ISC (Commerce)

Academic Year: 2025-2026

Date: मार्च 2026

Advertisements

Instructions to Candidates:

- You are allowed an additional fifteen minutes for only reading the paper.

- You must NOT start writing during reading time.

- This Question Paper has 16 printed pages.

- It is divided into three sections and has 18 questions in all.

- Section A is compulsory and has ten questions.

- You are required to attempt all questions either from Section B or Section C.

- Section B and Section C have four questions each.

- Internal choices have been provided in five questions in Section A and in two questions each in Section B and Section C.

- While attempting Multiple Choice Questions in Sections A, B and C, you are required to write only ONE option as the answer.

- All calculations should be shown clearly.

- All workings, including rough work, should be done on the same page as, and adjacent to, the rest of the answer.

- The intended marks for questions or parts of questions are given in the brackets [].

Anil and Sunil are partners in a firm. On 1st April 2024, their capital balances show as ₹ 3,00,000 and ₹ 2,00,000 respectively. On the same date, firm’s goodwill valued by Capitalisation of average profit method is determined at ₹ 3,50,000. Capitalised value of average profits and average profits are ₹ 8,50,000 and ₹ 1,70,000 respectively. What will be the normal commercial yield on capital invested in such business?

30%

10%

20%

15%

Chapter:

Akhil, Viren and Sarla are partners in a firm who share profits in 4 : 3 : 3 ratio. On the date of Sarla’s retirement from the firm, the books show the workmen compensation reserve of ₹ 12,000.

Akhil and Viren decide to share profit in equal ratio after Sarla’s retirement.

Choose the correct journal for the treatment of workmen compensation reserve if the continuing partners decide to show workmen compensation reserve in the reconstituted balance sheet.

Debit workmen compensation reserve A/c ₹ 12,000; Credit Akhil’s Capital A/c ₹ 4,800; Credit Viren’s Capital A/c ₹ 3,600 and Sarla’s Capital A/c ₹ 3,600

Debit workmen compensation reserve A/c ₹ 3,600 and Credit Sarla’s Capital A/c ₹ 3,600.

Debit Sarla’s Capital A/c ₹ 3,600; Credit Akhil’s Capital A/c ₹ 1,200 and Credit Viren’s Capital A/c ₹ 2,400.

Debit Akhil’s Capital A/c ₹ 1,200; Debit Viren’s Capital A/c ₹ 2,400 and Credit Sarla’s Capital A/c ₹ 3,600.

Chapter:

On 1st April 2023, Anand Limited issued 10%, 50,000 Debentures of ₹ 100 each as collateral security to ABC Bank against a loan raised of ₹ 80,00,000. It also issued 12%, 40,000 Debentures of ₹ 100 each on 1st October, 2023 in the stock market to invest money in a new line of product.

How much interest on debentures becomes payable by the company on 31st March 2024?

₹ 7,40,000

₹ 2,40,000

₹ 5,00,000

₹ 4,80,000

Chapter:

Choose the correct sequence of various types of guarantees of profit used while preparing profit and loss appropriation account by a partnership firm.

(P) Guarantee given by the firm to partners

(Q) Guarantee given by a partner to the firm

(R) Guarantee given by a partner to another partner

P, Q, R

Q, P, R

R, P, Q

Q, R, P

Chapter:

On dissolution of a firm, one of the partners, Abhi demands that his loan of ₹ 1,50,000 be paid before payment of capitals of the partners, whereas other partners, Bobby and Cathy demand that capitals should be paid before the payment of Abhi’s loan. State the correct order of payment. Give a reason for your answer.

Chapter:

Rahul and Nikhil are partners in a firm. They admit Tanvi for `1/5`th share. On the date of her admission, the firm’s book shows the following balances:

Rahul’s Capital: ₹ 2,80,000

Nikhil’s Capital: ₹ 2,20,000

Tanvi contributes 20% of the adjusted capital of Rahul and Nikhil. She also contributes ₹ 20,000 as half of her share of goodwill.

Pass the journal entry to record the capital contribution made by Tanvi.

Chapter:

Priya was a partner in a firm. On the date its dissolution, her loan was appearing on the liability side of the balance sheet at ₹ 25,000. Priya accepted an unrecorded asset of ₹ 17,500 and the balance was paid to her in cash.

Give the Journal entry for the above transaction.

