Definitions [14]

Define the concept of demand schedule.

A tabular representation that shows the quantity of a good a consumer is willing to purchase at different prices, over a specific period of time.

Define the following concept:

Derived demand

When goods are demanded so that they can be used in the production of some other commodity, it is called indirect or derived demand.

- "The demand for anything at a given price is the amount of it which will be bought per unit of time at that price." – Prof. Benham

- "By demand, we mean the quantity of a commodity that will be purchased at a particular price and not merely the desire of a thing." – Hansen

- "The demand for a particular good is the amount that will be purchased at a given price and at a given time." – Veera Anstey

- "Want is effective desire for particular thing which expresses itself in the effort or sacrifice necessary to obtain them." – Peterson

Define joint demand.

When two or more goods are demanded together, it is called joint demand. It exists when two or more goods are required together to satisfy a particular want. Joint demand is also called complementary demand.

Define composite demand.

Demand for goods that have multiple uses is called composite demand.

Define the following concept:

Demand

Demand for a commodity refers to the quantity of a commodity that a consumer is willing and is able to purchase at a particular price at any particular point in time.

The demand for a particular good is the amount that will be purchased at a given price and at a given time.

Define decrease in demand.

When there is a fall in demand due to changes in factors other than the own price of the commodity, it is called a decrease in demand.

Define contraction of demand (or decrease in quantity demanded).

When the quantity demanded of a commodity falls due to a rise in its own price of the commodity, other factors remaining constant, it is called a contraction of demand or a decrease in the quantity demanded.

Define price elasticity of demand.

It is the measure of the degree of responsiveness of the demand for a good to the changes in its price. It is defined as the percentage change in the demand for a good divided by the percentage change in its price.

ed = `"Percentage change in demand for good"/"Percentage change in price of that good"`

ed = `(ΔQ)/(ΔP) xx P/Q`

Where ΔQ = Q2 − Q1, change in demand

ΔP = P2 − P1, change in price

P1 = Initial price

Q1 = Initial quantity

Define elasticity of demand.

Price elasticity of demand tells us the amount of the change in the quantity demanded of a commodity in response to change in its price. In other words, it measures the degree of change of demand in response to changes in price.

Define the following concept:

Cross Elasticity of Demand

Cross elasticity of demand is the measure of the responsiveness of demand for a good to a change in the price of a related good.

`"Ec" = ("Proportionate change in quantity demanded of good X")/("Proportionate change in price of good Y")`

- "Elasticity of demand may be defined as the percentage change in quantity demanded to the percentage change in price." - Alfred Marshall

- "The elasticity of demand for a commodity is the rate at which quantity bought changes as the price changes." - A.K. Cairncross

- "Elasticity of demand is a technical term used by the economists to describe the degree of respensiveness of demand of a commodity to a change in its price." -Stonier and Hague

- Elasticity of demand refers to the degree of responsiveness of quantity demanded of a commodity to a change in any of its determinants.

- "Income elasticity of demand means the ratio of the percentage change in the quantity demanded to the percentage change in income." - Watson

- "The responsiveness of demand to change in income is termed as income elasticity of demand." - R.G. Lipsey

Formulae [2]

Demand = Desire + Willingness to Buy + Ability to Pay

Ey = `"Proportionate change in Quantity Demanded"/"Proportionate change in income"`

\[E_y=\frac{\frac{\Delta Q}{Q}}{\frac{\Delta Y}{Y}}\quad=\frac{\Delta Q}{Q}\div\frac{\Delta Y}{Y}=\frac{\Delta Q}{Q}\times\frac{Y}{\Delta Y}\]

Where:

Ey = Income elasticity of demand

ΔQ = Change in the quantity demanded

Q = Initial demand

ΔY = Change in income

Y = Initial Income

Theorems and Laws [2]

State and explain the law of demand.

