Advertisements

Advertisements

प्रश्न

Explain price determination under Perfect Competition.

Explain the determination of price of a commodity under perfect competition.

Advertisements

उत्तर १

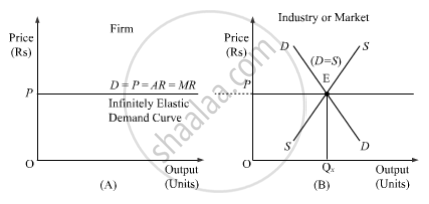

Under perfect competition, the market price, or the equilibrium price, is determined in the industry. Individual firms have no influence on this price. In the industry, the price is determined by the intersection of the market supply and market demand curves. In other words, the price under perfect competition is set at the point where the market supply of the good is equal to the market demand for the good. The individual firms take the market price so determined as fixed and adjust their supply accordingly.

In the figure, part A depicts the infinitely elastic demand curve faced by an individual firm in a perfectly competitive market. Part B depicts how the market demand and market supply curves interact to determine the market price. The market price OP is determined by the intersection of the market (industry) demand curve DD and the market (industry) supply curve SS. The market equilibrium is at point E, where OQx (amount of output) is supplied at the equilibrium market price OP. The price for the commodity is given to an individual firm, and no single firm can influence the market price. The firm faces an infinitely elastic demand curve, which suggests that no matter how many units of output are supplied, the price will remain the same. Hence, we can conclude that under a perfect competition market, an individual firm is a price taker and not a price maker.

उत्तर २

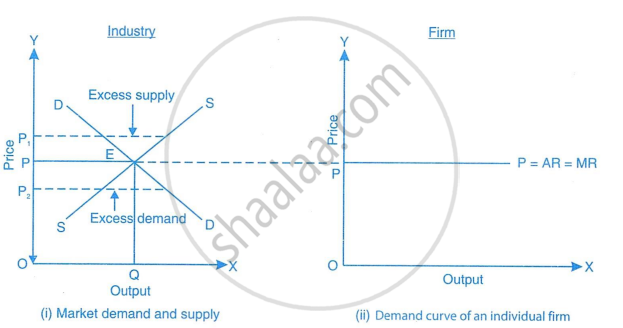

Under perfect competition, no individual firm or consumer can affect the market price due to their small share in total supply or demand. Instead, the price is set by the overall interaction of all firms (through the supply curve) and all consumers (through the demand curve) in the industry.

The short-run equilibrium price and quantity are determined at the point where the market demand curve and industry supply curve intersect. At this point, called equilibrium (E), total demand equals total supply. The corresponding price is OP and the quantity is OQ.

If the price goes above OP (like OP1), there is excess supply, so the price falls. If the price is below OP (like OP2), there is excess demand, so the price rises. At point E, there’s no shortage or surplus, so the price remains stable.