Definitions [33]

A chequebook contains several blank cheques, which can be used when payments or money transfers are needed. Banks give a chequebook to their account holders if they keep a certain minimum balance.

A cheque is said to be bounced or dishonoured when the bank refuses to pay the amount written on the cheque.

A cheque is a written order from an account holder to their bank to pay a specified amount to another person or the bearer (anyone physically holding or presenting it). It is mostly valid for 3 months from the date of issue.

A cash book is a special account book where all business cash and bank transactions (money received and paid) are recorded each day.

A simple cash book is a special accounting book that records only cash transactions (cash receipts and cash payments) of an organization, acting both as a journal and a ledger for these entries.

A petty cash book is a type of cash book in accounting that records all minor, routine cash payments and receipts separately from the main cash book.

A petty cashier is responsible for handling petty cash and maintaining the petty cash book.

A Purchase Book (also called Bought Day Book or Purchase Journal) is used to record only credit purchases of goods intended for resale or production.

A sales book is a special accounting record used to write down all the credit sales of goods made by a business, while cash sales or sales of assets are recorded elsewhere.

A purchase return book is a special accounting book where a business records goods sent back to suppliers because they are the wrong quality, damaged, or not needed—only returns from credit purchases are included.

A debit note is a brief statement prepared by the buyer when returning goods, showing the details and amount of goods returned, and letting the supplier know to reduce the buyer’s amount owed.

A credit note is a document given by a seller to a buyer when goods are returned, showing the amount to reduce or cancel what the buyer has to pay; it acts like a “refund slip” that adjusts the buyer’s account and proves the return happened.

The Sales Return Book is a special accounting book used to record goods that were sold to customers on credit but are returned to the business because they are not as ordered, damaged, or defective.

Journal Proper is a special accounting book where rare or miscellaneous transactions, not recorded in other subsidiary books, are entered.

The Accounting Equation shows that everything a business owns (Assets) is funded by either money borrowed from outsiders (Liabilities) or money invested by the owner (Capital).

A voucher is a formal written document that supports and records a financial transaction in business or accounting.

A computerised ledger software is a computer program that helps record, organize, and manage all financial transactions quickly and accurately.

Balancing a ledger account means adding up the debit and credit columns, finding the difference, and inserting this difference as 'Balance c/d' (carried down) on the side that totals less. This final balance is then brought forward for the next accounting period as 'Balance b/d' (brought down)

Posting is the process of transferring each entry from the journal or subsidiary books into the appropriate ledger account.

A Bank Reconciliation Statement is an accounting statement prepared to compare the balance shown in a company’s cash book with the balance shown in the bank statement, listing and explaining any differences, so records are accurate and complete.

A trial balance is a statement that lists the debit and credit balances of all ledger accounts on a specific date to check the mathematical accuracy of the books.

Errors in accounting mean mistakes made while recording, posting, or calculating financial transactions, like forgetting an entry or entering a wrong amount.

Rectification of accounting errors means finding and fixing these mistakes so that the financial results and statements show the true picture.

A suspense account is a temporary account created when the trial balance does not tally because of unknown errors.

Rectification of accounting errors means correcting mistakes made while recording financial transactions so that the accounts show true and accurate financial information.

A rectifying entry means a journal entry made to correct a mistake in the books of accounts by canceling the wrong entry and recording the correct one.

Depreciation means a gradual decrease in the value of fixed assets like buildings, machinery, furniture, and equipment due to their use, passage of time, or technological changes.

It is a method of depreciation where the same (fixed) amount is reduced from an asset’s value every year until it reaches its scrap value or end of life.

The Written Down Value (WDV) Method is a way to calculate depreciation where a fixed percentage is charged every year on the asset’s current book value (its remaining value after previous depreciation), making the depreciation amount decrease each year as the asset’s value reduces.

Making payment of bill well before the date of maturity is known as retirement of bill.

Section 4 of the Negotiable Instruments Act, 1881defines Promissory Note as: “A Promissory Note is defined as an instrument in writing, not being a bank note or a currency note, containing an unconditional undertaking signed by the maker, to pay a certain sum money only to or to the order of certain person, or the bearer”.

Section 5 of the Negotiable Instruments Act, 1881 defines Bill of Exchange as: “A bill of exchanges is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay certain sum of money only to, or to the order of a certain person, or to the bearer of the instrument”.

Cancellation of bill on maturity in return of a new bill for an extended period of credit is known as renewal of bill of exchange.

Formulae [6]

Assets = Capital + Liabilities

\[\text{Rectifying Entry = Reverse Entry + Correct Entry}\]

- When an error is found in the books, the wrong effect must first be canceled (by making the opposite or reversal entry), and then the correct transaction must be recorded accurately.