The law of demand was introduced by Prof. Alfred Marshall in his book, ‘Principles of Economics’, which was published in 1890. The law explains the functional relationship between price and quantity demanded.

According to Prof. Alfred Marshall, “Other things being equal, the higher the price of a commodity, the smaller is the quantity demanded, and the lower the price of a commodity, the larger is the quantity demanded.” In other words, other factors remaining constant, if the price of a commodity rises, demand for it falls; and when the price of a commodity falls, demand for it rises. Thus, there is an inverse relationship between price and quantity demanded. Symbolically, the functional relationship between demand and price is expressed as:

Dx = f (Px)

Where D = Demand for a commodity

x = Commodity

f = Function

Px = Price of a commodity

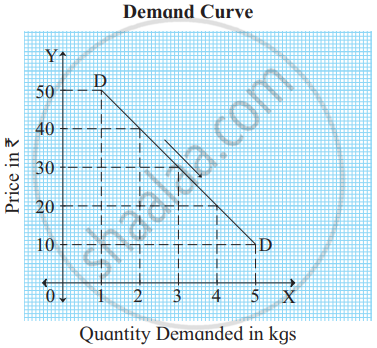

| Price of a commodity ‘x’ (₹) |

Quantity demanded of the commodity ‘x’ (in kgs.) |

| 50 | 1 |

| 40 | 2 |

| 30 | 3 |

| 20 | 4 |

| 10 | 5 |

As shown in the table, when the price of commodity ‘x’ is ₹ 50, the quantity demanded is 1 kg. When the price falls from ₹ 50 to ₹ 40, the quantity demanded rises from 1 kg to 2 kg. Similarly, at a price of ₹ 30, the quantity demanded is 3 kgs, and when the price falls from ₹ 20 to ₹ 10, the quantity demanded rises from 4 kgs to 5 kgs. Thus, as the price of a commodity falls, quantity demanded rises, and when the price of the commodity rises, quantity demanded falls. This shows an inverse relationship between price and quantity demanded.

The X-axis represents the demand for the commodity, and the Y-axis represents the price of the commodity x. DD is the demand curve, which slopes downward from left to right because price and quantity demanded are inversely related.

State and explain the ‘law of demand’ with its exceptions.

Prof. Alfred Marshall introduced the law of demand in his book, ‘Principles of Economics,’ published in 1890. The law explains the functional relationship between price and quantity demanded.

- Statement of the Law: According to Prof. Alfred Marshall, “Other things being equal, the higher the price of a commodity, the smaller the quantity demanded, and the lower the price of a commodity, the larger the quantity demanded.” Explanation: Other factors remain constant: when the price of a commodity rises, demand for it falls, and when the price of a commodity falls, demand for it rises. Thus, there is an inverse relationship between price and quantity demanded.

- Demand Schedule: The law of demand is explained with the help of the following demand schedule:

Demand Schedule Price of commodity

‘x’ (in ₹)Quantity demanded

per week (in kg)10 1 8 2 6 3 4 4 2 5 - From the above schedule, it can be observed that when the price of the commodity is ₹ 10, the demand is 1 kg.

- When the price falls from ₹ 10 to ₹ 8, the demand rises from 1 kg to 2 kg.

- Similarly, as the price falls from ₹ 8 to 6 and from ₹ 6 to 4, the demand rises from 2 kg to 3 kg and 3 kg to 4 kg, respectively.

- If we look at the schedule from bottom to top, when the price rises from ₹ 2 to ₹ 4, the demand falls from 5 kg to 4 kg.

- Thus, we can conclude that as the price of a commodity falls, the quantity demanded rises, and when the price of the commodity rises, the quantity in demand falls.

- This shows an inverse relationship between price and quantity demanded.