Chapter:

Enumerate two methods of redemption of debentures.

Chapter:

Manilal Ltd, is a manufacturing company. Its operating cycle is 15 months. On 31st March, 2025, its trade receivable of ₹ 70,000 includes ₹ 20,000 which is due to be collected on 13th April, 2026 and the remaining after 30th June, 2026.

You are required to calculate current and non-current assets of the company as at 31st March, 2025.

Chapter:

Assertion: Forfeited shares can be reissued at a discount.

Reason: The amount received by a company on forfeited shares can be used to cover the discount on the reissues of forfeited shares.

Which one of the following is correct?

Both Assertion and Reason are true and Reason is the correct explanation for Assertion.

Both Assertion and Reason are true but Reason is not the correct explanation for Assertion.

Assertion is true and Reason is false.

Both Assertion and Reason are false.

Chapter:

Amit, Karan and Rakhi were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. Amit died on 30th June 2024 while the firm closed its books on 31st March. According to their partnership deed, Amit’s representative would be entitled to get a share in the interim profits of the firm calculated on the basis of turnover. Turnover and profit for the year 2023-24 were ₹ 3,00,000 and ₹ 90,000 respectively and turnover in the year 2024-25 till the date of his death amounted to ₹ 60,000.

You are required to:

- Calculate Amit’s share of interim profit. (1)

- Pass the necessary Journal entry showing Amit’s share of interim profit. (2)

Chapter:

Pratik, Krish and Susan are partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. On 31st March, 2024, Krish retires and `1/3` of his share is taken by Pratik and the balance by Susan.

The extract of the Balance Sheet as at 31.03.2024 is as follows:

| Balance Sheet (Extract) of Pratik, Krish and Susan As at 31.3.24 |

|||||

| Liabilities | ₹ | ₹ | Assets | ₹ | ₹ |

| Investment Fluctuation Reserve | 8,000 | Investment | 52,000 | ||

| Employee Provident Fund | 12,000 | Debtors | 20,000 | 18,000 | |

| Less: P.D.D | (2,000) | ||||

| Capital Accounts: | |||||

| Pratik | 50,000 | 1,03,000 | |||

| Krish | 32,500 | ||||

| Susan | 21,000 | ||||

Other information:

- Bad debts amounted to ₹ 3,000.

- Remaining debtors are all good.

- Market value of the investments is ₹ 40,000.

- Krish was given investments in full settlement.

You are required to pass the journal entries on the date of Krish’s retirement.

Chapter:

On 1st April, 2024, Zeba Ltd. purchased a running business having a net worth of ₹ 2,00,000 from Ajay Ltd. for a purchase consideration of ₹ 2,10,000. The payment was made as follows:

- By issuing 9,000, 10% Debentures of ₹ 10 each at a premium of 20%.

- Balance by accepting a Bills of Exchange payable after 3 months.

You are required to pass journal entries in the books of Zeba Ltd.

(Ignore interest on Debentures).

Chapter:

On 1st April, 2024, Zubin Ltd. issued 3,000, 8% Debentures of ₹ 100 each at a discount of 5% to be redeemed after two years at a premium of 6%.

On 31st March, 2025, Zubin Ltd. had the following balances in its books before adjustments of capital losses:

| Securities Premium | ₹ 23,000 |

| Statement of Profit/Loss | ₹ 18,000 |

| General Reserve | ₹ 20,000 |

The company writes off all its capital losses in the same year.

You are required to prepare the following for the year 2024-2025:

- Loss on Issue of Debentures A/c (2)

- Securities Premium A/c (1)

Chapter:

APL Ltd., an unlisted construction company has 50,000, 10% Debentures of ₹ 100 each due for redemption at par on 31st March, 2024. The Debenture Redemption Investment was purchased on 30th April, 2023 and was sold on the date of redemption at 104% less 0.7% commission. APL Ltd. had sufficient balance in its Debenture Redemption Reserve A/c as per the provisions of the Companies’ Act, 2013.

You are required to prepare the following Ledger Accounts for the year 2023-2024:

- Debenture Redemption Reserve A/c (1)

- Debenture Redemption Investment A/c (2)

Chapter:

From the following information, calculate goodwill by Capitalisation of Super profit method for a firm run by Akshay and Baldev:

| Particulars | ₹ |

| Akshay’s Capital A/c | 1,20,000 |

| Baldev’s Capital A/c | 1,00,000 |

| Akshay’s Current A/c | 20,000 |

| Baldev’s Current A/c (Dr.) | 10,000 |

| General Reserve | 20,000 |

| Advertisement Suspense A/c | 10,000 |

Other information:

- Normal rate of return is 10% p.a.

