Advertisements

Advertisements

प्रश्न

The board of Directors of Suvidha Appliances Ltd. was not able to comprehend why the bank overdraft of ₹5,00,000 has arisen inspite of continuous increase in profits over the last three years. Following information is obtained from the books of the company:

| BALANCE SHEET as at 31st March, 2023 | |||||

| Particulars | Note No. |

2023 (₹’000) |

2022 (₹’000) |

||

| I. | Equity & Liabilities: | ||||

| (1) | Shareholder’s Funds | ||||

| Share Capital | 2,500 | 2,500 | |||

| Reserves and Surplus | 3,400 | 3,000 | |||

| (2) | Non-Current Liabilities | ||||

| Long-term Borrowings | 1 | 400 | - | ||

| (3) | Current Liabilities | ||||

| Short-term Borrowings | 2 | 500 | - | ||

| Trade Payables | 1,120 | 980 | |||

| Short-term Provision | 3 | 180 | 120 | ||

| 8,100 | 6,600 | ||||

| II. | Assets: | ||||

| (1) | Non Current Assets | ||||

| (a) Property, Plant and Equipment and Intangible Assets | |||||

| (i) Property, Plant and Equipment | 4 | 5,000 | 4,700 | ||

| (ii) Intangible Assets | 5 | 160 | 200 | ||

| (2) | Current Assets | ||||

| Inventory | 1,680 | 800 | |||

| Trade Receivables | 1,200 | 500 | |||

| Cash Balance | 52 | 390 | |||

| Other Current Assets | 6 | 8 | 10 | ||

| 8,100 | 6,600 | ||||

Notes to Accounts:

| 2023 (₹’000) |

2022 (₹’000) |

||

| 1. | Long-term Borrowings: | ||

| Mortgage Loan | 400 | - | |

| 2. | Short-term Borrowings: | ||

| Bank Overdraft | 500 | - | |

| 3. | Short-term Provision: | ||

| Provision for Tax | 180 | 120 | |

| 4. | Property, Plant and Equipment: | ||

| Plant & Machinery less depreciation | 5,000 | 4,700 | |

| 5. | Intangible Assets: | ||

| Goodwill | 160 | 200 | |

| 6. | Other Current Assets: | ||

| Repayment | 8 | 10 | |

Additional Information:

- Plant & Machinery costing ₹5,00,000 was sold during the year at a loss of ₹2,30,000.

- Depreciation charged on plant & machinery during the year was ₹4,20,000.

- Tax paid during the year amounted to ₹1,40,000.

- Mortgage loan was taken on 1st July, 2022, @ 15% p.a. Up to date, interest has been paid on the loan.

- Interim Dividend @ 8% on share capital was paid during the year.

You are required to prepare a statement for the Board of Directors to show how the overdraft has arisen. Also, give your suggestions to extinguish the overdraft and provide funds for expansion.

Advertisements

उत्तर

Introduction of the Project:

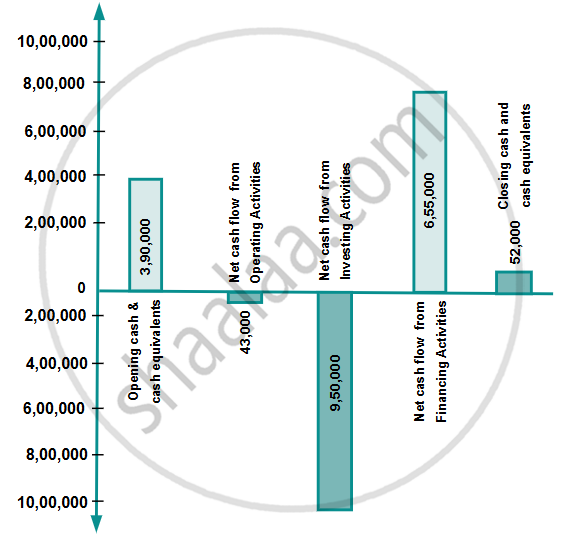

The project work is to ascertain how the company has an overdraft balance of ₹5,00,000 as at March 31, 2023, and a decrease in Cash balance from ₹3,90,000 on April 1, 2022, to only ₹52,000 on March 31, 2023.

Necessary data in the form of Balance Sheets as of 31st March, 2023 and 2022, is provided and used for the purpose of the project work.