- Demand Curve: The law of demand can be further explained with the help of the following demand curve:

In the above diagram, the Y-axis represents price, and the X-axis represents quantity demanded. DD is the demand curve that slopes downward from left to right. It represents the inverse relation between price and quantity in demand. - Exceptions: The exceptions to the law are as follows:

- Giffen’s paradox: Giffen Goods are inferior or low-quality goods like vanaspati ghee (Dalda), low-quality rice, etc. These are goods whose demand does not rise, even if their price falls. This happens because every person wants to increase their standard of living constantly.

Sir Robert Giffen observed this behaviour related to bread (an inferior good) in England. People had limited money, so they consumed more bread (a cheaper commodity) and less meat (a costlier commodity). He observed that when the price of bread decreased, less bread was demanded than before. The people saved money and used it to purchase meat, and thus, the demand for meat increased. This behaviour is called “Giffen’s paradox”. There is a direct relationship between price and quantity demanded in the case of Giffen goods. The demand curve for Giffen goods slopes upward from left to right. - Speculation: The law of demand does not hold true when people expect prices to rise further. In this case, although prices have risen today, consumers will demand more in anticipation of a further rise in the price. For example, during the epic lockdown in March 2020, people expected the prices of goods to rise in the future. Therefore, they purchased goods in large quantities, even at high prices.

- Habitual Goods: If a person is habituated to or addicted to certain goods, his demand for these goods will continue to be the same even if the price of such goods rises. For example, people addicted to social media like FB, TikTok, Instagram, etc., will not reduce their usage even if the data packs or internet usage rates are increased.

- Illusion of Price: Consumers may believe that high-priced goods are of better quality; therefore, demand for such goods tends to increase with an increase in their prices. For example, expensive branded products are in demand, even at high prices.

- Prestige Goods: Prestige goods are regarded as a status symbol in society. Rich people may demand more of these goods when their prices rise to show off. E.g. Gold, diamonds, expensive watches, luxury cars, etc.

- Fashion: A product that is out of fashion (e.g., keypad phones) will have less demand even if the price falls. A product in fashion (e.g., smartphones) will have a high demand even if the price rises. Thus, it is an exception to the law.

- Ignorance: Sometimes, people buy more of a commodity at high prices due to ignorance. This may happen because the consumer is not aware of the cost of the commodity at other places.

- Necessities: The demand for specific necessities like basic foodstuffs (wheat, salt, dal, etc.) will not change due to a change in their prices.

- Demonstration Effect: The tendency of the low-income group to imitate the consumption pattern of high-income groups is known as the demonstration effect. For example, the T-shirts “Being Human” by Salman Khan are in very high demand despite their high prices.

- Giffen’s paradox: Giffen Goods are inferior or low-quality goods like vanaspati ghee (Dalda), low-quality rice, etc. These are goods whose demand does not rise, even if their price falls. This happens because every person wants to increase their standard of living constantly.

Introduction: The law of demand was introduced by Prof. Alfred Marshall in his book ‘Principles of Economics’, published in 1890. The law explains the functional relationship between price and quantity demanded.

Statement of the Law: According to Prof. Alfred Marshall, “Other things being equal, higher the price of a commodity, smaller is the quantity demanded and lower the price of a commodity, larger is the quantity demanded.”

In other words, other factors remaining constant, if the price of a commodity rises, demand for it falls and when price of a commodity falls demand for the commodity rises. Thus, there is an inverse relationship between price and quantity demanded.

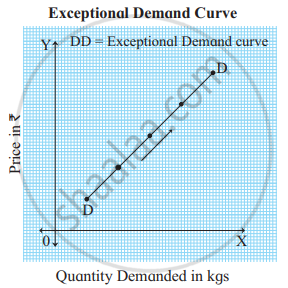

Exceptions to the Law of Demand: There are certain exceptions to the law of demand. It means that under exceptional circumstances, consumer buys more when the price of commodity rises and buys less when price of commodity falls. In such cases, demand curve slopes upwards from left to right. i.e. the demand curve has a positive slope as shown in figure.