- Trading profits for the preceding four years are as follows:

- 2021-2022 - ₹ 40,000

- 2022-2023 - ₹ 45000

- 2023-2024 - ₹ 50,000 (including loss by theft 5,000)

- 2024-2025 - ₹ 60000 (excluding depreciation on machinery ₹ 6,000)

Chapter:

On 31st March 2025, Rishiraj Ltd., an unlisted construction company, showed the following balances:

| Particulars | Amount (₹) |

| Equity Share Capital of ₹ 10 each | 10,00,000 |

| Calls-in-arrear (₹ 2 per share) | 30,000 |

| 8% Debenture of ₹ 100 each | 4,00,000 |

| 6% Bank Loan | 2,10,000 |

| Bank Overdraft | 54,000 |

| Cash Credit | 12,000 |

| Debenture Redemption Reserve | 40,000 |

| Premium on redemption of debentures | 20,000 |

| Interest on 8% Debentures due on 31.3.2025 has not been paid | 32,000 |

You are required to prepare an extract of Balance Sheet as at 31st March, 2025, showing the Equity and Liabilities. (Ignore Notes to Accounts)

Chapter:

Anu and Binu were partners sharing profits and losses in the ratio of 4 : 1. Their Balance sheet as at 31st March, 2025 was as follows:

| Balance sheet of Anu and Binu As at 31st March 2025. |

||||

| Liabilities | ₹ |

₹ | Assets | ₹ |

| Capital Accounts: | Bank | 26,000 | ||

| Anu | 25,000 | 35,000 | ||

| Binu | 10,000 | |||

| General Reserve | 10,000 | Building | 49,000 | |

| Bills Payable | 40,000 | Goodwill | 1,000 | |

| Debtors | 9,000 | |||

| 85,000 | 85,000 | |||

On 1st April 2025, Tinu is admitted as a new partner on the following terms:

- New profit-sharing ratio of the partners to be 2 : 1 : 1.

- Tinu shall bring in ₹ 16,000 as his capital and the required amount of goodwill in cash.

- Bills payable was overvalued by ₹ 2,000.

- The value of goodwill of the firm to be calculated on the basis of Tinu’s share in profit and the capital contributed by him.

- Provision for bad and doubtful debts ₹ 1,000 to be created out of General Reserve.

Pass the journal entries for treatment of goodwill and prepare Capital accounts of all the partners.

Chapter:

Advertisements

Tony and Sony are partners in a firm sharing profits and losses in the ratio of 4 : 3. On 1st April, 2025, they admit Ronny for `1/3` share in the profits.

Other information:

(a) Ronny brought in Land and Building worth ₹ 5,00,000 and Furniture worth ₹ 50,000 but was unable to contribute any amount for his share of Goodwill.

(b) At the time of Ronny’s admission, the firm showed the following balances:

| Advertisement Suspense A/c | ₹ 49,000 |

| General Reserve | ₹ 56,000 |

| Profit and Loss A/c (Dr) | ₹ 70,000 |

| Goodwill | ₹ 42,000 |

| Employees’ Provident Fund | ₹ 21,000 |

| Loan from Sony (taken on 1st January 2025) | ₹ 1,00,000 |

(c) Revaluation loss amounted to ₹ 7,000.

(d) Goodwill of the firm valued at ₹ 21,000.

You are required to:

- Pass journal entries for the above transactions on the date of Ronny’s admission.

- Pass journal entries regarding loan taken from Sony for the year 2024-25.

(Interest on loan is still due to be paid.)

Chapter:

Hima, Zoya and Bhanu were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. They decided to dissolve the firm on 1st April, 2025. Their Balance Sheet as at 31.3.2025 was as follows.

| Balance Sheet of Hima, Zoya and Bhanu As at 31.3.2025 |

|||

| LIABILITIES | ₹ | ASSETS | ₹ |

| Capital: Hima | 50,000 | Plant | 48,000 |

| Zoya | 80,000 | Furniture | 22,000 |

| Workmen’s Compensation Reserve | 15,000 | Investment | 33,000 |

| Investment fluctuation reserve | 22,000 | Stock | 25,000 |

| Trade Creditors | 28,000 | Debtors | 17,000 |

| Hima’s Loan | 12,000 | Cash at bank | 32,000 |

| Bhanu’s capital | 30,000 | ||

| 2,07,000 | 2,07,000 | ||

Additional information:

- Stock was taken by Zoya at 75% of the book value.

