Advertisements

Advertisements

Question

Manish and Naveen, after completing their graduation in commerce, decided to enter into a partnership to deal in Refrigerators. Sachin, a fresh graduate in business administration who was a close friend of both of them, also requested them to take him into partnership. They also took Sachin into partnership and prepared a partnership deed containing. The following clauses:

- Name of the firm will be ‘Ganga Refrigerators.’

- Capital: Manish and Naveen will contribute ₹12,00,000 each, whereas Sachin will contribute ₹6,00,000.

- Profit-Sharing Ratio: Profits and Losses are to be shared in the ratio of their Capital contribution.

- Interest on Capital: No interest on capital shall be allowed to the partners.

- Interest on Drawings: Interest on drawings is to be charged @ 10% p.a.

- Salary to a Partner: No partner is entitled to any salary or commission for taking part in running the firm’s business.

- Interest on Loan: Interest at the rate of 6% per annum is to be allowed on a partner’s loan to the firm. Such interest shall be paid even if there are losses to the firm.

- Admission of a New Partner: Without the consent of all existing partners, no new partner can be admitted to the firm.

- Each partner can participate in conduct of business.

- Each partner can inspect the books of firm and can take a copy of the same.

On 1st April, 2022, the partners contributed their share of capital, and the entire amount of Capital was deposited into the bank. On the same date, they entered into an agreement with L.G. Limited to sell the Refrigerators, bought from them on a one-month credit basis.

At the beginning of the year they purchased the following assets making payments through bank:

| ₹ | |

| Building | 25,00,000 |

| Office Equipments | 2,00,000 |

| Furniture | 1,50,000 |

Refrigerators were to be sold for cash only and the cash proceeds were to be deposited in the bank on the same day. All expenses were to be paid only through bank.

The following transactions were affected through bank during the year ended 31st March, 2023:

| ₹ | |

| Purchases | 16,90,000 |

| Sales | 24,60,000 |

| Salaries | 66,000 |

| Advertising expenses | 9,400 |

| Telephone expenses | 10,200 |

| Electricity expenses | 7,600 |

| Printing and stationery | 3,600 |

| Insurance premium | 4,000 |

| Sundry Expenses | 22,000 |

Manish withdrew for his personal use ₹10,000 per month at the end of each month.

Naveen withdrew for his personal use ₹8,000 per month at the beginning of each month.

Sachin withdrew for his personal use ₹40,000 during the year.

The purchases for the month of March 2023 amounted to ₹1,40,000. L.G. Limited was paid for purchases as per the terms agreed upon.

Other Information:

- Salaries have been paid for 11 months.

- Telephone expenses ₹1,000 and Electricity expenses ₹800 are yet to be paid.

- The closing stock as at 31st March, 2023, were as follows:

Refrigerators ₹3,50,000 Stationery ₹600 - Charge depreciation on building @ 4% and on Office Equipment and Furniture @ 20%.

Prepare Journal Entries, Ledger Accounts, and Trial Balance as on 31st March, 2023, Trading and Profit & Loss Account for the year ended on 31st March, 2023, and a Balance Sheet as at that date.

Further:

- L.G. Ltd. wants to know the short-term financial position of the Firm before extending the agreement on credit policy for the next year.

- Partners want to know the profitability of their business in terms of sales and capital employed into the business.

You are required to compute the required ratios and comment upon them.

Advertisements

Solution

Introduction of the Project:

The project work is:

- To prepare Journal and Ledger of M/s Ganga Refrigerators from the very start of the business;

- To prepare a trial balance;

- To prepare Trading and Profit & Loss Account for the year ended 31st March, 2023;

- To prepare a Balance Sheet as at 31st March, 2023;

- To assess the short-term financial position of the firm;

- To assess the profitability of the firm on the basis of profitability ratios.

The necessary data is provided and is used for the purpose of project work.