- This ensures that both debit and credit sides of the accounts reflect the proper financial position.

\[\mathrm{Depreciation~(p.a.)~=~\frac{Original~cost~-~Scrap~Value}{Estimated~life~of~the~asset~(in~years)}}\]

Original cost of Asset = Purchasing price of an Asset + Incidental charges, etc.

\[\text{Depreciation (p.a.)}=\frac{\text{Cost of the Asset × Rate of depreciation}}{100}\]

Note: If the asset is used for only part of the year, charge depreciation in proportion to the time used.

\[\text{Depreciation}=\text{Book Value at beginning of year}\times\frac{\text{Rate of Depreciation}}{100}\]

Where:

-

Book Value = Cost – Accumulated Depreciation

-

Rate of Depreciation (%) = Fixed rate used each year

\[\text{Discount}=\text{Amount of Bill}\times\frac{\text{Rate}}{100}\times\frac{\text{Unexpried days}}{365}\]

Or

\[\text{Discount}=\text{Amount of Bill}\times\frac{\text{Rate}}{100}\times\frac{\text{Unexpried months}}{12}\]

Key Points

1. Books of Drawer (Creditor/Seller):

Cash/Bank A/c ...Dr.

Rebate / Discount A/c ...Dr.

To Bills Receivable A/c

(Being bill retired and rebate allowed)

2. Books of Drawee (Debtor / Buyer):

Bills Payable A/c ...Dr.

To Cash / Bank A/c

To Rebate / Discount A/c

(Being our acceptance retired and rebate received)

- A negotiable instrument includes a promissory note, bill of exchange, or cheque payable to order or bearer under the Negotiable Instruments Act, 1881.

- A promissory note is a written promise to pay a certain sum of money.

- The person who makes and signs the promissory note is called the Maker or Drawer.

- The Maker is also known as the promiser because he promises to pay the amount.

- The person in whose favour the promissory note is drawn is called the Drawee or Payee, and he is also known as the promisee.

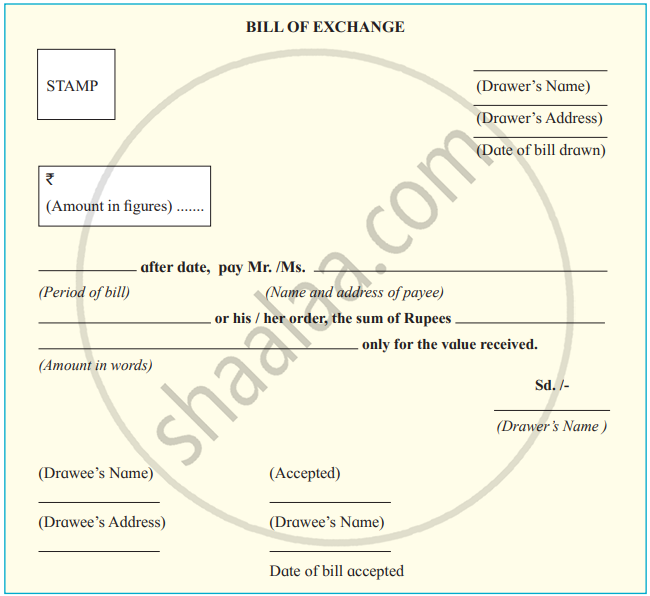

- Meaning: A Bill of Exchange is a written order by the creditor to the debtor to pay a fixed amount; it becomes valid after acceptance.

- Parties: Drawer (makes the bill), Drawee (pays the bill), Payee (receives the amount).

- Features: Must be written, signed, dated, stamped, and contain an unconditional order to pay.

- Types: Trade, Accommodation, Inland, Foreign, After Date, After Sight, and Demand Bills.

- Terms: Draft (before acceptance), Days of Grace (3 days extra), Holder (possessor), Holder in Due Course (gets it for value before maturity).

| Basis | Provision | Reserve |

|---|---|---|

| Nature | Liability or asset reduction | Shareholders' money |

| Purpose | For specific loss/expense | For specific or general use |

| Charge vs. Appropriation | Charged to profit | Appropriated from profit |

| Disclosure in Financial Statement | Shown as an expense in P&L | Shown under Shareholders' Funds |

| Disclosure in Balance Sheet | Under Provisions or asset deduction | Under 'Reserves & Surplus' |

| Investment Outside Business | Not allowed | Allowed (as fund) |

| Legal Requirement | Legally required | Based on prudence |

| Necessity | Mandatory even without profit | Created only if profits exist |

| Utilisation for Dividends | Not allowed | Allowed |

| Utilisation for Other Purposes | Only for the loss provided | Can be used for any purpose |

- Discounting a bill means getting money from the bank before the due date by giving the bill to the bank.

