Advertisements

Advertisements

प्रश्न

X Ltd. has applied for a short-term loan of ₹10 Lac from State Bank of India. The bank manager, while making a decision about granting the loan, wants to have an idea about the Sources and Utilisation of Cash. You are required to submit a project report to the bank manager, which would enable him to decide about granting the loan. Following particulars are related to X Ltd.

| BALANCE SHEET as at 31st March, 2023 | |||||

| Particulars | Note No. |

March 31, 2023 (₹’000) |

March 31, 2022 (₹’000) |

||

| I. | Equity & Liabilities: | ||||

| (1) | Shareholder’s Funds | ||||

| Share Capital | 2,500 | 2,000 | |||

| Reserves and Surplus | 1,800 | 1,200 | |||

| (2) | Non-Current Liabilities | ||||

| Long-term Borrowings | 1,200 | 1,000 | |||

| (3) | Current Liabilities | ||||

| Short-term Borrowings | 1 | 250 | - | ||

| Trade Payables | 1,860 | 1,800 | |||

| Short-term Provision | 2 | 240 | 200 | ||

| 7,850 | 6,200 | ||||

| II. | Assets: | ||||

| (1) | Non Current Assets | ||||

| (a) Property, Plant and Equipment and Intangible Assets | |||||

| (i) Property, Plant and Equipment (Machinery) | 3 | 4,300 | 2,900 | ||

| (b) Non-Current Investments | 300 | 200 | |||

| (2) | Current Assets | ||||

| Short-term Investments (Marketable) | 120 | 250 | |||

| Inventories | 1,000 | 500 | |||

| Trade Receivables | 1,500 | 1,400 | |||

| Cash & Bank Balance | 630 | 850 | |||

| Other Current Assets | 4 | - | 100 | ||

| 7,850 | 6,200 | ||||

Note:

| 31-3-2023 (₹’000) |

31-3-2022 (₹’000) |

||

| 1. | Short-term Borrowings: | ||

| Bank Overdraft | 250 | - | |

| 2. | Short-term Provision: | ||

| Provision for Tax | 240 | 200 | |

| 3. | Machinery: | 6,200 | 4,500 |

| Less: Accumulated Depreciation | 1,900 | 1,600 | |

| 4,300 | 2,900 | ||

| 4. | Other Current Assets: | ||

| Payment in Advance | - | 100 | |

Additional Information:

- Provision for Tax made during the year 2022-23 amounted to ₹2,25,000.

- An interim dividend of ₹2,00,000 was paid during the year.

- Machinery costing ₹8,00,000 (accumulated depreciation thereon being 1,80,000) were sold during the year at a loss ₹1,20,000.

- Interest received on Investments amounted to ₹30,000.

- Interest on long-term borrowings paid during the year amounted to ₹1,20,000.

Advertisements

उत्तर

Introduction of the Project:

The project work is to submit a report to the bank manager, which should enable him to arrive at a decision regarding granting a short-term loan of ₹10 Lac. to X Ltd.

Necessary data, as well as additional information, is provided in the form of Balance Sheets as of 31st March, 2022 and 2023. The data provided is used for the purpose of the project work.

Since X Ltd. has applied for a short-term loan, the bank manager will require information regarding the company’s short-term financial position. He will also require information regarding the sources and utilisation of cash during the period to assess the ability of the enterprise to generate future cash flows.

Hence, the project work is planned and executed by preparing a Cash Flow Statement.