The project work is planned and executed as follows:

- Prepare Journal and Ledger Accounts;

- Prepare Trial Balance;

- Prepare Trading and Profit & Loss Account for the year ended 31st March, 2023;

- Prepare Balance Sheet as at 31st March, 2023;

- Calculate Current Ratio and Quick Ratio to assess the short-term financial position;

- Calculate Gross Profit Ratio, Net Profit Ratio, and Return on Capital Employed to assess the profitability of the business.

| JOURNAL OF GANGA REFRIGERATORS | ||||

| Date | Particulars | L.F. | Amount Dr. (₹) |

Amount Cr. (₹) |

| 2022 | ||||

| April 1 | Bank A/c ...Dr. | 30,00,000 | - | |

| To Manish’s Capital A/c | - | 12,00,000 | ||

| To Naveen’s Capital A/c | - | 12,00,000 | ||

| To Sachin’s Capital A/c | - | 6,00,000 | ||

| (Amount contributed as capital) | ||||

| April 1 | Building A/c ...Dr. | 25,00,000 | - | |

| Office Equipments A/c ...Dr. | 2,00,000 | - | ||

| Furniture A/c ...Dr. | 1,50,000 | - | ||

| To Bank A/c | - | 28,50,000 | ||

| (Assets purchased) | ||||

| 2023 | ||||

| March 31 | Purchases A/c ...Dr. | 16,90,000 | - | |

| To Bank A/c | - | 16,90,000 | ||

| (Purchase of Refrigerators) | ||||

| March 31 | Bank A/c ...Dr. | 92,000 | - | |

| To Sales A/c | - | 92,000 | ||

| (Sales of Refrigerators) | ||||

| March 31 | Salaries A/c ...Dr. | 66,000 | - | |

| Advertising Exp. A/c ...Dr. | 9,400 | - | ||

| Telephone Exp. A/c ...Dr. | 10,200 | - | ||

| Electricity Exp. A/c ...Dr. | 7,600 | - | ||

| Printing and Stationery A/c ...Dr. | 3,600 | - | ||

| Insurance Premium A/c ...Dr. | 4,000 | - | ||

| Sundry Expenses A/c ...Dr. | 22,000 | - | ||

| To Bank A/c | - | 1,22,800 | ||

| (Payment for expenses through the bank) | ||||

| March 31 | Manish’s Drawings A/c ...Dr. | 1,20,000 | - | |

| Naveen’s Drawings A/c ...Dr. | 96,000 | - | ||

| Sachin’s Drawings A/c ...Dr. | 40,000 | - | ||

| To Bank A/c | - | 2,56,000 | ||

| (Amount withdrawn for personal expenses) | ||||

| March 31 | Manish’s Capital A/c ...Dr. | 1,20,000 | - | |

| Naveen’s Capital A/c ...Dr. | 96,000 | - | ||

| Sachin’s Capital A/c ...Dr. | 40,000 | - | ||

| To Manish’s Drawings A/c | - | 1,20,000 | ||

| To Naveen’s Drawings A/c | - | 96,000 | ||

| To Sachin’s Drawings A/c | - | 40,000 | ||

| (Transfer of Drawings to Capital Accounts) | ||||

| March 31 | Purchases A/c ...Dr. | 1,40,000 | - | |

| To Creditors | - | 1,40,000 | ||

| (Payment due for last month’s purchases) | ||||

| March 31 | Salaries A/c ...Dr. | 6,000 | - | |

| Telephone Exp. A/c ...Dr. | 1,000 | - | ||

| Electricity Exp. A/c ...Dr. | 800 | - | ||

| To Outstanding Expenses A/c | - | 7,800 | ||

| (Amount due for expenses) | ||||

| March 31 | Stock of Stationery A/c ...Dr. | 600 | - | |

| To Stationery A/c | - | 600 | ||

| (Stock of Stationery at the end of the year) | ||||

| March 31 | Closing Stock A/c ...Dr. | 3,50,000 | - | |

| To Trading A/c | - | 3,50,000 | ||

| (Stock of Refrigerators at the end of the year) | ||||

| March 31 | Depreciation A/c ...Dr. | 1,70,000 | - | |

| To Office Equipments A/c | - | 40,000 | ||

| To Furniture A/c | - | 30,000 | ||

| To Building A/c | - | 1,00,000 | ||

| (Depreciation Charged on different assets) | ||||

| March 31 | Profit and Loss A/c ...Dr. | 6,80,000 | - | |

