Advertisements

Advertisements

Question

Illustrate the concept of Producer’s Equilibrium.

Advertisements

Solution

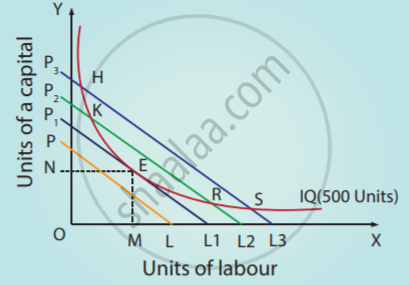

Producer equilibrium is the situation where the producer maximizes his output. It is also known as the optimum combination of the factors of production.

(Eg.) Maximum output at minimum cost.

Producer attains equilibrium where the Iso-cost line is tangent to the Iso-quant.

In the figure profit of the firm is maximized at the point of equilibrium.

At the point of equilibrium slope of the Iso-cost line = Slope of Iso-product curve At the point E, the firm employs OM units of labour and ON units of capital which is the least cost combination.

APPEARS IN

RELATED QUESTIONS

Producer’s equilibrium is achieved at the point where:

What are the conditions for the producer’s equilibrium?

A producer in microeconomics is best described as ______.

Producer’s equilibrium refers to the situation where the producer ______.

Which pair of conditions must be satisfied for producer’s equilibrium under the MR–MC approach?

In terms of total revenue and total cost, the producer is in equilibrium at the output level where ______.

If at a given level of output MR < MC, what should the producer do to reach equilibrium?