- Some trade creditors took over furniture at a reduced value of ₹ 18,000 and the remaining creditors were paid by cheque.

- Plant was realised at 10% less than the book value and one debtor from whom ₹ 2,000 were due could not pay anything.

- An unrecorded liability was settled for ₹ 7,500.

You are required to:

- Prepare Realisation A/c (4)

- Calculate the final settlement with the partners. (2)

Chapter:

Raman, Shivam and Namita are partners sharing profits and losses in the ratio of 1 : 1 : 2. On 31st March, 2024, their books showed the following balances:

| Partners | Capital Account | Current Account | Loan from Partner |

| Raman | ₹ 2,00,000 | ₹ 1,00,000 (Cr.) | |

| Shivam | ₹ 4,00,000 | ₹ 50,000 (Dr.) | ₹ 1,50,000 |

| Namita | ₹ 6,00,000 | ₹ 1,50,000 (Cr.) |

On 1st April, 2024, they adopted the fluctuating capital method of accounting, thereby transferring the current account balances to their capital accounts.

Their partnership deed provided for the following:

- Interest on capital to be allowed @ 10% per annum.

- A monthly allowance of ₹ 8,000, ₹ 6,000 and ₹ 4,000 to be allowed to Raman, Shivam and Namita respectively.

- Interest on loan taken from a partner to be allowed at 10% per annum. Additional loan was taken from Shivam on 1st October, 2024 amounting to ₹ 50,000.

During the year ending 31st March, 2025, the firm earned a net profit of ₹ 5,00,000 before allowing interest on Shivam’s loan.

For the year ending 31st March, 2025 you are required to:

- Prepare Partners’ Capital a/c (6)

- Pass adjusting entry for interest on loan from Shivam. (1)

- Prepare Shivam’s loan account. (2)

- Pass Journal entries for transferring the current account balances of Shivam and Namita to their capital accounts. (1)

Chapter:

Saoli and Paoli are partners in a firm sharing profits and losses equally. The trading profit for the year ending 31st March, 2025 was ₹ 51,800.

Other information:

- Interest on drawings: Saoli ₹ 1,200 and Paoli ₹ 1,000.

- Interest on Paoli’s loan to the firm, not debited in the Profit & Loss a/c ₹ 6,000.

- Interest on capital: Saoli ₹ 20,000 and Paoli ₹ 15,000.

- Salary to partners: Saoli ₹ 15,000 and Paoli ₹ 10,000.

Prepare Profit & Loss Appropriation account for the year ended 31st March, 2025.

Chapter:

Das, Roy and Sen are partners in a firm. The profit of the firm, for the year ended 31st March, 2025, was ₹ 1,20,000 which was equally distributed among them, without providing for the following provisions of the partnership deed:

- Roy had guaranteed that the firm would earn a profit of at least ₹ 1,35,000. Any shortfall in these profits would be personally compensated by him.

- Profits to be shared in the ratio of 2 : 2 : 1.

- Sen is guaranteed by the firm that his share of profits, in any given year, would be a minimum of ₹ 30,000.

You are required to pass the necessary journal entries to rectify the error in accounting on 1st April 2025.

Chapter:

During the year 2023-24, Nikoy Ltd. registered with an authorised capital of 5,00,000 equity shares of ₹ 10 each. It issued 2,00,000 equity shares, the same year, to which 95% applications were subscribed.

During the year 2024-25, Nikoy Ltd.

- Purchased Land & Building costing ₹ 5,00,000 from Agro Housing Ltd. Purchase consideration was settled by issuing sufficient number of Equity shares at 25% premium.

- Issued 10,000 Equity Shares to promoters at par.

- Invited applications for 20,000 equity shares of ₹ 10 each at 25% premium. Entire money was payable on applications. Applications were received for 16,000 shares. Since it did not fulfil the provisions of the Companies’ Act 2013, regarding minimum subscription, the entire application money was refunded within 15 days.

