House of India (DFHI)

- Structure of Money Market in India > Unorganized Sector

- Money Market

- Role of Money Market in India

- Problems of the Indian Money Market

- Reforms Introduced in the Money Market

- Recent Developments in Banking Sector

- Capital Market

- Structure of Capital Market in India

- Role of Capital Market in India

- Problems of the Capital Market

- Regional Stock Exchanges in India

- Reforms Introduced in the Capital Market

- Economic Policy in an Economy

Foreign Trade of India

- India’s Trade Relations Before 1947

- Internal Trade

- Foreign Trade of India

- Types of Foreign Trade

- Role of Foreign Trade

- India’s Recent Trade Relations with China and Japan

- Composition of India’s Foreign Trade

- India’s Foreign Trade Share in GNI

- Composition of India's Imports

- Composition of India's Exports

- Direction of India’s Foreign Trade

- Trends in India’s Foreign Trade since 2001

- Concept of Balance of Payments

- Balance of Trade

- Member Nations of OPEC and OECD

- Meaning of price determination under perfect competition

- Marshall’s scissors analogy

- Example: Demand and supply schedule for apples

- Diagram: equilibrium price with demand and supply

- Total demand and total supply

- Table: equilibrium between demand and supply

- Equilibrium price of firm and industry under perfect competition

- Key Points: Price Determination Under Perfect Competition

CISCE: Class 12

Meaning of price determination under perfect competition

- In perfect competition, the price of a commodity is determined by the interaction of market demand and market supply.

- The price at which quantity demanded is exactly equal to quantity supplied is called the equilibrium price.

- At the equilibrium price, both buyers and sellers are satisfied and there is no tendency for the price to rise or fall.

CISCE: Class 12

Marshall’s scissors analogy

- Alfred Marshall explained price determination with the example of a pair of scissors.

- A cloth can be cut only when both blades of the scissors work together.

- Similarly, price in the market is determined by both demand and supply; it is useless to ask which one is “more important”.

- Sometimes demand may play a bigger role (for example, when tastes or incomes change quickly), and at other times supply may play a bigger role (for example, when the cost of production changes).

- Therefore, both demand and supply together determine the equilibrium price.

CISCE: Class 12

Example: Demand and supply schedule for apples

| Price per kg of apples (₹) | Quantity demanded (kg) | Quantity supplied (kg) | Relationship between DD and SS |

|---|---|---|---|

| 100 | 5000 | 1000 | DD > SS |

| 200 | 4000 | 2000 | DD > SS |

| 300 | 3000 | 3000 | DD = SS |

| 400 | 2000 | 4000 | DD < SS |

| 500 | 1000 | 5000 | DD < SS |

Interpretation

- As price rises from ₹100 to ₹200, quantity demanded falls (from 5000 kg to 4000 kg) and quantity supplied rises (from 1000 kg to 2000 kg).

- At the price of ₹300, quantity demanded and quantity supplied are both 3000 kg, so ₹300 is the equilibrium price and 3000 kg is the equilibrium quantity.

- At prices above ₹300 (₹400, ₹500), supply is greater than demand (excess supply).

- At prices below ₹300 (₹100, ₹200), demand is greater than supply (excess demand).

CISCE: Class 12

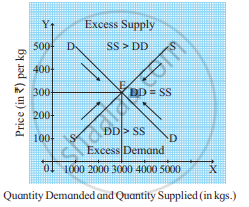

Diagram: equilibrium price with demand and supply

- On the X‑axis: quantity of apples.

- On the Y‑axis: price per kg of apples.

- DD is a downward‑sloping demand curve, showing an inverse relationship between price and quantity demanded.

- SS is an upward‑sloping supply curve, showing a direct relationship between price and quantity supplied.

- The curves intersect at point E.

At E, the equilibrium price = ₹300 and the equilibrium quantity = 3000 kg.

At any price above E, there is excess supply.

At any price below E, there is excess demand. - Market forces push the price towards this intersection point E.

CISCE: Class 12

Total demand and total supply

Total demand (market demand)

- Demand means the quantity of a commodity that consumers are willing and able to buy at different prices during a given period.

