Definitions [9]

Subsidiary books are special accounting books used to record similar types of transactions in an organized and chronological manner before posting them to the ledger.

A Purchase Book (also called Bought Day Book or Purchase Journal) is used to record only credit purchases of goods intended for resale or production.

A debit note is a brief statement prepared by the buyer when returning goods, showing the details and amount of goods returned, and letting the supplier know to reduce the buyer’s amount owed.

A credit note is a document given by a seller to a buyer when goods are returned, showing the amount to reduce or cancel what the buyer has to pay; it acts like a “refund slip” that adjusts the buyer’s account and proves the return happened.

A purchase return book is a special accounting book where a business records goods sent back to suppliers because they are the wrong quality, damaged, or not needed—only returns from credit purchases are included.

A sales book is a special accounting record used to write down all the credit sales of goods made by a business, while cash sales or sales of assets are recorded elsewhere.

The Sales Return Book is a special accounting book used to record goods that were sold to customers on credit but are returned to the business because they are not as ordered, damaged, or defective.

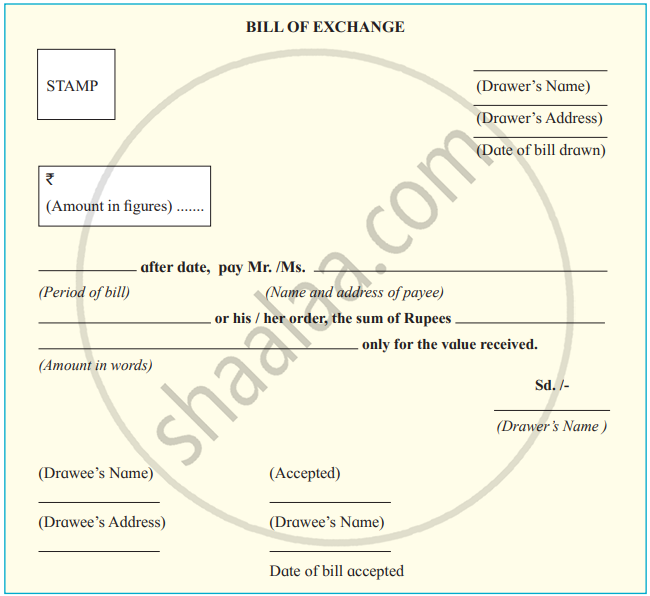

Section 5 of the Negotiable Instruments Act, 1881 defines Bill of Exchange as: “A bill of exchanges is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay certain sum of money only to, or to the order of a certain person, or to the bearer of the instrument”.

Journal Proper is a special accounting book where rare or miscellaneous transactions, not recorded in other subsidiary books, are entered.

Key Points

- Meaning: A Bill of Exchange is a written order by the creditor to the debtor to pay a fixed amount; it becomes valid after acceptance.

- Parties: Drawer (makes the bill), Drawee (pays the bill), Payee (receives the amount).

- Features: Must be written, signed, dated, stamped, and contain an unconditional order to pay.

- Types: Trade, Accommodation, Inland, Foreign, After Date, After Sight, and Demand Bills.

- Terms: Draft (before acceptance), Days of Grace (3 days extra), Holder (possessor), Holder in Due Course (gets it for value before maturity).