- The company incurred ₹ 22,000 as share issue expenses.

You are required to:

- Pass necessary journal entries for the year 2024-25.

- Calculate the Subscribed Capital of Nikoy Ltd. as at 31st March, 2025.

- Prepare the share issue expenses account.

Chapter:

Maconie Ltd. issued 50,000 Equity Shares of ₹ 10 each at ₹ 15, payable as follows:

- On Application, ₹ 6 including premium of ₹ 2

- On Allotment, ₹ 5 including balance of premium

- Remaining amount on First and Final call after 3 months of shares being allotted applications were oversubscribed. Applications for 5,000 shares were rejected and money refunded immediately, and the remaining applications were allotted on pro rata basis in the ratio of 7:5.

| Journal of Maconie Ltd. | ||||

| Date | Particulars | L.F. | Debit (₹) |

Credit (₹) |

| Bank A/c ...Dr. | ? | |||

| To Share Application A/c | ? | |||

| (Being application money received) | ||||

| Share Application A/c ...Dr. | ? | |||

| To Share Capital A/c | ? | |||

| To Securities Premium A/c | 1,00,000 | |||

| To Bank A/c | 30,000 | |||

| To Share Allotment A/c | ? | |||

| (Being application money transferred and adjusted) | ||||

| Share Allotment A/c ...Dr. | 2,50,000 | |||

| To Share Capital A/c | 1,00,000 | |||

| To Securities Premium A/c | 1,50,000 | |||

| (Being allotment money due) | ||||

| Bank A/c ...Dr. | ? | |||

| To Share Allotment A/c | ? | |||

| To Calls in advance A/c | 8,000 | |||

| (Being allotment money received including amount received for call) | ||||

| Share First & Final Call A/c ...Dr. | 2,00,000 | |||

| To Share Capital A/c | 2,00,000 | |||

| (Being first call money due) | ||||

| Bank A/c ...Dr. | 1,92,000 | |||

| Calls in advance A/c ...Dr. | 8,000 | |||

| To Share First & Final Call A/c | 2,00,000 | |||

| (Being share first & final call money received) | ||||

| Interest on calls in advance A/c ...Dr. | ? | |||

| To Shareholders’ A/c | ? | |||

| (Being interest due on calls in advance as per provisions of Table F of Schedule I of the Company Act, 2013) | ||||

You are required to:

- Complete the entries no. 1, 2, 4 and 7 along with the missing information represented by ‘?’.

- Pass journal entries to pay and close Interest on Calls-in-Advance Account.

Chapter:

Belrise industries, an auto ancillary company, plans to raise ₹ 2,150 crore through a public issue of equity shares. The funds will primarily be used to partly repay its debt.

Which ratios would be impacted by the decision of the Belrise industries?

P. Debt to Equity Ratio

Q. Inventory Turnover Ratio

R. Trade Receivable Turnover Ratio

S. Interest Coverage Ratio

Only P

Only Q and R

Only R and S

Only P and S

Chapter:

Equity shares capital of Royal Ltd. increased from ₹ 40,00,000 to ₹ 50,00,000. The percentage change is ______.

25%

33∙33%

20%

40%

Chapter:

State whether interest received on calls-in-arrear by a company is considered as Operating, Investing or Financing activity.

Chapter:

Given below is an extract of the Cash flow statement of ILO Ltd.

| Particulars | 31.3.2025 (₹) |

31.3.2024 (₹) |

| Net increase/decrease in cash & cash equivalent | (13) | 23 |

| Opening cash and cash equivalent | 17612 | ? |

| Closing cash & cash equivalent | ? | 17612 |

You are required to find out the missing information represented by ‘?’.

Chapter:

| “The current ratio estimates a firm’s capacity of paying short-term or current liabilities, including payables and debts, with its short-term or current assets. A current ratio less than 1.00 implies that the business’s debts due within 12 months are more significant than its assets. Conversely, a ratio greater than 1.00 indicates that the company has sufficient assets to cover its short-term obligations.” |

Based on the above extract, explain why a very high current ratio might not always indicate an optimal financial health.

Chapter:

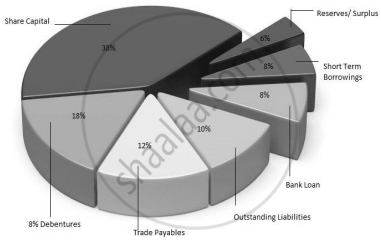

The pie chart below shows the Equity and Liabilities of Moonside Ltd. as at 31st March, 2025.

