Topics

Introduction to Partnership and Partnership Final Accounts

- Concept of Partnership

- Partnership Deed

- Provisions of the Indian Partnership Act, 1932

- Special Aspects of Partnership Accounts> Partner's Capital Account

- Partner's Capital Account> Fixed Capital Account

- Partner's Current Account

- Partner's Capital Account> Fluctuating Capital Account

- Examples on Partners’ Capital Accounts

- Partnership Final Accounts

- Trading Account

- Profit and Loss Account

- Balance Sheet

- Adjustments in Final Account

- Examples on Partnership Final Accounts

Introduction to Partnership

Accounts of ‘Not for Profit’ Concerns

Partnership Final Accounts

- Partnership Final Accounts

- Adjustments - Income Receivable

- Interest on Capital and Current Accounts

- Adjustments - Interest on Investment and Loans

- Adjustments - Goods Destroyed by Fire Or Accident (Insured Or Uninsured)

- Adjustments - Goods Stolen

- Adjustments of Financial Statements - Goods Distributed as Free Samples and Manager's Commission

- Adjustments - Goods Withdrawn by Partners

- Adjustments - Unrecorded Purchases and Sales

- Adjustments - Capital Expenditure Included in Revenue Expenses and Vice-versa

- Adjustments - Bills Receivable Dishonoured

- Adjustments - Bills Payable Dishonoured

- Adjustments - Deferred Expenses

- Adjustments - Capital Receipts Included in Revenue Receipts and Vice-versa

- Adjustments - Commission to Working Partner Managers on the Basis of Gross Profit Net Profit, Sales, Etc

Reconstitution of Partnership (Admission of Partner)

- Reconstitution of Partnership

- Admission of Partner

- New Profit Sharing Ratio

- Sacrificing Ratio

- Admission of Partner> Accounting Treatment of Goodwill

- Average Profit Method

- Super Profit Method

- Admission of Partner> Reserves and Accumulated Profit/Losses

- Admission of Partner> Revaluation of Assets and Liabilities

- Admission of Partner> Adjustment of Capital

- Examples on Admission of Partner

Reconstitution of Partnership

- Modes of Reconstitution of a Partnership Firm

- Admission of Partner

- New Profit Sharing Ratio

- Methods of Valuation of Goodwill

- Admission of Partner> Adjustment of Capital

- Admission of Partner> Revaluation of Assets and Liabilities

- Admission of Partner> Accounting Treatment of Goodwill

- Retirement of Partner

- Needs of Retirement Or Death of a Partner

- Retirement/Death of a Partner> Treatment of Goodwill

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Retirement/Death of a Partner> New Profit Sharing Ratio

Dissolution of Partnership Firm

Reconstitution of Partnership (Retirement of Partner)

- Retirement of Partner

- Retirement/Death of a Partner> New Profit Sharing Ratio

- Retirement/Death of a Partner> Gaining Ratio

- Retirement/Death of a Partner> Treatment of Goodwill

- Hidden Goodwill

- Retirement/Death of a Partner> Reserves and Accumulated Profits/Losses

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Retirement/Death of a Partner> Adjustment of Capitals

- Computation of Amount Due to the Retiring Partner

- Payment of Amount due to Retiring Partner

- Examples on Retirement of Partner

Accounts of “Not for Profit” concerns

- Concept of Non-Profit Concerns

- Receipts and Payments Account

- Additional Information - Prepaid Expenses of the Current and Previous Year

- Additional Information - Subscription Received in Advance

- Additional Information - Subscription Outstanding of the Current and Previous Year

- Additional Information - Capitalisation of Entrance Fees

- Additional Information - Creation of Special Funds Out of Donations

- Additional Information - Stock of Stationery

- Additional Information - Opening Balances of Assets and Liabilities

- Income and Expenditure Account

Reconstitution of Partnership (Death of Partner)