Following are the exceptions to the law of demand:

- Giffen’s paradox: Inferior goods or low-quality goods are those goods whose demand does not rise even if their price falls. At times, demand decreases when the price of such commodities falls. Sir Robert Giffen observed this behaviour in England regarding bread. He noted that, when the price of bread declined, people did not buy more because of an increase in their real income or purchasing power. They preferred to buy superior goods like meat. This is known as Giffen’s paradox.

- Prestige goods: Expensive goods like diamonds, gold, etc., are status symbols. So rich people buy more of it, even when their prices are high.

- Speculation: The law of demand does not hold true when people expect prices to rise still further. In this case, although prices have risen today, consumers will demand more in anticipation of a further price rise. For example, prices of oil, sugar, etc., tend to rise before Diwali. So people continue purchasing more at high prices, anticipating that prices may rise during Diwali.

- Price illusion: Consumers believe that high-priced goods are of better quality. Therefore, the demand for such goods tends to increase with a rise in their prices. For example, expensive branded products are in demand even at high prices.

- Ignorance: Sometimes, due to ignorance, people buy more of a commodity at a high price. This may happen when consumer is ignorant about the price of that commodity at other places.

- Habitual goods: Due to habitual consumption, certain goods, such as tea, are purchased in required quantities even at higher prices.

Key Points

- Micro demand = individual level; macro demand = whole economy (aggregate) level.

- Both levels must mention price and time for demand to make sense.

- Demand is always a “flow” concept—measured as so much per time period.

| Type of Demand | Meaning / Explanation | Examples |

|---|---|---|

| Individual Demand | Demand of a single consumer | Demand of one person for a product |

| Market Demand | Sum total of demands of all consumers | Total demand for rice in a market |

| Ex ante Demand | Planned or desired demand | Expected demand for a product |

| Ex post Demand | Actual demand realised in the market | Actual sales of a product |

| Joint Demand | Demand for goods used together | Car and petrol |

| Derived Demand | Demand arising from demand for another good | Labour, raw materials |

| Composite Demand | Demand for goods with multiple uses | Coal, electricity, milk |

| Direct Demand | Demand for goods directly satisfying wants | Food, clothes |

| Alternative Demand | Demand satisfied by alternatives | Rice or chapati |

| Competitive Demand | Demand for substitute goods | Tea and coffee |

- The demand curve represents the law of demand visually.

- There are two types: individual and market demand curves.

- The market demand curve is derived by summing individual curves at each price.

- Movements along the curve are due to price changes; curve shifts are due to outside factors.

- Change in demand occurs due to factors other than price.

- Increase in demand: Demand curve shifts right (favourable factors).

- Decrease in demand: Demand curve shifts left (unfavourable factors).

- Law of demand only shows direction (more or less), elasticity shows the degree (how much more or less).

- Some things (necessities) have inelastic demand; luxuries or goods with many substitutes have elastic demand.

- Alfred Marshall introduced this concept and the popular measurement formula.

- YED shows how demand changes with income.

- Luxury goods: YED > 1 → demand grows faster than income.

- Necessities: 0 < YED < 1 → demand grows slower than income.

- Essential goods: YED = 0 → demand stays the same.

- Inferior goods: YED < 0 → demand drops as income rises.

- Total Expenditure Formula:

Total Expenditure (TE) = Price (P) × Quantity Demanded (Q) - Revenue Method Formula:

Ed = AR / (AR - MR)

or

Ed = Average Revenue / (Average Revenue - Marginal Revenue) - Arc Elasticity Demand Formula:

\[\mathrm{E=\frac{Q_{2}-Q_{1}}{Q_{2}+Q_{1}}\div\frac{P_{1}-P_{2}}{P_{1}+P_{2}}}\] - Proportionate Method Formula:

\[\mathrm{Ed}=\frac{\text{Percentage change in Quantity demanded}}{\text{Percentage change in Price}}\]

\[\mathrm{Ed}=\frac{\%\triangle\mathrm{Q}}{\%\triangle\mathrm{P}}\]

Important Questions [91]

- Write Explanatory Answer. State and Explain the Law of Demand with Its Exception.