- The bank gives less than the bill amount (after deducting discount charges) and collects the full amount from the drawee on the due date.

- The main parties involved are Drawer (Seller), Drawee (Buyer), Holder/Payee, and the Bank.

- The process includes selling goods on credit, drawing and accepting the bill, and then discounting it with the bank.

- The discount is treated as an expense for the drawer and is recorded in the books of accounts.

A. Drawer discounts the bill with the bank:

1. Books of Drawer:

Bank A/c ...Dr.

Discount A/c ...Dr.

To Bills Receivable A/c

(Being Drawee’s acceptance discounted with the bank)

2. Books of Drawee: No entry

(Drawee is not a party to the transaction)

B. Discounted bill honoured on the due date:

1. Books of Drawer: No entry

(Cash already received at the time of discounting)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

C. Discounted bill dishonoured on the due date:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bank A/c

(Being a discounted bill dishonoured on the due date)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

D. Discounted bill dishonoured and noting charges paid by bank:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bank A/c

(Being a discounted bill dishonoured on the due date and Noting Charges paid by the bank)

[Amount = Bill amount + Noting Charges]

2. Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and Noting Charges payable)

- Endorsement means transferring the title of a bill by signing it on the back and handing it over to another person.

- The person who transfers the bill is called the Endorser, and the one who receives it is the Endorsee.

- Endorsement is usually done to settle a debt the drawer or holder owes to others.

- A bill of exchange is a negotiable instrument and can be endorsed multiple times before maturity.

- On the due date, the endorsee presents the bill to the drawee and receives the payment.

A. Drawer endorses the bill to Endorsee:

1. In the Books of Drawer/Endorser:

Endorsee’s A/c ...Dr.

To Bills Receivable A/c

(Being Drawee’s acceptance endorsed to our creditor)

2. In the Books of Drawee: No Entry

(Drawee is not a party to the endorsement transaction)

3. In the Books of Endorsee:

Bills Receivable A/c ...Dr.

To Endorser’s A/c

(Being Bills Receivable received from our debtor)

B. Endorsed bill honoured on the due date:

1. In the Books of Drawer / Endorser: No entry

(Drawer is not a party to the transaction)

2. In the Books of Drawee:

Bills Payable A/c Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

3. In the Books of Endorsee:

Cash / Bank A/c ...Dr.

To Bills Receivable A/c

(Being Bills Receivable received honoured)

C. Endorsed bill dishonoured on the due date:

1. In the Books of Drawer / Endorser:

Drawee’s A/c ...Dr.

To Endorsee’s A/c

(Being an endorsed bill dishonoured on the due date)

2. In the Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

3. In the Books of Endorsee:

Endorser’s A/c ...Dr.

To Bills Receivable A/c

(Being Bills Receivable dishonoured)

D. Endorsed bill dishonoured and noting charges paid by Endorsee:

1. In the Books of Drawer / Endorser:

Drawee’s A/c ...Dr.

To Endorsee’s A/c

(Being endorsed bill dishonoured and noting charges paid by Endorsee)

(Amount = Bill amount + Noting Charges)

2. In the Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and noting charges payable)

3. In the Books of Endorsee:

Endorser’s A/c ...Dr.

To Bills Receivable A/c

To Cash A/c

(Being Bills Receivable dishonoured and noting charges paid)

- The drawer can send the bill to the bank for collection instead of presenting it personally on the due date.

- The bank collects the amount from the drawee on the due date on behalf of the drawer.

- For this service, the bank charges a fee known as Bank Charges.

- A temporary account called “Bill Sent for Collection A/c” is opened by the drawer for this purpose.

- This account is closed when the bank collects the payment or if the bill is dishonoured.

A. Bill sent to the bank for collection:

1. Books of Drawer:

Bill Sent for Collection A/c ...Dr.

To Bills Receivable A/c

(Being bill sent to the bank for collection)

2. Books of Drawee: No entry

(Drawee is not a party to the transaction)

B. Bill sent to bank for collection honoured on the due date and bank charges debited by bank:

1. Books of Drawer:

Bank A/c ...Dr.

Bank Charges A/c ...Dr.

To Bill Sent for Collection A/c

(Being bill honoured and bank charges debited)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

C. Bill sent to bank for collection dishonoured on the due date:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bill Sent for Collection A/c

(Being bill sent for collection dishonoured)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

D. Bill sent to bank for collection dishonoured on due date and Noting Charges paid:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bill Sent for Collection A/c

To Bank A/c

(Being bill sent for collection dishonoured and noting charges paid)

2. Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and noting charges payable)

- Honouring of Bill: When the Drawee pays the bill amount on the due date, it is called honouring. The holder must present the bill on or before the due date, or the Drawee is not liable.

