Advertisements

Advertisements

Question

After doing their graduation, Banerjee suggested to his classmate Chatterjee to form a partnership to start a computer business. Chatterjee agreed to the proposal and requested to admit his friend Diwedi also to the proposed firm. All of them formed a partnership and prepared a partnership deed containing the following clauses:

- Name of the firm will be ‘Progressive Computers’.

- Capital: Banerjee will contribute ₹6,00,000, Chatterjee ₹5,00,000, and Diwedi ₹4,00,000.

- Profit-Sharing Ratio: Profits and Losses are to be shared equally, irrespective of their capital contribution.

- Interest on Capital: Interest on Capital shall be allowed @ at 8% per annum. Interest on capital will be allowed only when there is a profit.

- Interest on Drawings: No interest is to be charged on drawings.

- Salary to a Partner: No partner is entitled to any salary or commission for taking part in running the firm’s business.

- Interest on Loan: Interest at the rate of 6% per annum is to be allowed on a partner’s loan to the firm. Such interest shall be paid even if there are losses to the firm.

- Admission of a New Partner: Without the consent of all existing partners, no new partner can be admitted to the firm.

- Each partner can participate in the conduct of business.

- Each partner can inspect the books of firm and can take a copy of the same.

They started business on 1st April 2022, and the partners contributed the entire share of their capitals by cheques drawn in the firm’s name. On the same date, they deposited the cheques in the bank.

On the same date, they purchased 20 computers of ₹50,000 each. They deposited ₹20,000 for the electric connection with the Electricity Board and also deposited ₹1,50,000 with the VSNL for Internet and telephone connection.

They spent ₹40,000 for getting the Computer Cafe furnished and also spent ₹6,000 in getting the pamphlets printed and distributed.

All payments were to be made by cheques and all the receipts were to be deposited in the bank on the same day.

At the end of the year, the results were:

| ₹ | |

| Purchases of Computer stationery like floppy discs, CDs, etc. | 92,000 |

| Revenue from fees received from students of Computer classes | 5,48,000 |

| Revenue on Account of Internet Facility | 4,20,000 |

| Revenue from sale of Computer Stationery | 1,60,000 |

| Wages paid to Servant | 60,000 |

| Electricity Charges | 2,40,000 |

| Telephone Charges | 73,000 |

| Entertainment Expenses | 7,000 |

| General Expenses | 5,200 |

| Rent of the Building | 1,20,000 |

Drawings made by partners were: Banerjee ₹50,000, Chatterjee ₹40,000, and Diwedi ₹20,000.

You are required to:

- Journalize the above transactions, post them into the Ledger, and prepare a trial balance.

- Prepare Trading and Profit & Loss Account and Balance Sheet, taking into consideration that a telephone bill of ₹6,800 is yet to be paid.

- Depreciate furniture by 20% and computers by 30%.

- Calculate profitability ratios and comment on the efficiency of the business ifthe norms set for Gross Profit Ratio and Net Profit Ratio in similar type of business enterprises are 60% and 15% respectively.

- Partners want to expand their business. They approached the bank for a loan of ₹5,00,000. Mention the ratios that the bank manager will take into consideration before granting the loan.

Advertisements

Solution

Introduction of the Project:

The project work is,

- To make an accounting record of all the transactions from the very start of the business of Progressive Computers;

- Prepare the firm’s Trading and Profit & Loss Account to ascertain the net profit for the period.

- To prepare the Balance Sheet of the firm to ascertain the financial position,

- To assess the profitability based on profitability ratios, and

- To suggest whether the bank manager should grant a loan.

The necessary data is provided and is used for project work.

The project work is planned and executed as follows:

- Prepare journal, ledger, and trial balance;

- Prepare Trading and Profit & Loss Account for the year ending 31st March, 2023, and a Balance Sheet as at 31st March, 2023;

- Calculate Gross Profit Ratio and Net Profit Ratio to assess the profitability of the business.