- Death of Partner

- Retirement/Death of a Partner> New Profit Sharing Ratio

- Retirement/Death of a Partner> Gaining Ratio

- Retirement/Death of a Partner> Revaluation of Assets and Liabilities

- Determination of Amount due to the Deceased Partner

- Settlement of Amount Payable to the Deceased Partner

- Examples on Death of Partner

Single Entry System

- Concept of Single Entry System

- Statements of Affairs

- Additional Information - Additional Capital

- Effects of Adjustments-Drawings

- Concept of Depreciation

- Additional Information - Undervaluation of Assets and Liabilities

- Additional Information - Overvaluation of Assets and Liabilities

- Interest on Capital and Current Accounts

- Additional Information - Partners Salary

- Illustrations of Single Entry System

Dissolution of Partnership Firm

- Concept of Dissolution of Partnership Firm

- Difference Between Dissolution of Partnership and Dissolution of Firm

- Accounting at the Time of Dissolution of a Firm

- Types of Firm Dissolution> Simple Dissolution

- Accounting Entries To Close The Books Of Accounts

- Transfer Stage

- Realisation/Disposal Stage

- Distribution Stage

- Treatment of Unrecorded (Undisclosed) Assets and Liabilities

- Process of Dissolution> Valuation of Goodwill

- Process of Dissolution> Realisation Account

- Examples on Simple Dissolution

- Types of Firm Dissolution> Dissolution under Insolvency Situation

- When One Partner Becomes Insolvent

- When Two Partners Become Insolvent

- When All Partners Are Insolvent

Bills of Exchange

- Credit Transactions

- Concept of Bills of Exchange

- Acceptance

- Due Date

- Promissory Note

- Honouring and Dishonouring of Bill of Exchange

- Classification of Bills for Accounting

- Accounting Treatment> Retaining the Bill till the Due Date

- Accounting Treatment> Discounting the Bill of Exchange

- Accounting Treatment> Endorsement of Bill of Exchanges

- Accounting Treatment > Bills Sent to Bank for Collection

- Renewal Bill of Exchange

- Retirement of Bill under Rebate

- Insolvency of Drawee

- Examples on Bills of Exchange

Bill of Exchange (Only Trade Bill)

- Necessity of Bill of Exchange (Only Trade Bill)

- Acceptance

- Concept of Bills of Exchange

- Honouring and Dishonouring of Bill of Exchange

- Accounting Treatment> Discounting the Bill of Exchange

- Accounting Treatment> Retaining the Bill till the Due Date

- Accounting Treatment> Endorsement of Bill of Exchanges

- Accounting Treatment > Bills Sent to Bank for Collection

- Insolvency of Drawee

- Retirement of Bill under Rebate

- Accounting at the Time of Dissolution of a Firm

- Examples on Bills of Exchange

Company Accounts

- Concept of Shares

- Shareholder's Fund> Share Capital of a Company

- Private Placement of Shares

- Terms of Issue of Shares> Issue of Shares at Par

- Under Subscription of Shares

- Over Subscription of Shares

- Types of Share Issue

- Forfeiture of Shares

- Concept of Debentures

- Terms of Issue of Debentures> Issue of Debentures at Par

- Issue of Debentures for Consideration Other than Cash

- Interest on Debentures

Company Accounts - Issue of Shares

- Joint Stock Company

- Concept of Shares

- Kinds of Shares> Equity Shares

- Kinds of Shares> Preference Shares

- Shareholder's Fund> Share Capital of a Company

- Treatment of Share Capital in Balance Sheet

- Methods of Issue of Share Capital

- Terms of Issue of Shares> Issue of Shares at Par

- Terms of Issue of Shares> Issue of Shares at Premium

- Terms of Issue of Shares> Issue Shares at Discount

- Over Subscription of Shares

- Pro-rata Allotment

- Under Subscription of Shares

- Calls-In-Arrears

- Calls-In-Advance

- Issue of Shares for Consideration other than Cash

- Forfeiture of Shares

- When Shares Were Originally Issued at a Premium

- When Shares Were Originally Issued at Discount

- Reissue of Forfeited Shares

Analysis of Financial Statements

- Concept of Financial Statements

- Concept of Financial Statement Analysis

- Formats of Financial Statement Analysis

- Tools of Analysis of Financial Statements

- Comparative Financial Statement

- Comparative Balance Sheet

- Comparative Income Statement

- Common-Size Statement

- Common Size Balance Sheet

- Common-Size Income Statement

- Concept of Cash Flow Statement

- Preparation of Cash Flow Statement

- Concept of Ratio Analysis

- Current Ratios/Working Capital Ratios

- Quick Ratio/Acid Test Ratio/Liquid Ratio

- Gross Profit Ratio

- Net Profit Ratio

- Operating Profit Ratio

- Operating Ratio

- Return on Investment

- Return on Capital Employed

Analysis of Financial Statements

- Comparative Financial Statement

- Common-Size Statement

- Concept of Cash Flow Statement

- Quick Ratio/Acid Test Ratio/Liquid Ratio

- Classification of Ratios> Income Statement Ratio

- Classification of Ratios> Combined/Mixed Ratio

- ROCE

Computer In Accounting

- Introduction

- Definition: Joint Stock Company

- Features

- Merits

- Demerits

- Types of Companies

- Real-Life Application

- Key Point Summary

Maharashtra State Board: Class 11

Introduction

A Joint Stock Company is a business owned by many people who each buy “shares” of ownership.

