Please select a subject first

Advertisements

Advertisements

What is revenue expenditure?

Concept: Classification of Expenditure

Market for a good is in equilibrium. There is simultaneous "decrease" both in demand and supply of the good. Explain its effect on market price

Concept: Market Equilibrium

Explain the chain of effects of excess supply of a good on its equilibrium price

Concept: Equilibrium Price

Explain how government budget can be helpful in bringing economic stabilization in the economy.

Concept: Objectives of Government Budget

A market for a good is in equilibrium. The supply of good "decreases". Explain the chain of effects of this change

Concept: Market Equilibrium

Giving reason, state whether the following is a revenue expenditure or a capital expenditure in a government budget:

Expenditure of building a bridge.

Concept: Classification of Expenditure

What is meant by price ceiling? Explain its implications.

Concept: Price Ceiling

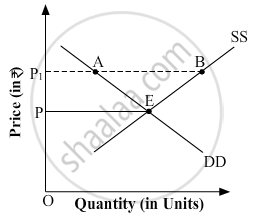

Answer the following question.

In the given diagram, OP is the market-determined price, and OP1 is the price fixed by the government.

Concept: Price Floor

Suppose the demand and supply equations of a commodity X in a perfectly competitive market are given by :

Qd = 1700 – 2P

Qs = 1300 + 3P

Calculate the value of equilibrium price and equilibrium quantity of the commodity X.

Concept: Equilibrium Price

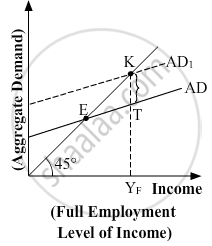

Answer the following question.

In the given figure, what does the gap 'KT' represent? State any two fiscal measures to correct the situation.

Concept: Measures of Government Deficit

Answer the following question.

Define "Trade surplus". How is it different from "Current account surplus"?

Concept: Concept of Balance of Payments >> Balance of Payments Surplus and Deficit

"Under the flexible exchange rate system, the Central Bank does not intervene in the foreign exchange market."

Justify the statement, giving valid arguments.

Concept: Determination of the Exchange Rate

Explain the impact of home currency depreciation on the exports of a nation.

Concept: Determination of the Exchange Rate

Giving valid reason, state whether the following statement is true or false:

Dividend received from investment abroad is recorded on the credit side of the capital account.

Concept: Concept of Balance of Payments >> Current Account

Giving valid reason, state whether the following statement is true or false:

Depreciation of the Indian Currency will lead to promotion of Indian exports.

Concept: Determination of the Exchange Rate

Distinguish between Autonomous transactions and Accommodating transactions.

Concept: Concept of Balance of Payments >> Balance of Payments Surplus and Deficit

Read the extract given below and answer the questions that follow:

At back of the dim class

One unnoted, sweet and young. His eyes live in a dream,

Of squirrel's game, in three room, other than this.

(a) Why is the class dim?

(b) How is the young child different from others?

(c) What is he doing?

(d) What is a tree room?

Concept: An Elementary School Classroom in a Slum

After mother Skunk and Roger Skunk return home, she hugs him before he sleeps. What does this show about mother Skunk?

Concept: Should Wizard Hit Mommy?

What impression do you form of Jack as a father? Support your answer.

Concept: Should Wizard Hit Mommy?

Describe the precautions taken by the prison officers to prevent Evans from escaping.

Concept: Evans Tries an O-level