Definitions [4]

Define Labour.

- Labour is the active factor of production.

- In common parlance, labour means manual labour or unskilled work. But in Economics the term ‘labour’ has a wider meaning.

- It refers to any work undertaken for securing an income or reward. Such work may be manual or intellectual. For example, the work done by an agricultural worker or a cook or rickshaw puller or a mason is manual.

- The work of a doctor or teacher or engineer is intellectual.

- In short, labour in economics refers to any type of work performed by a labourer for earning an income.

Define production function.

A production function indicates the highest amount of a product that can be made in a specific time frame using a set amount of inputs, utilising the best available production method.

A production function shows the maximum quantity of a commodity that can be produced per unit of time with the given amount of inputs when the best production technique available is used. A production function can be expressed in the form of a table, graph or algebraic equation. In the form of an algebraic equation, the production function for a good may be expressed as:

QX = f(F1, F2...Fn) Where OX is the quantity of output of the commodity X: and F1, F2 ... Fn are the quantities of different inputs used to produce the commodity X.

- “As the proportion of the factor in a combination of factors is increased after a point, first the marginal and then the average product of that factor will diminish.”

—Benham - “The law of variable proportion states that if the inputs of one resource is increased by equal increment per unit of time while the inputs of other resources are held constant, total output will increase, but beyond some point the resulting output increases will become smaller and smaller.”

—Leftwich - “An increase in some inputs relative to other fixed inputs will, in a given state of technology, cause output to increase; but after a point the extra output resulting from the same additions of extra inputs will become less and less.”

—Samuelson

"The law of supply states that the higher the price, the greater the quantity supplied or the lower the price, the smaller the quantity supplied." – Dooley

Formulae [1]

A production function can be shown as:

- A table (showing different combinations of inputs and output),

- A graph, or

- An equation (algebraic form).

General form:

\[Q_x=f(f_1,f_2,\ldots,f_n)\]

Where:

- Qx = quantity of output of commodity X,

- f1, f2,…, fn = quantities of different factor inputs,

- Qx is the dependent variable (depends on inputs) ,

- f1, f2,…, fn are independent variables.

If we assume only two inputs: labour (L) and capital (K):

\[Q_x=f(L,K)\]

Theorems and Laws [5]

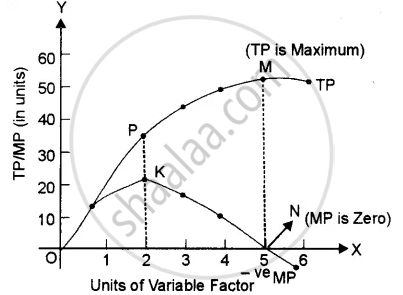

Explain the law of variable proportions with the help of a diagram.

The law of variable proportions (LVP) states that as we increase the quantity of only one input, keeping other inputs fixed, total product (TP) initially increases at an increasing rate, then at a decreasing rate and finally at a negative rate.

In the given diagram, the quantity of the variable factor has been measured on X-axis and the Y-axis measures the total product on the Y-axis. The diagram indicates how the total product and marginal product change as a result of increases in the quantity of one factor to a fixed quantity of other factors.

The law can be better explained through three stages:

- First stage:

- Increasing return to a factor: In the first stage, every additional variable factor adds more and more to the total output. It means TP increases at an increasing rate and the MP of each variable factor rises. Better utilisation of fixed factors and increases in the efficiency of a variable factor due to specialisation are the major factors responsible for increasing returns. The increasing returns to a factor stage have been shown in the given diagram between O to P. It implies. TP increases at an increasing rate (till point ‘P’) and MP rises till it reaches its maximum point ‘K,’ which marks the end of the first phase.

- Increasing return to a factor: In the first stage, every additional variable factor adds more and more to the total output. It means TP increases at an increasing rate and the MP of each variable factor rises. Better utilisation of fixed factors and increases in the efficiency of a variable factor due to specialisation are the major factors responsible for increasing returns. The increasing returns to a factor stage have been shown in the given diagram between O to P. It implies. TP increases at an increasing rate (till point ‘P’) and MP rises till it reaches its maximum point ‘K,’ which marks the end of the first phase.

- Second stage:

- Diminishing returns to a Factor: In the second stage, every additional variable factor adds a lesser and lesser amount of output. It means TP increases at a diminishing rate and MP falls with an increase in a variable factor. The breaking of the optimum combination of a fixed and variable factor is the major factor responsible for diminishing returns. The second stage ends at point ‘S’ when MP is zero and TP is maximum (point ‘M’).

Stage 2 is very crucial, as a rational producer will always aim to produce in this phase because TP is maximum and MP of each variable factor is positive.

- Diminishing returns to a Factor: In the second stage, every additional variable factor adds a lesser and lesser amount of output. It means TP increases at a diminishing rate and MP falls with an increase in a variable factor. The breaking of the optimum combination of a fixed and variable factor is the major factor responsible for diminishing returns. The second stage ends at point ‘S’ when MP is zero and TP is maximum (point ‘M’).

- Third stage:

- Negative Returns to a Factor: In the third stage the employment of additional variable factors causes TP to decline. MP now becomes negative. Therefore, this stage is known as negative returns to a factor. Poor coordination between variable and fixed factors is the basic cause for this stage. In the fig., the third stage starts after point ‘N’ on the MP curve and point ‘O’ on the TP curve. The MP of each variable factor is negative in the 3 stages. So, no firm would deliberately choose to operate in this stage.

- If you keep increasing the variable input (e.g., labour) for a fixed input (e.g., land), the total production goes up at first, then grows slowly, and finally can go down.

- Marginal product (extra output from one more unit) and average product (output per unit) also rise at first, but later start to fall.

State the law of supply.

The law of supply states that other factors being equal, the quantity of a good supplied increases with an increase in the price level and decreases with a decrease in the price level of a good.

Law of supply states the direct relationship between price and quantity supplied, keeping other factors constant.

The law of supply states that other factors being equal, the quantity of a good supplied increases with an increase in the price level and decreases with a decrease in the price level of a good.

The supply schedule below shows the positive relationship between price and quantity supplied.

| Price (in Rs) | Quantity Supplied |

| 5 | 100 |

| 10 | 200 |

| 15 | 300 |

SS is the supply curve sloping upwards. When the price increases from Rs. 5 to Rs. 15, the quantity supplied also increases from 100 units to 300 units.

Explain the law of supply.

The law of supply shows a direct relationship between the price of a good and the quantity supplied. As the price rises, the quantity supplied also increases. This scenario is represented by an upward-sloping supply curve. This happens mainly due to two reasons:

- Profit Motivation: When the price of a product goes up, the chance of earning more profit also increases (assuming other factors remain the same). This encourages producers to supply more of that product.

- Rising Production Costs: As production increases, the cost of making each additional unit (marginal cost) also rises. So, producers are willing to produce and supply more only if the price is high enough to cover these extra costs.

“Other things being constant, the higher the price of a commodity, more is the quantity supplied; and lower the price of a commodity, less is the quantity supplied.”

In simple words: When the price rises, supply rises; when the price falls, supply falls.

There is a direct relationship between price and quantity supplied.

Symbolically:

Sx = f (Px)

Where:

- S = Supply

- x = Commodity

- f = Function

- P = Price of the commodity

Key Points

- A production function shows the technical relationship between physical inputs and maximum possible output in a given time.

- Short run: At least one factor is fixed; the firm changes output by changing only variable factors.

- Long run: All factors are variable; the firm can change the scale of production and plant size.

- Short‑run production function Q = f (L) → study of returns to a factor and Law of Variable Proportions.

- Long‑run production function → study of returns to scale.

- Only one input is changed; others are fixed.

- First, output improves quickly.

- Later, output slows down and may decrease.

- Businesses use this law to find the best input mix.

- Economies of scale help firms reduce average costs as production increases.

- Internal economies include technical, marketing, labour, managerial, and transport/storage economies plus pecuniary savings.

- External economies come from industry growth and infrastructure shared by all firms.

- Understanding these helps firms and policymakers improve production efficiency.

- Diseconomies of scale increase costs when a firm grows too big.

- Internal diseconomies arise from management, technical, production, marketing, and financial issues.

- External diseconomies come from pollution, infrastructure overload, and resource competition.

- Understanding these helps firms stay efficient and avoid costly expansion.

- Producer’s equilibrium is the output level where the producer earns maximum profit and has no incentive to change output.

- Under the TR–TC approach, equilibrium occurs at the output where the vertical gap between TR and TC is greatest.

- Under the MR–MC approach, equilibrium occurs where MR = MC and MC is rising; MR > MC implies “increase output”, while MR < MC implies “decrease output”.

- Law of supply: The Higher the price, higher the supply; lower price, lower supply (if all else stays the same).

- Exceptions: rare items, short periods, perishable goods, some labor markets.

- Supply is always shown using a schedule (table) and a curve (graph).

- Supply schedule shows price and quantity supplied in tabular form

- Assumes other factors constant

- Types: Individual and Market

- Individual supply schedule shows supply of one producer

- Market supply schedule shows total supply of all producers

- Market supply = sum of individual supplies

- Law of supply: Higher price → higher quantity supplied

- Supply curve is graphical form of supply schedule

- Price on Y-axis, quantity on X-axis

- Supply curve slopes upward

- Types: Individual supply curve and Market supply curve