- Fill in the Blank with Appropriate Alternatives Given in the Bracket: Demand for Salt is ___________.

- Do You Agree with the Following Statement? Give Reason Many Factors Influence the Demand for a Commodity.

- Distinguish between desire and demand.

- Explain the Following Concepts Or Give Definitions. Demand

- Demand for Necessaries is

- There Are No Exceptions to the Law of Demand.

- Demand for Electricity is Elastic.

- Give Reasons Or Explain the Following Statement Demand for Habitually Used Goods in Inelastic.

- Explain the following concept: Effective demand

- Fill in the Blank Using Proper Alternative Given in the Bracket:Perfectly Inelastic Demand Curve is

- State Whether the Following Statement is True Or False :Demand for Necessary Goods is Inelastic.

- Match the Pairs

- State whether the following statement is True or False. Demand for perishable goods is inelastic.

- State with Reason. Whether You ‘Agree’ Or ‘Disagree’ with the Following Statement: There Are No Exceptions to the Law of Demand.

- Fill in the Blank with Proper Alternatives Given in the Bracket:Indirect Demand is Also Known as _______ Demand.

- State Whether the Following Statement is True Or False.Perfectly Inelastic Demand Curve is Parallel to ‘X’ Axis.

- Write Short Answer for the Following Question.Explain the Law of Demand.

- Fill in the Blank Using Proper Alternatives Given in the Bracket:Demand for Salt is ...............

- Demand Curve and Supply Curve.

- State and explain the law of demand.

- Fill in the Blanks Using Proper Alternatives Given in the Brackets. Demand for Car and Petrol is ____________ De

- Write whether the following statement is True or False: Demand curve has a positive slope.

- Write whether the following statement is True or False: Demand for commodities depends upon various factors.

- Write whether the following statement is True or False: Salt has elastic demand.

- Demand for habitual commodity is ______.

- Define the concept of demand schedule.

- State Whether the Following Statement is True Or False:

- Fill in the Blank Using Appropriate Alternatives Given Below the Demand for Perishable Goods is _______

- Distinguish Between : Individual Demand Schedule and Market Demand Schedule.

- Fill in the blank with appropriate alternatives given in the bracket: The law of demand states ________ relation between demand and price.

- Write Answers in ‘One’ Or ‘Two’ Paras Each. What Are the Main Determinants of Aggregate Demand?

- Distinguish between Joint demand and Composite demand.

- Distinguish between expansion in demand and increase in demand.

- A Perfectly Inelastic Demand Curve is Parallel to 'Y' Axis.

- Distinguish Between Individual Demand and Market Demand. With the help of diagrams explain the difference between individual demand and market demand.

- Match the Following Group 'A' with Group 'B': (A) Electricity (1) Joint Demand (B) Perfectly Elastic Demand (2) Lord Keynes (3) Prof. Pigou (C) Aggregate Supply

- Define Or Explain the Following Concepts (Any Three): Individual Demand

- Distinguish between the following: Direct demand and Indirect demand.

- Identify and explain the following concept: Due to mandatory use of masks during corona epidemic the demand for mask producing labour has increased.

- Find the odd word out: Types of demand: Direct demand, Indirect demand, Composite demand, Market demand

- Distinguish between: Joint/complementary demand and competitive demand.

- Explain with Reason Whether You 'Agree' Or 'Disagree' with the Following Statement: There Are Many Types of Demands.

- Explain any four types of demand.

- Complete the correlation. Direct demand : Food and Mobiles : ______ : Land and Labour.

- State Whether the Following Statements Are True Or False with Reason: Demand for Medicine is Inelastic.

- Define Or Explain the Concept Perfectly Elastic Demand

- The Demand for Salt is _____________

- Population is the Only Determinant Factor of Demand.