| JOURNAL | ||||

| Date | Particulars | L.F. | Amount Dr. (₹) |

Amount Cr. (₹) |

| 2022 |

||||

| April 1 | Bank A/c ...Dr. | 15,00,000 | - | |

| To Banerjee’s Capital A/c | - | 6,00,000 | ||

| To Chatterjee’s Capital A/c | - | 5,00,000 | ||

| To Diwedi’s Capital A/c | - | 4,00,000 | ||

| (Capital contributed by the partners deposited into the Bank) | ||||

| April 1 | Computers A/c ...Dr. | 10,00,000 | - | |

| To Bank A/c | - | 10,00,000 | ||

| (Computers purchased) | ||||

| April 1 | Electricity Board A/c ...Dr. | 20,000 | - | |

| VSNL A/c ...Dr. | 1,50,000 | - | ||

| To Bank A/c | - | 1,70,000 | ||

| (Security deposit with the electricity board and VSNL) | ||||

| April 1 | Furniture and Fixtures A/c ...Dr. | 40,000 | - | |

| To Bank A/c | - | 40,000 | ||

| (Furnishing of Computer Cafe) | ||||

| 2023 | ||||

| March 31 | Advertisement A/c ...Dr. | 6,000 | - | |

| To Bank A/c | - | 6,000 | ||

| (Payment made for pamphlets) | ||||

| March 31 | Purchases A/c ...Dr. | 92,000 | - | |

| To Bank A/c | - | 92,000 | ||

| (Purchase of computer stationery) | ||||

| March 31 | Bank A/c ...Dr. | 11,28,000 | - | |

| To Revenue from Fees and Sales A/c | - | 11,28,000 | ||

| (Fees received from computer classes ₹5,48,000, from the Internet facility ₹4,20,000, and from the sale of computer stationery ₹1,60,000.) | ||||

| March 31 | Wages A/c ...Dr. | 60,000 | - | |

| Electricity Charges A/c ...Dr. | 2,40,000 | - | ||

| Telephone Charges A/c ...Dr. | 73,000 | - | ||

| Entertainment Expenses A/c ...Dr. | 7,000 | - | ||

| General Expenses A/c ...Dr. | 5,200 | - | ||

| Rent A/c ...Dr. | 1,20,000 | - | ||

| To Bank A/c | - | 5,05,200 | ||

| (Expenses paid) | ||||

| March 31 | Banerjee’s Drawings A/c ...Dr. | 50,000 | - | |

| Chatterjee’s Drawings A/c ...Dr. | 40,000 | - | ||

| Diwedi’s Drawings A/c ...Dr. | 20,000 | - | ||

| To Bank A/c | - | 1,10,000 | ||

| (Amount withdrawn for personal expenses) | ||||

| March 31 | Banerjee’s Capital A/c ...Dr. | 50,000 | - | |

| Chatterjee’s Capital A/c ...Dr. | 40,000 | - | ||

| Diwedi’s Capital A/c ...Dr. | 20,000 | - | ||

| To Banerjee’s Drawings A/c | - | 50,000 | ||

| To Chatterjee’s Drawings A/c | - | 40,000 | ||

| To Diwedi’s Drawings A/c | - | 20,000 | ||

| (Transfer of Drawings to Capital A/cs) | ||||

| March 31 | Depreciation A/c ...Dr. | 3,08,000 | - | |

| To Furniture and Fixtures A/c | - | 8,000 | ||

| To Computers A/c | - | 3,00,000 | ||

| (Depreciation provided) | ||||

| March 31 | Telephone Charges A/c ...Dr. | 6,800 | - | |

| To Outstanding Telephone Charges A/c | - | 6,800 | ||

| (Outstanding telephone charges) | ||||

| March 31 | Profit and Loss A/c ...Dr. | 2,10,000 | - | |

| To Profit and Loss Appropriation A/c | - | 2,10,000 | ||

| (The transfer of Profit to Profit and Loss Appropriation Account) | ||||

| March 31 | Interest on Capital A/c ...Dr. | 1,20,000 | - | |

| To Banerjee’s Capital A/c | - | 48,000 | ||

| To Chatterjee’s Capital A/c | - | 40,000 | ||

| To Diwedi’s Capital A/c | - | 32,000 | ||

| (The Interest on partner’s Capitals) | ||||

| March 31 | Profit and Loss Appropriation A/c ...Dr. | 1,20,000 | - | |

| To Interest on Capital A/c | - | 1,20,000 | ||

| (The transfer of interest on Capital to Profit and Loss Appropriation Account) | ||||

| March 31 | Profit and Loss Appropriation A/c ...Dr. | 90,000 | - | |

| To Banerjee’s Capital A/c | - | 30,000 | ||

| To Chatterjee’s Capital A/c | - | 30,000 | ||

| To Diwedi’s Capital A/c | - | 30,000 | ||

| (The transfer of credit balance of Profit and Loss Appropriation Account to partner’s Capital Accounts) | ||||