- Dishonouring of Bill: If the Drawee refuses or fails to pay, the bill is dishonoured. This can be due to non-acceptance or non-payment.

- Noting: It is the formal recording of dishonour by a Notary Public. It serves as proof that legal action is needed and should be done within a reasonable time.

- Protest: A written certificate issued by a Notary Public confirming the dishonour of a bill after noting. It is used as legal evidence.

- Noting Charges: Fees paid to the Notary Public for noting. Initially paid by the holder but finally borne by the Drawee.

A. Cancellation of Old Bill or Dishonour of Bill:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bills Receivable A/c or

To Bank A/c or

To Bill Sent for Collection A/c or

To Endorsee’s A/c

(Being old bill cancelled for renewal)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance cancelled for renewal)

B. Interest Due on Balance Amount:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Interest A/c

(Being interest due)

2. Books of Drawee:

Interest A/c ...Dr.

To Drawer’s A/c

(Being interest due)

C. Receiving / Paying Part Payment:

1. Books of Drawer:

Cash / Bank A/c Dr.

To Drawee’s A/c

(Being part payment received along with interest)

Note: Add interest amount if received

2. Books of Drawee:

Drawer’s A/c ...Dr.

To Cash / Bank A/c

(Being part payment made along with interest)

D. Drawing and Acceptance of New Bill:

1. Books of Drawer:

Bills Receivable A/c ...Dr.

To Drawee’s A/c

(Being a new bill drawn and accepted for the balance)

Note: Add interest amount if included

2. Books of Drawee:

Drawer’s A/c ...Dr.

To Bills Payable A/c

(Being new bill accepted for the balance)

When Interest Paid in Cash Immediately

A. Cancellation of Old Bill

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bills Receivable A/c or

To Bank A/c or

To Bill Sent for Collection A/c or

To Endorsee’s A/c

(Being old bill cancelled for renewal)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance cancelled for renewal)

B. Interest Paid in Cash Along with Part Payment:

1. Books of Drawer:

Cash / Bank A/c ...Dr.

To Drawee’s A/c

To Interest A/c

(Being part payment received with interest in cash)

2. Books of Drawee:

Drawee’s A/c ...Dr.

Interest A/c ...Dr.

To Cash / Bank A/c

(Being part payment made along with interest)

C. New Bill Drawn for Balance:

1. Books of Drawer:

Bills Receivable A/c ...Dr.

To Drawee’s A/c

(Being new bill drawn and acceptance received)

2. Books of Drawee:

Drawer’s A/c ...Dr.

To Bills Payable A/c

(Being acceptance given)

Concepts [49]

- Cash Memo

- Cheque

- Cash Book

- Cash Book > Simple Cash Book (Single Column Cash Book)

- Cash Book > Petty Cash Book

- Purchase Book

- Sales Book

- Purchase Return Book

- Sales Return Book

- Journal Proper

- Accounting Equation

- Debit,Credit and Golden Rules

- Origin of Transactions

- Voucher

- Books of Original Entry

- Understanding the Ledger

- Balancing of Ledger Accounts

- Posting

- Bank Reconciliation Statement(BRS)

- Preparation of BRS

- Calculating Bank Balance at an Accounting Date

- Corrected Cash Book Balanced

- Trial Balance

- Preparation of the Trial Balance by the Balance Method

- Errors in Accounting

- Types of Errors

- Suspense Account

- Detection and Rectification of Errors

- Concept of Depreciation

- Fixed Instalment Method

- Written Down Value Method

- Accounting Treatment under Fixed Instalment and Written Down Value Methods

- Accounting Treatment of Depreciation-By Creating Provision for Depreciation

- Accounting Treatment of Depreciation-Accumulated Depreciation Account

- Retirement of Bill under Rebate

- Accounting Treatment of Depreciation-Treatment of Disposal of Asset

- Promissory Note

- Provisions and Reserves

- Concept of Bills of Exchange

- Accounting Treatment> Discounting the Bill of Exchange

- Types of Reserves-Revenue Reserve

- Accounting Treatment> Endorsement of Bill of Exchanges

- Types of Reserves-Capital Reserve

- Accounting Treatment > Bills Sent to Bank for Collection

- Types of Reserves-General Reserve

- Honouring and Dishonouring of Bill of Exchange

- Types of Reserves-Specific Reserves

- Renewal Bill of Exchange

- Accounting Treatment of Bill Transactions