| CASH FLOW STATEMENT | ||||

| for the year ended 31st March, 2023 | ||||

| Particulars | Amount (₹’000) |

Amount (₹’000) |

Amount (₹’000) |

|

| A. | Cash flows from Operating Activities: | |||

| Net Profit before Tax (Note 1) | 1,025 | |||

| Adjustments For Non-Cash and Non-Operating Items: | ||||

| Add: Depreciation(4) | 480 | |||

| Loss on Sale of Machinery | 120 | |||

| Interest on Long-term Borrowings | 120 | |||

| Interest on Non-Current Investments | (30) | |||

| Operating Profit before Working Capital Changes | 1,715 | |||

| Add: Increase in Trade Payables | 60 | |||

| Decrease in Payment in Advance | 100 | 160 | ||

| 1,875 | ||||

| Less: Increase in Inventories | 500 | |||

| Increase in Trade Receivables | 100 | 600 | ||

| 1,275 | ||||

| Payment of Tax(2) | (185) | |||

| Net cash from operating activities | 1,090 | 1,090 | ||

| B. | Cash flows from Investing Activities: | |||

| Sales of Machinery | 500 | |||

| Purchase of Machinery(3) | (2,500) | |||

| Purchase of Non-Current Investments | (100) | |||

| Interest received | 30 | |||

| Net cash used in investing activities | (2,070) | (2,070) | ||

| C. | Cash flows from Financing Activities: | |||

| Proceeds from the issue of share capital | 500 | |||

| Proceeds from Long-term Borrowings | 200 | |||

| Proceeds from Short-term Borrowings (Increase in Bank Overdraft) |

250 | |||

| Interest paid | (120) | |||

| Interim Dividend Paid | (200) | |||

| Net cash from financing activities | 630 | 630 | ||

| Net decrease in cash and cash equivalents | (350) | |||

| Add: Cash and cash equivalents at the beginning of the period(5) | 1,100 | |||

| Cash and cash equivalents at the end of the period | 750 | |||

Notes:

(1)

| Amount (₹’000) |

|

| Calculation of Net Profit before Tax: | |

| Reserve and Surplus Balance on 31st March 2023 | 1,800 |

| Less: Reserve and Surplus Balance on 31st March, 2022 | 1,200 |

| 600 | |

| Add: Current year’s Provision for Tax | 225 |

| Interim Dividend | 200 |

| 1,025 |

(2)

| PROVISION FOR TAX ACCOUNT | |||

| Particulars | Amount (₹’000) |

Particulars | Amount (₹’000) |

| To Bank A/c (balancing figure, being Payment of Tax) | 185 | By Balance b/d | 200 |

| To Balance c/d | 240 | By Statement of P & L (Provision made during Current Year) | 225 |

| 425 | 425 | ||

(3)

| MACHINERY ACCOUNT | |||

| Particulars | Amount (₹’000) |

Particulars | Amount (₹’000) |

| To Balance b/d | 4,500 | By Bank A/c (Sale) | 500 |

| To Bank A/c (Balancing figure, being purchased) | 2,500 | By Accumulated Depreciation A/c | 180 |

| By Loss on Sale of Machinery A/c | 120 | ||

| By Balance c/d | 6,200 | ||

| 7,000 | 7,000 | ||

(4)

| ACCUMULATED DEPRECIATION ACCOUNT | |||

| Particulars | Amount (₹’000) |

Particulars | Amount (₹’000) |

| To Machinery A/c (Accumulated depreciation of Machinery sold) | 180 | By Balance b/d | 1,600 |

| To Balance c/d | 1,900 | By Depreciation A/c (balancing figure, being the current year’s depreciation) | 480 |

| 2,080 | 2,080 | ||

(5)

| Amount (₹’000) |

Amount (₹’000) |

|

| Cash and Cash Equivalents: | ||

| Marketable Securities | 120 | 250 |

| Cash & Bank Balances | 630 | 850 |

| 750 | 1,100 |

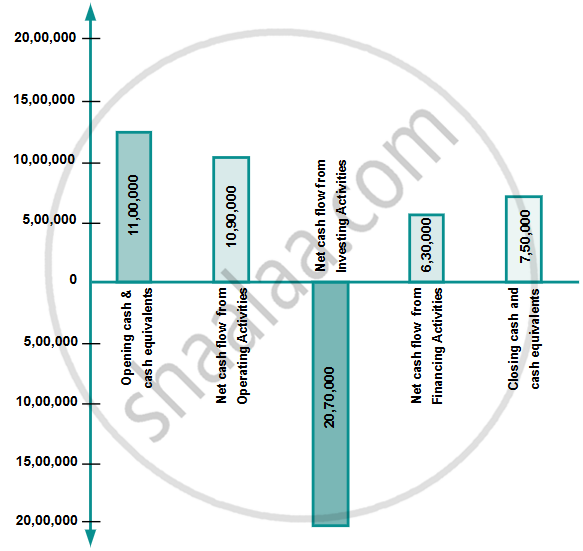

Comments: Cash outflow due to Investing activities is ₹20,70,000, whereas cash inflow from operating and financing activities is only ₹10,90,000 and ₹6,30,000, respectively. As a result, there is a net cash outflow of ₹3,50,000. Fixed Assets should have been purchased from long-term sources.

PRESENTATION OF INFORMATION:

CASH FLOWS ACTIVITIES IN X LTD.