- The capital is pooled and divided into small parts called shares.

- Owners of shares are called shareholders.

- The company itself is created and governed by law.

Maharashtra State Board: Class 11

Definition: Joint Stock Company

- “A Joint Stock Company is a voluntary association of individuals for profit having capital divided into transferable Shares, the ownership of which is the condition on membership.” – Prof. L. H. Haney.

- “A Company is a person, artificial, invisible, intangible, and existing only in the eyes of the law. Being a mere creature of law, it possesses only those properties which the charter of its creation confers upon it, either expressly or as incidental to its very existence.” – Chief Justice Marshal

- According to The Companies Act 2013, Section 2 (20), the term “Company” means “a Company incorporated under the Companies Act 2013 or any previous Company law.”

Maharashtra State Board: Class 11

Features

Maharashtra State Board: Class 11

Merits

- Large amount of Capital: Many people can invest.

- Professional Management: Experts run the company affairs.

- More Scope for expansion: Easier to grow, start new projects.

- Public Confidence: Audited by law, it is easy to build confidence.

- Relief in Taxation: Sometimes, tax relaxation is provided for working in backward areas.

- Expert Services: Companies can hire professionals, such as legal advisors, auditors, and consultants.

- Perpetual Succession: The Company continues no matter what happens to shareholders.

- Limited Liability: Risk is only for the unpaid share amount.

Maharashtra State Board: Class 11

Demerits

- Rigid Formation: Many legal steps and fees.

- Lack of Secrecy: Important info must be published.

- Delay in the Decision-Making process: Too many people are involved, and meetings are lengthy.

- No Personal Contact: Owners don’t know workers/customers directly.

- High Cost of Management: Higher salaries, advertisement, and administrative costs.

- Reckless Speculation: Some directors might misuse information for personal gain.

Maharashtra State Board: Class 11

Real-Life Applications

Reliance Industries Ltd., Tata Motors Ltd., and Maruti Suzuki Ltd.

Maharashtra State Board: Class

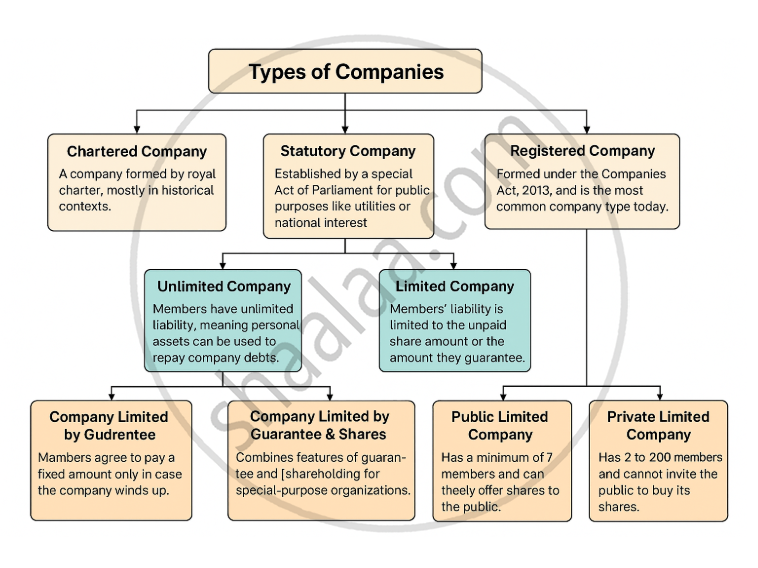

Types of Companies

Maharashtra State Board: Class 11, 12

Key Points: Joint Stock Company

- Meaning: A Joint Stock Company is a business organisation where ownership is divided into transferable shares held by shareholders.

- Origin: It emerged during the Industrial Revolution to overcome the limitations of partnerships, such as unlimited liability and limited capital, by raising funds from the public.

- Legal Status: A Joint Stock Company is an artificial legal person with a separate legal identity and perpetual succession, created under company law.

- Merits: It provides benefits like large capital, limited liability, expert management, public confidence, and better scope for expansion.

- Types: Companies can be Chartered, Statutory, or Registered, and further classified as Public, Private, Limited, or Unlimited.