| To Profit and Loss Appropriation A/c | - | 6,80,000 | ||

| (The transfer of Profit to Profit and Loss Appropriation Account) | ||||

| March 31 | Manish’s Capital A/c ...Dr. | 5,500 | - | |

| Naveen’s Capital A/c ...Dr. | 5,200 | - | ||

| Sachin’s Capital A/c ...Dr. | 2,000 | - | ||

| To Interest on Drawings A/c | - | 12,700 | ||

| (Interest on partners’ drawings) | ||||

| March 31 | Interest on Drawings A/c ...Dr. | 12,700 | - | |

| To Profit & Loss Appropriation A/c | - | 12,700 | ||

| (The transfer of interest on drawings to Profit & Loss Appropriation Account) | ||||

| March 31 | Profit and Loss Appropriation A/c ...Dr. | 6,92,700 | - | |

| To Manish’s Capital A/c | - | 2,77,080 | ||

| To Naveen’s Capital A/c | - | 2,77,080 | ||

| To Sachin’s Capital A/c | - | 1,38,540 | ||

Notes:

- Interest in Manish’s Drawings:

Since he has withdrawn at the end of every month, interest on the whole amount will be calculated for 5.5 months:

`1,20,000xx10/100xx5.5/12= "₹"5,500` - Interest in Naveen’s Drawings:

Since he has withdrawn at the beginning of every month, interest on the whole amount will be calculated for 6.5 months:

`96,000xx10/100xx6.5/12= "₹"5,200` - Interest in Sachin’s Drawings:

As the date of the drawings is not given, interest will be calculated for an average period of 6 months:

`40,000xx10/1006/12= "₹"2,000`

LEDGER ACCOUNTS:

| BANK ACCOUNT | |||||

| Date | Particulars | Amount (₹) |

Date | Particulars | Amount (₹) |

| 2022 | 2022 | ||||

| April 1 | To Manish’s Capital A/c | 12,00,000 | April 1 | By Building A/c | 25,00,000 |

| To Naveen’s Capital A/c | 12,00,000 | April 1 | By Office Equipments A/c | 2,00,000 | |

| To Sachin’s Capital A/c | 6,00,000 | April 1 | By Furniture A/c | 1,50,000 | |

| 2023 | 2023 | ||||

| March 31 | To Sales A/c | 24,60,000 | March 31 | By Purchases A/c | 16,90,000 |

| March 31 | By Salaries A/c | 66,000 | |||

| March 31 | By Advertisement Expenses A/c | 9,400 | |||

| March 31 | By Telephone Expenses A/c | 10,200 | |||

| March 31 | By Electricity Expenses A/c | 7,600 | |||

| March 31 | By Printing and Stationery A/c | 3,600 | |||

| March 31 | By Insurance Premium A/c | 4,000 | |||

| March 31 | By Sundry Expenses | 22,000 | |||

| March 31 | By Manish’s Drawings | 1,20,000 | |||

| By Naveen’s Drawings | 96,000 | ||||

| By Sachin’s Drawings | 40,000 | ||||

| March 31 | By Balance c/d | 5,41,200 | |||

| 54,60,000 | 54,60,000 | ||||

| MANISH’S CAPITAL ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2022 | ||||||

| March 31 | To Drawings A/c | 1,20,000 | April 1 | By Bank A/c | 12,00,000 | ||

| March 31 | To Balance c/d | 10,80,000 | |||||

| 12,00,000 | 12,00,000 | ||||||

| NAVEEN’S CAPITAL ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2022 | ||||||

| March 31 | To Drawings A/c | 96,000 | April 1 | By Bank A/c | 12,00,000 | ||

| March 31 | To Balance c/d | 11,04,000 | |||||

| 12,00,000 | 12,00,000 | ||||||

| SACHIN’S CAPITAL ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2022 | ||||||

| March 31 | To Drawings A/c | 40,000 | April 1 | By Bank A/c | 6,00,000 | ||

| March 31 | To Balance c/d | 5,60,000 | |||||

| 6,00,000 | 6,00,000 | ||||||

| BUILDING ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April 1 | To Bank A/c | 25,00,000 | March 31 | By Depreciation A/c | l,00,000 | ||