You are required to prepare the equity and liability side of common size statement of Moonside Ltd. as at 31st March, 2025, when the total of the Equity and Liabilities side is ₹ 10,00,000.

Chapter:

Calculate the debt to equity ratio from the given information:

| Particulars | (₹) |

| Current Liabilities | ₹ 3,50,000 |

| Working Capital | ₹ 2,00,000 |

| Non-current Assets | ₹ 8,00,000 |

| Shareholders’ funds | ₹ 6,00,000 |

Chapter:

Calculate the inventory turnover ratio if:

- Cost of Revenue from operations is ₹ 3,20,000.

- Gross profit is 20% of Revenue from Operations.

- Closing inventory is 4 times of opening inventory.

- Opening inventory is 10% of Revenue from operations.

Chapter:

Calculate the operating ratio from the information given below.

| Particulars | (₹) |

| Opening Inventory | 20,000 |

| Closing inventory | 9,000 |

| Purchases | 80,000 |

| Wages | 8,000 |

| Carriage inward | 3,000 |

| Depreciation | 18,000 |

| Amortization | 6,000 |

| Gross Profit | 48,000 |

Chapter:

The Quick ratio of the company is 2 : 1. State if the following would improve, reduce or not change the ratio:

- Bills receivable discounted dishonoured on due date.

- Debentures issued for purchase of Plant and machinery.

Chapter:

Advertisements

From the following Balance Sheets of Kiosk Ltd. you are required to prepare a Cash Flow Statement (As per AS 3) for the period ended 2024-25.

| Balance Sheets of Kiosk Ltd. As at 31st March, 2025 and 31st March, 2024 |

|||

| Particulars | Note No. |

31.3.2025 (₹) |

31.3.2024 (₹) |

| I. EQUITY AND LIABILITIES | |||

| 1. Shareholders’ Funds | |||

| (a) Share Capital | 8,50,000 | 5,50,000 | |

| (b) Reserves and Surplus (Statement of P/L) | 1,80,000 | 1,00,000 | |

| 2. Non-Current Liabilities | |||

| Long-term Borrowings (8% Debentures) | 50,000 | 2,00,000 | |

| 3. Current Liabilities | |||

| (a) Short-term borrowings (Bank Overdraft) | 1,25,000 | 1,15,000 | |

| (b) Short-Term Provisions (Provision for tax) | 95,000 | 1,35,000 | |

| TOTAL | 13,00,000 | 11,00,000 | |

| II. ASSETS | |||

| 1. Non-Current Assets: | |||

| Property, Plant & Equipment & Intangible Assets | |||

| (i) Property, Plant & Equipment | 7,50,000 | 5,50,000 | |

| (ii) Intangible assets (Patent) | 1,40,000 | 85,000 | |

| 2. Current Assets | |||

| (a) Current Investments | 65,000 | 1,45,000 | |

| (b) Trade Receivables | 1,95,000 | 2,05,000 | |

| (c) Cash & Bank Balances (Cash at Bank) | 1,50,000 | 1,15,000 | |

| TOTAL | 13,00,000 | 11,00,000 | |

Notes to Accounts:

| Particulars | 31.3.2025 ₹ |

31.3.2024 ₹ |

| 1) Property, plant and equipment | 8,15,000 | 5,85,000 |

| Accumulated depreciation | (65,000) | (35,000) |

Additional Information:

- A Machinery costing ₹ 30,000 (depreciation provided thereon ₹ 10,000) was sold at a loss of ₹ 3,000.

- Tax provided for the year 2024-25 ₹ 32,000.

- 8% Debentures were redeemed on 31.3.2025.

- Interest received on current investments was ₹ 2,500.

Chapter:

Prepare a cash flow statement showing cash generated from the operation of Solex Ltd. for the year ended 31.3.2025.

Net profit for the year ended 31.3.2025 was ₹ 1,25,000 after considering the following items:

| Depreciation on plant | ₹ 17,500 |

| Transfer to general reserve | ₹ 13,500 |

| Provision for tax | ₹ 15,000 |

| Provision for doubtful debt | ₹ 1,600 |

Note: All Debtors are good.