- Each unit of a commodity has a “demand price”, the price at which it can be sold to some buyer.

- Other things being equal, when price falls, quantity demanded increases; when price rises, quantity demanded decreases.

- A fall in price:

i. induces existing buyers to buy more,

ii. brings in new buyers, and

iii. may create substitution and income effects.

Total supply (market supply)

- Supply means the quantity of a commodity that producers are willing to offer for sale at different prices during a given period.

- It is not the total stock but only the part that producers are ready to sell at given prices.

- Each unit of a commodity has a “supply price”, the price at which it is offered for sale.

- Other things being equal, when price rises, quantity supplied increases; when price falls, quantity supplied decreases.

CISCE: Class 12

Table: equilibrium between demand and supply

| Price (₹) | Quantity demanded | Quantity supplied | Situation |

|---|---|---|---|

| 5 | 12 | 1 | Excess demand |

| 10 | 10 | 2 | Excess demand |

| 15 | 8 | 4 | Excess demand |

| 20 | 6 | 6 | Equilibrium (D = S) |

| 25 | 4 | 8 | Excess supply |

| 30 | 2 | 10 | Excess supply |

| 35 | 1 | 12 | Excess supply |

Explanation

- At price ₹20, quantity demanded = quantity supplied = 6 units → equilibrium price and equilibrium quantity.

- If the price is above ₹20, say ₹25:

i. Buyers demand only 4 units but sellers supply 8 units (excess supply).

ii. Sellers compete among themselves to sell, so the price falls towards ₹20. - If the price is below ₹20, say ₹15:

i. Buyers demand 8 units but sellers supply only 4 units (excess demand).

ii. Buyers compete among themselves to buy, so the price rises towards ₹20. - Thus, price adjusts until demand equals supply, and equilibrium is reached.

CISCE: Class 12

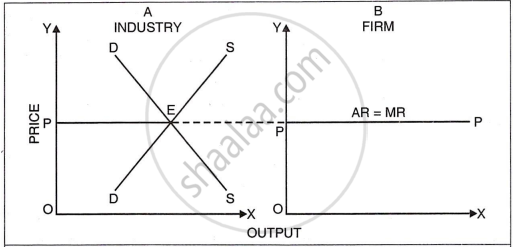

Equilibrium price of firm and industry under perfect competition

Industry equilibrium

- In perfect competition, the industry (all firms together) determines the market price by the intersection of market demand and market supply.

- In Fig. 2, the industry demand curve DD and supply curve SS intersect at point E, giving equilibrium price OP.

Firm’s price under perfect competition

- Under perfect competition, each individual firm is a price taker, not a price maker.

- In Fig. 2, the firm faces a horizontal demand curve at price OP.

- The firm can sell any quantity of its output at price OP but cannot charge more or less than OP.

- The firm’s demand curve is also its average revenue (AR) and marginal revenue (MR) curve under perfect competition.

Maharashtra State Board: Class 12

CISCE: Class 12

CISCE: Class 12

Key Points: Price Determination Under Perfect Competition

- Price under perfect competition is determined by the interaction of market demand and market supply.

- Equilibrium price is the price at which quantity demanded equals quantity supplied; equilibrium quantity is the corresponding quantity.

- At prices above equilibrium, there is excess supply and price tends to fall.

- At prices below equilibrium, there is excess demand and the price tends to rise.

- Marshall compared demand and supply to the two blades of a pair of scissors; both are essential for price determination.

- In perfect competition, the industry determines the price, and each firm is a price taker and must accept that price.

Test Yourself

Related QuestionsVIEW ALL [3]

Observe the following table and answer the questions:

| Price of a banana (per dozen) in ₹ | Demand (in dozen) | Supply (in dozen) | Relation between DD and SS |

| 10 | 500 | 100 | DD > SS |

| 20 | 400 | _____ | DD > SS |

| 30 | _____ | 300 | DD = SS |

| 40 | 200 | _____ | DD < SS |

| 50 | ______ | 500 | DD < SS |

- Fill in the blanks in the above schedule.

- Derive the equilibrium price from the above schedule with the help of a suitable diagram.