| March 31 | By Balance c/d | 24,00,000 | |||||

| 25,00,000 | 25,00,000 | ||||||

| OFFICE EQUIPMENT ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April 1 | To Bank A/c | 2,00,000 | March 31 | By Depreciation A/c | 40,000 | ||

| March 31 | By Balance c/d | 1,60,000 | |||||

| 2,00,000 | 2,00,000 | ||||||

| FURNITURE ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April 1 | To Bank A/c | 1,50,000 | March 31 | By Depreciation A/c | 30,000 | ||

| March 31 | By Balance c/d | 1,20,000 | |||||

| 1,50,000 | 1,50,000 | ||||||

| PURCHASES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 16,90,000 | March 31 | By Trading A/c | 18,30,000 | ||

| March 31 | To Creditors A/c | 1,40,000 | |||||

| 18,30,000 | 18,30,000 | ||||||

| SALES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Trading A/c | 24,60,000 | March 31 | By Bank A/c | 24,60,000 | ||

| SALARIES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 66,000 | March 31 | By P& L A/c | 72,000 | ||

| March 31 | To Outstanding Exp. A/c | 6,000 | |||||

| 72,000 | 72,000 | ||||||

| ADVERTISING EXP. ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 9,400 | March 31 | By P& L A/c | 9,400 | ||

| 9,400 | 9,400 | ||||||

| TELEPHONE EXP. ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 10,200 | March 31 | By P& L A/c | 11,200 | ||

| March 31 | To Outstanding Exp. A/c | 1,000 | |||||

| 11,200 | 11,200 | ||||||

| ELECTRICITY EXPENSES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 7,600 | March 31 | By Profit & Loss A/c | 8,400 | ||

| March 31 | To Outstanding Exp. A/c | 800 | |||||

| 8,400 | 8,400 | ||||||

| PRINTING AND STATIONERY ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 3,600 | March 31 | By Stock of Stationery | 600 | ||

| March 31 | By Profit & Loss A/c | 3,000 | |||||

| 3,600 | 3,600 | ||||||

| INSURANCE PREMIUM ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 4,000 | March 31 | By P& L A/c | 4,000 | ||

| 4,000 | 4,000 | ||||||

| SUNDRY EXPENSES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 22,000 | March 31 | By P& L A/c | 22,000 | ||

| 22,000 | 22,000 | ||||||

| MANISH’S DRAWINGS ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 1,20,000 | March 31 | By Capital A/c | 1,20,000 | ||

| 1,20,000 | 1,20,000 | ||||||

| NAVEEN’S DRAWINGS ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 96,000 | March 31 | By Capital A/c | 96,000 | ||

| 96,000 | 96,000 | ||||||

| SACHIN’S DRAWINGS ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 40,000 | March 31 | By Capital A/c | 40,000 | ||

| 40,000 | 40,000 | ||||||

| CREDITORS ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Balance c/d | 1,40,000 | March 31 | By Purchases A/c | 1,40,000 | ||

| 1,40,000 | 1,40,000 | ||||||

| OUTSTANDING EXP. ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Balance c/d | 7,800 | March 31 | By Salaries | 6,000 | ||

| March 31 | By Telephone Exp. | 1,000 | |||||

| March 31 | By Electricity Exp. | 800 | |||||

| 7,800 | 7,800 | ||||||

| STOCK OF STATIONERY ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Stationery A/c | 600 | March 31 | By Balance c/d | 600 | ||

| 600 | 600 | ||||||

| CLOSING STOCK ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Trading A/c | 3,50,000 | March 31 | By Balance c/d | 3,50,000 | ||

| 3,50,000 | 3,50,000 | ||||||

| OUTSTANDING EXP. ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Office Equipments A/c | 40,000 | March 31 | By P& L A/c | 1,70,000 | ||