- Change in the Price of Substitute Goods Affects the Demand for Another Goods.

- Explain with Reason Whether You ‘Agree’ Or ‘Disagree’ with the Following Statement:Various Factors Incluence Tha Demand for a Commodity.

- The Slope of Demand Curve is ___________ in the Case of Relatively Inelastic Demand. [Flatter/ Steeper/ Horizontal / Vertical]

- State with reasons whether you ‘agree’ or ‘disagree’ with the following statement. Demand curve slopes downward from left to right.

- Write Explanatory Notes Or Answer the Following. Aggregate Demand

- Define Or Explain the Following Concept.Market Demand .

- Fill in the Blank Using Proper Alternative Given in the Bracket:Market Demand is a Total Demand Of...............Buyers.

- Explain the law of demand with its assumptions.

- State with reason, whether you Agree or Disagree with the following statement. The demand curve slopes downward from left to right.

- State and explain the ‘law of demand’ with its exceptions.

- Explain the concept of price elasticity of demand.

- Income elasticity of demand for inferior goods is negative.

- Demand for the Commodity Having Multiple Uses Has Elastic Demand.

- Explain the factors determining the elasticity of demand.

- Explain any 'two methods' of measuring price elasticity of demand.

- Write Short Notes Proportional Method of Measuring the Elasticity of Demand.

- Define Or Explain the Following Concept.Unitary Elastic Demand.

- Write a short note on factors determining elasticity of demand.

- State Whether the Following Statement is True Or False :Concept of Elasticity of Demand is Useful for Finance Minister.

- What is the elasticity of demand?

- State Whether the Following Statement Istrue Or False with Reason: The Concept of Elasticity of Demand is Useful in Economic Theory.

- Give Reasons Or Explain the Following Statements Demand for Basic Necessities is Inelastic.

- State Whether the Following Statements Are True Or False : the Demand of Foodgrains is Inelastic.

- Fill in the blanks with appropriate alternatives given in the bracket. Demand elasticity can be measured from demand curve by ___________ method.

- Fill in the Blank with Appropriate Alternatives Given Below: Income Elasticity of Demand for Inferior Goods is __________.

- Write Short Answer for the Following Question :

- Give an economic term: Elasticity resulting from a proportionate change in quantity demanded due to a proportionate change in price.

- State whether the following statements are TRUE or FALSE : The demand of foodgrains is inelastic.

- Choose the Correct Answer : Demand of Labour is _______

- Choose the Correct Answer : Perfectly Elastic Demand Curve is _________.

- State Whether the Following Statement Is True Or False :Concept of ‘Elasticity of Demand’ is Useful for the Finance Minister.

- State with Reason Whether You Agree Or Disagree with the Following Statements. (Any Three) Vrious Factors Influence Elasticity of Demand.

- Match the Following :(A) Demand and Price (1) Wages (B) Perfectly Elastic Supply (2) Vertical Supply Curve (C) Land (3) Transfer Income (D) Unemployment Allowance(4) Horizontal Supply Curve

- Define Or Explain the Following Concepts (Any Three): Stock

- Write Short Note on the Following. Ratio Method of Measuring Price Elasticity of Demand ?

- The account in which the specific amount is deposited per month regularly is known as ______.

- Choose the Correct Answer : Demand of Electricity for Domestic Purpose is _________.

- Answer the Following Questions. [Any Three] Explain the Imprtance of Elasticity of Demand.

- Explain with Reason, Whether You Agree Or Disagree with the Following Statement:Price Elasticity of Demand Can Not Be Measured by Using Geometric Method.

- Give Reasons Or Explain the Following Statements (Any Four): the Demand Curve is Sloping Down from Left to Right.

- Write Short Notes Significance of Price Elasticity of Demand.

- Define Or Explain the Following Concepts (Any Three): Cross Elasticity of Demand