LEDGER:

| BANK ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2022 | ||||||

| April l | To Banerjee’s Capital A/c | 6,00,000 | April l | By Computers A/c | 10,00,000 | ||

| To Chatterjee’s Capital A/c | 5,00,000 | April l | By Electricity Board A/c | 20,000 | |||

| To Diwedi’s Capital A/c | 4,00,000 | April l | By VSNL A/c | 1,50,000 | |||

| April l | By Furniture and Fixtures A/c | 40,000 | |||||

| 2023 | 2023 | ||||||

| March 31 | To Revenue from Fees and Sales A/c | 11,28,000 | March 31 | By Advertisement A/c | 6,000 | ||

| March 31 | By Purchases A/c | 92,000 | |||||

| March 31 | By Wages A/c | 60,000 | |||||

| March 31 | By Electricity Charges A/c | 2,40,000 | |||||

| March 31 | By Telephone Charges A/c | 73,000 | |||||

| March 31 | By Entertainment Exp. A/c | 7,000 | |||||

| March 31 | By General Exp. A/c | 5,200 | |||||

| March 31 | By Rent A/c | 1,20,000 | |||||

| March 31 | By Drawings A/c: | ||||||

| Banerjee | 50,000 | ||||||

| Chatterjee | 40,000 | ||||||

| Diwedi | 20,000 | ||||||

| March 31 | By Balance c/d | 7,04,800 | |||||

| 26,28,000 | 26,28,000 | ||||||

| 2023 | |||||||

| April 1 | To Balance b/d | 7,04,800 | |||||

| CAPITAL ACCOUNTS | |||||||||

| Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

| 2023 | 2022 | ||||||||

| March 31 | To Drawings A/c | 50,000 | 40,000 | 20,000 | April 1 | By Bank A/c | 6,00,000 | 5,00,000 | 4,00,000 |

| March 31 | To Balance c/d | 5,50,000 | 4.60,000 | 3.80,000 | |||||

| 6,00,000 | 5,00,000 | 4,00,000 | 6,00,000 | 5,00,000 | 4,00,000 | ||||

| COMPUTERS ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April l | To Bank A/c | 6,00,000 | March 31 | By Depreciation A/c | 3,00,000 | ||

| March 31 | By Balance c/d | 7,00,000 | |||||

| 10,00,000 | 10,00,000 | ||||||

| 2023 | |||||||

| April 1 | To Balance b/d | 7,00,000 | |||||

| ELECTRICITY BOARD ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April l | To Bank A/c | 20,000 | March 31 | By Balance c/d | 20,000 | ||

| 2023 | |||||||

| April 1 | To Balance b/d | 20,000 | |||||

| VSNL ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April l | To Bank A/c | 1,50,000 | March 31 | By Balance c/d | 1,50,000 | ||

| 2023 | |||||||

| April 1 | To Balance b/d | 1,50,000 | |||||

| FURNITURE AND FIXTURES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2022 | 2023 | ||||||

| April l | To Bank A/c | 40,000 | March 31 | By Depreciation A/c | 8,000 | ||

| March 31 | By Balance c/d | 32,000 | |||||

| 40,000 | 40,000 | ||||||

| 2023 | |||||||

| April 1 | To Balance b/d | 32,000 | |||||

| ADVERTISEMENT ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 6,000 | March 31 | By P & L A/c | 6,000 | ||

| PURCHASES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 92,000 | March 31 | By Trading A/c | 92,000 | ||

| PURCHASES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 92,000 | March 31 | By Trading A/c | 92,000 | ||

| REVENUE FROM FEES AND SALES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Trading A/c | 11,28,000 | March 31 | By Bank A/c | 11,28,000 | ||

| WAGES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 60,000 | March 31 | By Trading A/c | 60,000 | ||

| ELECTRICITY CHARGES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 2,40,000 | March 31 | By P & L A/c | 2,40,000 | ||

| TELEPHONE CHARGES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 73,000 | March 31 | By P & L A/c | 79,800 | ||

| March 31 | To Outstanding Telephone Charges A/c | 6,800 | |||||

| 79,800 | 79,800 | ||||||

| ENTERTAINMENT EXPENSES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 7,000 | March 31 | By P & L A/c | 7,000 | ||

| GENERAL EXPENSES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 5,200 | March 31 | By P & L A/c | 5,200 | ||

| RENT ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Bank A/c | 1,20,000 | March 31 | By P & L A/c | 1,20,000 | ||

| DEPRECIATION ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Furniture and Fixtures A/c | 8,000 | March 31 | By P & L A/c | 3,08,000 | ||