| March 31 | To Furniture A/c | 30,000 | |||||

| March 31 | To Building A/c | 1,00,000 | |||||

| 1,70,000 | 1,70,000 | ||||||

| TRIAL BALANCE as at 31st March, 2023 | |||

| Dr. | Cr. | ||

| Particulars | Amount (₹) |

Particulars | Amount (₹) |

| Bank Balance | 5,41,000 | Manish’s Capital A/c | 12,00,000 |

| Building | 24,00,000 | Naveen’s Capital A/c | 12,00,000 |

| Office Equipments | 1,60,000 | Sachin’s Capital A/c | 6,00,000 |

| Purchases (₹16,90,000 + ₹1,40,000 for the month of March 2023) |

18,30,000 | Creditors (for purchases for the month of March 2023) |

1,40,000 |

| Furniture | 1,20,000 | Sales | 24,60,000 |

| Salaries | 72,000 | Outstanding Expenses | 7,800 |

| Advertisement Exp. | 9,400 | ||

| Telephone Exp. | 11,200 | ||

| Electricity Exp. | 8,400 | ||

| Printing and Stationery | 3,000 | ||

| Insurance Premium | 4,000 | ||

| Sundry Expenses | 22,000 | ||

| Manish’s Drawings | 1,20,000 | ||

| Naveen’s Drawings | 96,000 | ||

| Sachin’s Drawings | 40,000 | ||

| Stock of Stationery | 600 | ||

| Depreciation | 1,70,000 | ||

| 56,07,800 | 56,07,800 | ||

| TRADING & PROFIT AND LOSS ACCOUNT for the year ended 31st March, 2023 | ||||

| Particulars | Amount (₹) |

Amount (₹) |

Particulars | Amount (₹) |

| To Purchases | 18,30,000 | By Sales | 24,60,000 | |

| To Gross Profit transferred to P& L A/c | 9,80,000 | By Closing Stock (of Refrigerators) | 3,50,000 | |

| 28,10,000 | 28,10,000 | |||

| To Salaries | 66,000 | By Gross Profit b/d | 9,80,000 | |

| Add: Outstanding (66,000 ÷ 11) |

6,000 | 72,000 | ||

| To Advertisement Exp. | 9,400 | |||

| To Telephone Exp. | 10,200 | |||

| Add: Outstanding | 1,000 | 11,200 | ||

| To Electricity Exp. | 7,600 | |||

| Add: Outstanding | 800 | 8,400 | ||

| To Printing and Stationery | 3,600 | |||

| Less: Closing stock of stationery | 600 | 3,000 | ||

| To Insurance Premium | 4,000 | |||

| To Sundry Expenses | 22,000 | |||

| To Depreciation on: | ||||

| Building | 1,00,000 | |||

| Office Equipments | 40,000 | |||

| Furniture | 30,000 | 1,70,000 | ||

| To Net Profit transferred to Profit & Loss Appropriation A/c | 6,80,000 | |||

| 9,80,000 | 9,80,000 | |||

| TRADING & PROFIT AND LOSS ACCOUNT for the year ended 31st March, 2023 | |||||

| Particulars | Amount (₹) |

Amount (₹) |

Particulars | Amount (₹) |

Amount (₹) |

| To Profit Transferred to: | By Profit & Loss A/c (Net Profit) | 6,80,000 | |||

| Manish’s Capital A/c | 2,77,080 | By Interest on Drawings: | |||

| Naveen’s Capital A/c | 2,77,080 | Manish | 5,500 | ||

| Sachin’s Capital A/c | 1,38,540 | 6,92,700 | Naveen | 5,200 | |

| Sachin | 2,000 | 12,700 | |||

| 6,92,700 | 6,92,700 | ||||

| PARTNERS’ CAPITAL ACCOUNTS (After Appropriations) as at 31st March, 2023 | |||||||

| Particulars | Manish (₹) |

Naveen (₹) |

Sachin (₹) |

Particulars | Manish (₹) |

Naveen (₹) |

Sachin (₹) |

| To Interest on Drawings | 5,500 | 5,200 | 2,000 | By Balance b/d (Net after drawings) | 10,80,000 | 11,04,000 | 5,60,000 |