The project work is planned and executed by preparing a cash flow statement to find out the causes of the decrease in cash balance and the evolution of bank overdraft:

| CASH FLOW STATEMENT | ||||

| for the year ended 31st March, 2023 | ||||

| Particulars | Amount (₹’000) |

Amount (₹’000) |

Amount (₹’000) |

|

| A. | Cash flows from Operating Activities: | |||

| Net Profit before Tax (Note 1) | 800 | |||

| Adjustments For Non-Cash and Non-Operating Items: | ||||

| Add: Depreciation | 420 | |||

| Add: Loss on Sale of Plant & Machinery | 230 | |||

| Add: Interest on Mortgage Loan | 45 | |||

| Add: Goodwill Written Off | 40 | 735 | ||

| Operating Profit before Working Capital Changes | 1,535 | |||

| Add: Decrease in Prepayments | 2 | |||

| Add: Increase in Trade Payables | 140 | 142 | ||

| 1,677 | ||||

| Less: Increase in Inventory | 880 | |||

| Less: Increase in Trade Receivables | 700 | 1,580 | ||

| 97 | ||||

| Payment of Tax | (140) | |||

| Net cash used in operating activities | (43) | (43) | ||

| B. | Cash flows from Investing Activities: | |||

| Sale of Plant & Machinery | 270 | |||

| Purchase of Plant & Machinery(3) | (1,220) | |||

| Net cash used in investing activities | (950) | (950) | ||

| C. | Cash flows from Financing Activities: | |||

| Raising of Mortgage Loan | 400 | |||

| Raising of Bank overdraft | 500 | |||

| Interim Dividend | (200) | |||

| Interest on Mortgage Loan | (45) | |||

| Net cash from financing activities | 655 | 655 | ||

| Net decrease in cash equivalents | (338) | |||

| Add: Cash and cash equivalents at the beginning of the period | 390 | |||

| Add: Cash and cash equivalents at the end of the period | 52 | |||

Note:

(1)

| CALCULATION OF NET PROFIT BEFORE TAX |

|

| Amount (₹’000) |

|

| Reserve and Surplus on 31st March, 2023 | 3,400 |

| Less: Reserve and Surplus on 31st March, 2022 | 3,000 |

| 400 | |

| Add: Provision for Tax(2) | 200 |

| Add: Interim Dividend | 200 |

| 800 | |

(2)

| PROVISION FOR TAX ACCOUNT | |||

| Particulars | Amount (₹’000) |

Particulars | Amount (₹’000) |

| To Bank A/c | 140 | By Balance b/d | 120 |

| To Balance c/d | 180 | By Statement of P & L (Balancing figure, provision made during the year) |

200 |

| 320 | 320 | ||

(3)

| PLANT & MACHINERY ACCOUNT | |||

| Particulars | Amount (₹’000) |

Particulars | Amount (₹’000) |

| To Balance b/d | 4,700 | By Bank A/c | 270 |

| To Bank A/c (Balancing figure, being purchase) | 1,220 | By Loss on Sale of Plant & Machinery A/c | 230 |

| By Depreciation A/c | 420 | ||

| By Balance c/d | 5,000 | ||

| 5,920 | 5,920 | ||

PRESENTATION OF INFORMATION:

Causes of a decrease in cash and an increase in bank overdraft:

Cash flow statement reveals that the leading causes of the decrease in cash balance and increase in bank overdraft are as follows:

- Purchase of Plant & Machinery: Plant & Machinery has been purchased for ₹12,20,000. For this purpose ₹4,00,000 has been raised through mortgage loan and the balance has been paid from current sources.

- Increase in Inventory: Inventory has increased by ₹8,80,000. It indicates that quite a lot of funds are blocked in inventory, causing a shortage of cash resources.

- Increase in Trade Receivables: Trade Receivables have increased by ₹7,00,000. Excessive funds blocked in Trade Receivables cause a shortage of cash resources.

Suggestions:

- The company should take immediate steps to reduce the inventory level.

- The company should improve its credit collection service. The business should also look over its credit sales strategy. Before lending money to a customer, it’s important to make sure they can pay it back.

- Since long-term debts comprise a very small amount of shareholders’ funds, the corporation may grow long-term borrowing to increase its cash reserves.