| March 31 | To Computers A/c | 3,00,000 | |||||

| 3,08,000 | 3,08,000 | ||||||

| OUTSTANDING TELEPHONE CHARGES ACCOUNT | |||||||

| Date | Particulars | L.F. | Amount (₹) |

Date | Particulars | L.F. | Amount (₹) |

| 2023 | 2023 | ||||||

| March 31 | To Balance c/d | 6,800 | March 31 | By Telephone Charges A/c | 6,800 | ||

| 2023 | |||||||

| April 1 | By Balance b/d | 6,800 | |||||

| DRAWINGS ACCOUNTS | |||||||||

| Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

| 2023 | 2023 | ||||||||

| March 31 | To Bank A/c | 50,000 | 40,000 | 20,000 | March 31 | By Capital A/c | 50,000 | 40,000 | 20,000 |

| TRIAL BALANCE as at 31st March, 2023 | |||||

| Name of Accounts | L.F. | Balance Dr. (₹) |

Name of Accounts | L.F. | Balance Cr. (₹) |

| Bank A/c | 7,04,800 | Banerjee’s Capital A/c | 6,00,000 | ||

| Computers A/c | 7,00,000 | Chatterjee’s Capital A/c | 5,00,000 | ||

| Electricity Board A/c | 20,000 | Diwedi’s Capital A/c | 4,00,000 | ||

| VSNL A/c | 1,50,000 | Revenue from Fees and Sales A/c | 11,28,000 | ||

| Furniture & Fixtures A/c | 32,000 | Outstanding Telephone Charges A/c | 6,800 | ||

| Advertisement A/c | 6,000 | ||||

| Purchases A/c | 92,000 | ||||

| Wages A/c | 60,000 | ||||

| Electricity Charges A/c | 2,40,000 | ||||

| Telephone Charges A/c | 79,800 | ||||

| Entertainment Expenses A/c | 7,000 | ||||

| General Expenses A/c | 5,200 | ||||

| Rent A/c | 1,20,000 | ||||

| Banerjee’s Drawings A/c | 50,000 | ||||

| Chatterjee’s Drawings A/c | 40,000 | ||||

| Diwedi’s Drawings A/c | 20,000 | ||||

| Depreciation A/c | 3,08,000 | ||||

| 26,34,800 | 26,34,800 | ||||

| TRADING AND PROFIT & LOSS ACCOUNT for the year ending 31st March, 2023 | ||||||

| Particulars | L.F. | Amount (₹) |

Amount (₹) |

Particulars | L.F. | Amount (₹) |

| To Purchases A/c | 92,000 | By Revenue from Fees and Sales A/c | 11,28,000 | |||

| To Wages A/c | 60,000 | |||||

| To Gross Profit transferred to P & L A/c | 9,76,000 | |||||

| 11,28,000 | 11,28,000 | |||||

| To Advertisement A/c | 6,200 | 9,76,000 | ||||

| To Electricity Charges A/c | 2,40,000 | |||||

| To Telephone Charges A/c | 79,800 | |||||

| To Entertainment Expenses A/c | 7,000 | |||||

| To General Expenses A/c | 5,200 | |||||

| To Rent A/c | 1,20,000 | |||||

| To Depreciation A/c: | ||||||

| Furniture and Fixtures | 8,000 | |||||

| Computers | 3,00,000 | 3,08,000 | ||||

| To Net Profit transferred to Profit & Loss Appropriation A/c | 2,10,000 | |||||

| 9,76,000 | 9,76,000 | |||||

| PROFIT & LOSS APPROPRIATION ACCOUNT for the year ending 31st March, 2023 | ||||||

| Particulars | L.F. | Amount (₹) |

Amount (₹) |

Particulars | L.F. | Amount (₹) |

| To Interest on Capital: | By Profit & Loss A/c (Net Profit) | 2,10,000 | ||||

| Banerjee | 48,000 | |||||

| Chatterjee | 40,000 | |||||

| Diwedi | 32,000 | 1,20,000 | ||||

| To Profit Transferred to: | ||||||

| Banerjee’s Capital A/c | 30,000 | |||||

| Chatterjee’s Capital A/c | 30,000 | |||||

| Diwedi’s Capital A/c | 30,000 | 90,000 | ||||

| 2,10,000 | 2,10,000 | |||||

| PARTNER'S CAPITAL ACCOUNTS (AFTER APPROPRIATIONS) | |||||||||

| Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

Date | Particulars | Banerjee (₹) |

Chatterjee (₹) |

Diwedi (₹) |

| 2023 | 2023 | ||||||||

| March 31 | To Balance A/c | 6,28,000 | 5,30,000 | 4,42,000 | March 31 | By balance b/d (Net, after Drawings) | 5,50,000 | 4,60,000 | 3,80,000 |