| To Balance c/d | 13,51,580 | 13,75,880 | 6,96,540 |

By Profit & Loss Appropriation A/c |

2,77,080 | 2,77,080 | 1,38,540 |

| 13,57,080 | 13,81,080 | 6,98,540 | 13,57,080 | 13,81,080 | 6,98,540 | ||

| BALANCE SHEET as at 31st March, 2023 | |||||

| Particulars | Amount (₹) |

Amount (₹) |

Particulars | Amount (₹) |

Amount (₹) |

| Creditors | 1,40,000 | Bank balance | 5,41,200 | ||

| Outstanding Expenses for: | Stock of Refrigerators | 3,50,000 | |||

| Salaries | 6,000 | Stock of Stationery | 600 | ||

| Telephone Exp. | 1,000 | Office Equipments | 2,00,000 | ||

| Electricity Exp. | 800 | Less: Depreciation | 40,000 | 1,60,000 | |

| Capitals: | Furniture | 1,50,000 | |||

| Manish | 13,51,580 | Less: Depreciation | 30,000 | 1,20,000 | |

| Naveen | 13,75,880 | Building | 25,00,000 | ||

| Sachin | 6,96,540 | 34,24,000 | Less: Depreciation | 1,00,000 | 24,00,000 |

| 35,71,800 | 35,71,800 | ||||

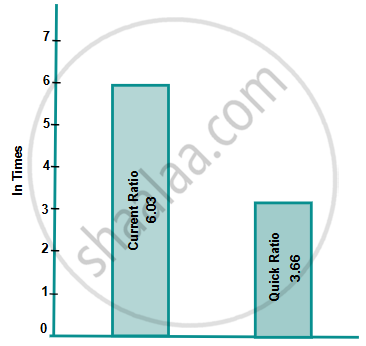

(1) Short-term Financial Position:

- `"Current Ratio"="Current Assets"/"Current Liabilities"`

`=(8,91,800)/(1,47,800)`

= 6.03:1 - `"Quick Ratio"="Quick Assets"/"Current Liabilities"`

`=(5,41,200)/(1,47,800)`

= 3.66:1 - Comments: The short-term financial position of the business is sound because its current ratio is higher than the ideal ratio of 2:1. Similarly, the quick ratio is also higher than the ideal ratio of 1:1. Hence, L.G. Ltd. may extend the credit facility.

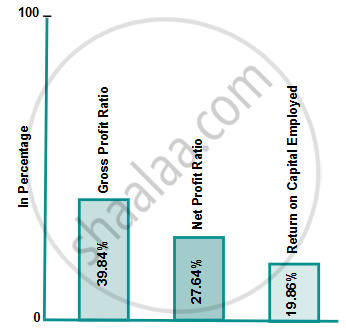

(2) Profitability:

- `"G.P. Ratio"="G.P."/"Net Sales"xx100`

`=(9,80,000)/(24,60,000)xx100`

= 39.84% - `"N.P. Ratio"="N.P."/"Net Sales"xx100`

`=(6,80,000)/(24,60,000)xx100`

= 27.64% - `"Return on Capital Employed"="N.P."/"Capital employed"xx100`

`=(6,80,000)/(34,24,000)xx100`

= 19.86% - Comments: These ratios indicate that the profitability in terms of sales and profitability in terms of capital employed is quite good.

PRESENTATION OF INFORMATION:

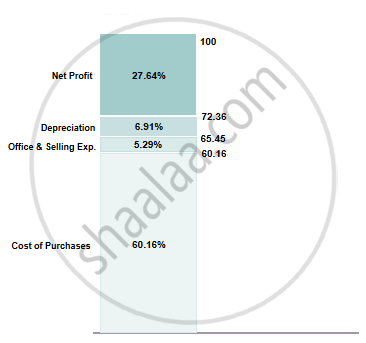

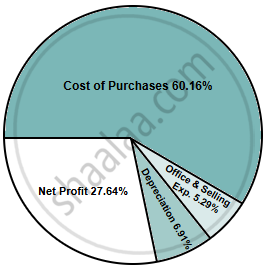

| Sales | 24,60,000 | 100% | Cumulative Percentages |

| Cost of Purchases (Purchases Less Closing Stock) |

14,80,000 | 60.16% | 60.16% |

| Office & Selling Exp. | 1,30,000 | 5.29% | 65.45% |

| Depreciation | 1,70,000 | 6.91% | 72.36% |

| Net Profit | 6,80,000 | 27.64% | 100.00% |

| 24,60,000 | 100.00% |

BAR DIAGRAM:

PIE CHART:

DEPICTION OF RATIOS:

(1)

(2)