Position of Current assets & current liabilities:

| Particulars | 31.3.2025 (₹) |

31.3.2024 (₹) |

| Trade receivable | 27,000 | 28,000 |

| Trade payable | 12,000 | 17,000 |

| Current investment | 24,000 | 18,000 |

| Marketable securities | 9,000 | 7,000 |

Chapter:

Following is the information provided for Creation Ltd. for the year ended 31.3.2025:

- Equity share capital of ₹ 10 each increased from ₹ 10,00,000 to ₹ 15,00,000.

- 12%, 3,000 Debentures of ₹ 100 each redeemed on 30.9.2024.

- Proposed dividend on equity shares for the previous year was ₹ 1,50,000.

- 12%, 20,000 Preference shares of ₹ 100 each issued at par on 31.3.2025.

- Out of the equity share capital issued, ₹ 1,00,000 issued for consideration other than cash for purchase of machinery.

You are required to ascertain cash flow from the financing activity.

Chapter:

Which one of the following keys is used to uniquely identify a record in a table?

Foreign Key

Primary Key

Composite Key

Alternate Key

Chapter:

Which one of the following keys is the standard short key in MS Excel to ‘Paste’?

Ctrl + Z

Ctrl + V

Ctrl + X

Ctrl + Y

Chapter:

How is a cell range specified in a spreadsheet?

Chapter:

Define composite attribute with suitable examples.

Chapter:

Differentiate between Desktop Database and Server Database.

Chapter:

What is the use of ‘Sort’ option in accounting spreadsheets?

Chapter:

What is the use of ‘Filter’ option in accounting spreadsheets?

Chapter:

Mink & Sons run a bakery that sells sandwiches, cookies, muffins and pastries. The raw material is sourced from a well-known supplier and fresh items are prepared every day for the customers. The cost of each item also includes the cost of cutlery and paper napkins.

During the festive season, the bakery gives small discounts to its customers.

The spread sheet given below is a summary of its Purchases, Sales and Unsold Stock for the month of October 2023:

| A | B | C | D | E | F | G | H | I | J | K | |

| 1 | Bakery items | No. of items prepared | Cost price per item (₹) | Total cost (₹) | No. of items sold | List price per item (₹) | Festival Discount per item (₹) | Total sales (₹) | Cost of items sold (₹) | Cost of unsold stock (₹) | Profit (₹) |

| 2 | Sandwiches | 275 | 80 | 22,000 | 220 | 105 | 5 | ?? | 17,600 | 4,400 | 4,400 |

| 3 | Cookies | 250 | 50 | 12,500 | 220 | 75 | 5 | 15,400 | ?? | 1,500 | 4,400 |

| 4 | Muffins | 330 | 40 | 13,200 | 300 | 75 | 5 | 21,000 | 12,000 | ?? | 9,000 |

| 5 | Pastries | 225 | 60 | 13,500 | 200 | 95 | ?? | 18,000 | 12,000 | 1,500 | 6,000 |

| 6 | Total | 1,080 | 61,200 | 940 | 23,800 |

Based on the above transactions and the information given in the spreadsheet, answer the following questions:

- Write the formula to calculate the total sales of sandwiches in cell H2.

- Give the formula to calculate the cost of cookies sold in cell I3

- Write the formula to calculate the cost of unsold stock of muffins in cell J4.

-

- Give the formula to calculate the festival discount on the sale of Pastries in cell G5.

- Calculate the amount of festival discount per pastry in cell G5.

Chapter:

Other Solutions

Submit Question Paper

Help us maintain new question papers on Shaalaa.com, so we can continue to help studentsonly jpg, png and pdf files

CISCE previous year question papers Class 12 Accounts with solutions 2025 - 2026

Previous year Question paper for CISCE Class 12 -2026 is solved by experts. Solved question papers gives you the chance to check yourself after your mock test.

By referring the question paper Solutions for Accounts, you can scale your preparation level and work on your weak areas. It will also help the candidates in developing the time-management skills. Practice makes perfect, and there is no better way to practice than to attempt previous year question paper solutions of CISCE Class 12.

How CISCE Class 12 Question Paper solutions Help Students ?

• Question paper solutions for Accounts will helps students to prepare for exam.

• Question paper with answer will boost students confidence in exam time and also give you an idea About the important questions and topics to be prepared for the board exam.

• For finding solution of question papers no need to refer so multiple sources like textbook or guides.