| March 31 | By Interest on Capital | 48,000 | 40,000 | 32,000 | |||||

| March 31 | By Profit & Loss Appropriation A/c | 30,000 | 30,000 | 30,000 | |||||

| 6,28,000 | 5,30,000 | 4,42,000 | 6,28,000 | 5,30,000 | 4,42,000 | ||||

| BALANCE SHEET as at 31st March, 2023 | |||||

| Particulars | Amount (₹) |

Amount (₹) |

Particulars | Amount (₹) |

Amount (₹) |

| Outstanding Telephone Charges | 6,800 | Bank | 7,04,800 | ||

| Capital Accounts: | Electricity Board (Security Deposit) | 20,000 | |||

| Banerjee | 6,28,000 | VSNL (Security Deposit) | 1,50,000 | ||

| Chatterjee | 5,30,000 | Furniture and Fixtures (Less Dep.) | 32,000 | ||

| Diwedi | 4,42,000 | 16,00,000 | Computers (Less Dep.) | 7,00,000 | |

| 16,06,800 | 16,06,800 | ||||

Profitability Ratios:

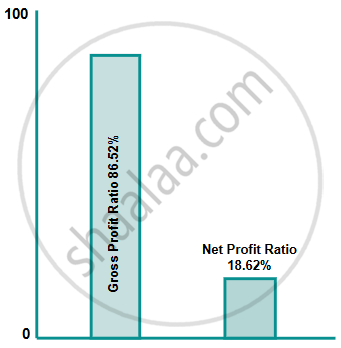

- `"Gross Profit Ratio"=("Gross Profit")/("Net Revenue from Operations")xx100`

`=(9,76,000)/(11,28,000)xx100`

`=86.52%` - `"Net Profit Ratio"=("Net Profit")/("Net Revenue from Operations")xx100`

`=(2,10,000)/(11,28,000)xx100`

`=18.62%`

- Progressive Computers’ Gross Profit Ratio is 86.52% compared to 60% in similar types of business enterprises (as stated in the question).

- Progressive Computers’ Net Profit Ratio is 18.62% compared to 15% in similar types of business enterprises (as stated in the question).

Comments: Efficiency of Progressive Computers’ is quite good since Gross Profit Ratio and Net Profit Ratio are sufficiently higher than the norms set for similar types of business enterprises.

Granting of Loan:

In addition to Gross Profit Ratio and Net Profit Ratio, the Bank will also consider the following ratios before granting the loan:

- `"Current Ratio"=("Current Assets")/("Current Liabilities")`

- `"Quick Ratio"=("Liquid Assets")/("Current Liabilities")`

- `"Debt Equity Ratio"=("Long term Debts")/("Equity")`

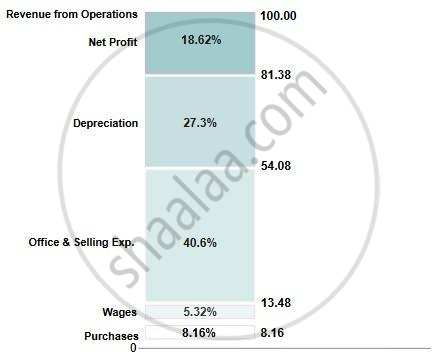

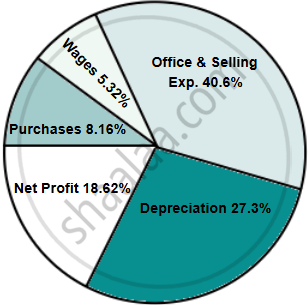

PRESENTATION OF INFORMATION:

| Revenue from Operations (Sales) | 11,28,000 | Sales 100% | Cumulative Percentages |

| Purchases | 92,000 | 8.16% | 8.16% |

| Wages | 60,000 | 5.32% | 13.48% |

| Office & Selling Exp. | 4,58,000 | 40.60% | 54.08% |

| Depreciation | 3,08,000 | 27.30% | 81.38% |

| Net Profit | 2,10,000 | 18.62% | 100.00% |

| 11,28,000 | 100 |

BAR DIAGRAM:

PIE CHART:

DEPICTION OF RATIOS: