Definitions [7]

Define the following concept:

Cross Elasticity of Demand

Cross elasticity of demand is the measure of the responsiveness of demand for a good to a change in the price of a related good.

`"Ec" = ("Proportionate change in quantity demanded of good X")/("Proportionate change in price of good Y")`

Define elasticity of demand.

Price elasticity of demand tells us the amount of the change in the quantity demanded of a commodity in response to change in its price. In other words, it measures the degree of change of demand in response to changes in price.

Define price elasticity of demand.

It is the measure of the degree of responsiveness of the demand for a good to the changes in its price. It is defined as the percentage change in the demand for a good divided by the percentage change in its price.

ed = `"Percentage change in demand for good"/"Percentage change in price of that good"`

ed = `(ΔQ)/(ΔP) xx P/Q`

Where ΔQ = Q2 − Q1, change in demand

ΔP = P2 − P1, change in price

P1 = Initial price

Q1 = Initial quantity

- "Elasticity of demand may be defined as the percentage change in quantity demanded to the percentage change in price." - Alfred Marshall

- "The elasticity of demand for a commodity is the rate at which quantity bought changes as the price changes." - A.K. Cairncross

- "Elasticity of demand is a technical term used by the economists to describe the degree of respensiveness of demand of a commodity to a change in its price." -Stonier and Hague

- Elasticity of demand refers to the degree of responsiveness of quantity demanded of a commodity to a change in any of its determinants.

Define perfectly elastic demand.

Perfectly elastic demand means that quantity demanded will increase to infinity when the price decreases and quantity demanded will fall to zero when price increases.

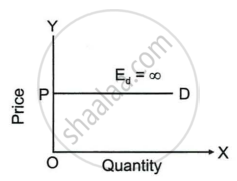

With the help of a diagram define perfectly elastic demand.

The demand curve runs parallel to the x-axis. A little change in price results in an indefinitely huge change in the quantity needed. The demand curve represents completely elastic demand for the commodity.

- "Income elasticity of demand means the ratio of the percentage change in the quantity demanded to the percentage change in income." - Watson

- "The responsiveness of demand to change in income is termed as income elasticity of demand." - R.G. Lipsey

Formulae [1]

Ey = `"Proportionate change in Quantity Demanded"/"Proportionate change in income"`

\[E_y=\frac{\frac{\Delta Q}{Q}}{\frac{\Delta Y}{Y}}\quad=\frac{\Delta Q}{Q}\div\frac{\Delta Y}{Y}=\frac{\Delta Q}{Q}\times\frac{Y}{\Delta Y}\]

Where:

Ey = Income elasticity of demand

ΔQ = Change in the quantity demanded

Q = Initial demand

ΔY = Change in income

Y = Initial Income

Key Points

- Law of demand only shows direction (more or less), elasticity shows the degree (how much more or less).

- Some things (necessities) have inelastic demand; luxuries or goods with many substitutes have elastic demand.

- Alfred Marshall introduced this concept and the popular measurement formula.

- Total Expenditure Formula:

Total Expenditure (TE) = Price (P) × Quantity Demanded (Q) - Revenue Method Formula:

Ed = AR / (AR - MR)

or

Ed = Average Revenue / (Average Revenue - Marginal Revenue) - Arc Elasticity Demand Formula:

\[\mathrm{E=\frac{Q_{2}-Q_{1}}{Q_{2}+Q_{1}}\div\frac{P_{1}-P_{2}}{P_{1}+P_{2}}}\] - Proportionate Method Formula:

\[\mathrm{Ed}=\frac{\text{Percentage change in Quantity demanded}}{\text{Percentage change in Price}}\]

\[\mathrm{Ed}=\frac{\%\triangle\mathrm{Q}}{\%\triangle\mathrm{P}}\]

- YED shows how demand changes with income.

- Luxury goods: YED > 1 → demand grows faster than income.

- Necessities: 0 < YED < 1 → demand grows slower than income.

- Essential goods: YED = 0 → demand stays the same.

- Inferior goods: YED < 0 → demand drops as income rises.

Important Questions [11]

- Explain the factors determining the elasticity of demand.

- Discuss any four factors affecting price elasticity of demand.

- What is the elasticity of demand?

- Define the following concept: Cross Elasticity of Demand

- Mention any two examples of composite demand.

- The elasticity of demand for school bag will be ______.

- Draw a diagram showing a perfectly elastic demand curve.

- With the help of a graph explain the relatively inelastic demand for a commodity.

- Analyse the given graphs and identify the type of elasticity of demand of: Picture 1 Picture 2

- State whether demand will be Elastic or Inelastic. Give reasons for your answer. The demand for salt by households.

- State whether demand will be Elastic or Inelastic. Give reasons for your answer. A consumer prefers to postpone the purchase of a car to avail more of year ending discount.