Definitions [3]

Section 5 of the Negotiable Instruments Act, 1881 defines Bill of Exchange as: “A bill of exchanges is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay certain sum of money only to, or to the order of a certain person, or to the bearer of the instrument”.

A person whose liabilities are more than the assets and is not in a position to pay off his liabilities is known as insolvent person.

Making payment of bill well before the date of maturity is known as retirement of bill.

Formulae [1]

\[\text{Discount}=\text{Amount of Bill}\times\frac{\text{Rate}}{100}\times\frac{\text{Unexpried days}}{365}\]

Or

\[\text{Discount}=\text{Amount of Bill}\times\frac{\text{Rate}}{100}\times\frac{\text{Unexpried months}}{12}\]

Key Points

- A draft becomes a valid Bill of Exchange only after the Drawee accepts it by signing with the word “Accepted” and the date.

- Acceptance is necessary to make the Drawee legally responsible for payment of the bill.

- General Acceptance means the Drawee accepts the bill without any conditions or changes.

- Qualified Acceptance means the Drawee accepts the bill with changes or conditions to the original terms.

- Types of Qualified Acceptance include changes to time, place, amount, parties, or added conditions for payment.

- Meaning: A Bill of Exchange is a written order by the creditor to the debtor to pay a fixed amount; it becomes valid after acceptance.

- Parties: Drawer (makes the bill), Drawee (pays the bill), Payee (receives the amount).

- Features: Must be written, signed, dated, stamped, and contain an unconditional order to pay.

- Types: Trade, Accommodation, Inland, Foreign, After Date, After Sight, and Demand Bills.

- Terms: Draft (before acceptance), Days of Grace (3 days extra), Holder (possessor), Holder in Due Course (gets it for value before maturity).

- Honouring of Bill: When the Drawee pays the bill amount on the due date, it is called honouring. The holder must present the bill on or before the due date, or the Drawee is not liable.

- Dishonouring of Bill: If the Drawee refuses or fails to pay, the bill is dishonoured. This can be due to non-acceptance or non-payment.

- Noting: It is the formal recording of dishonour by a Notary Public. It serves as proof that legal action is needed and should be done within a reasonable time.

- Protest: A written certificate issued by a Notary Public confirming the dishonour of a bill after noting. It is used as legal evidence.

- Noting Charges: Fees paid to the Notary Public for noting. Initially paid by the holder but finally borne by the Drawee.

- Discounting a bill means getting money from the bank before the due date by giving the bill to the bank.

- The bank gives less than the bill amount (after deducting discount charges) and collects the full amount from the drawee on the due date.

- The main parties involved are Drawer (Seller), Drawee (Buyer), Holder/Payee, and the Bank.

- The process includes selling goods on credit, drawing and accepting the bill, and then discounting it with the bank.

- The discount is treated as an expense for the drawer and is recorded in the books of accounts.

A. Drawer discounts the bill with the bank:

1. Books of Drawer:

Bank A/c ...Dr.

Discount A/c ...Dr.

To Bills Receivable A/c

(Being Drawee’s acceptance discounted with the bank)

2. Books of Drawee: No entry

(Drawee is not a party to the transaction)

B. Discounted bill honoured on the due date:

1. Books of Drawer: No entry

(Cash already received at the time of discounting)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

C. Discounted bill dishonoured on the due date:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bank A/c

(Being a discounted bill dishonoured on the due date)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

D. Discounted bill dishonoured and noting charges paid by bank:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bank A/c

(Being a discounted bill dishonoured on the due date and Noting Charges paid by the bank)

[Amount = Bill amount + Noting Charges]

2. Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and Noting Charges payable)

- The drawer can hold the bill until the due date instead of endorsing or discounting it.

- On the due date, the drawer (or holder) presents the bill to the drawee for payment.

- The drawee may honour (pay) or dishonour (refuse) the bill on the due date.

- If the bill is honoured, the drawer receives the payment directly from the drawee.

- This method involves no bank or third-party involvement until maturity.

A. Creditor sells goods on credit:

1. Books of Drawer / Creditor:

Debtor’s A/c ...Dr.

To Sales A/c

(Being goods sold on credit)

2. Books of Drawee / Debtor:

Purchases A/c ...Dr.

To Creditor’s A/c

(Being goods purchased on credit)

B. Drawer draws a bill, and acceptance received:

1. Books of Drawer / Creditor:

Bills Receivable A/c ...Dr.

To Drawee’s A/c

(Being bill drawn and acceptance received)

2. Books of Drawee / Debtor:

Drawer’s A/c ...Dr.

To Bills Payable A/c

(Being acceptance given)

C. Retained bill honoured on due date:

1. Books of Drawer / Creditor:

Cash / Bank A/c ...Dr.

To Bills Receivable A/c

(Being retained bill duly honoured on the due date)

2. Books of Drawee / Debtor:

Bills Payable A/c ...Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

D. Retained bill dishonoured on the due date:

1. Books of Drawer / Creditor:

Drawee’s A/c ...Dr.

To Bills Receivable A/c

(Being retained bill dishonoured on the due date)

2. Books of Drawee / Debtor:

Bills Payable A/c ...Dr.

To Drawee’s A/c

(Being our acceptance dishonoured on the due date)

E. Retained bill dishonoured and noting charges paid by Drawer:

1. Books of Drawer / Creditor:

Drawee’s A/c ...Dr.

To Bills Receivable A/c

To Cash A/c

(Being retained bill dishonoured on the due date and Noting Charges paid)

2. Books of Drawee / Debtor:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawee’s A/c

(Being our acceptance dishonoured and Noting Charges payable)

A. Drawer endorses the bill to Endorsee:

1. In the Books of Drawer/Endorser:

Endorsee’s A/c ...Dr.

To Bills Receivable A/c

(Being Drawee’s acceptance endorsed to our creditor)

2. In the Books of Drawee: No Entry

(Drawee is not a party to the endorsement transaction)

3. In the Books of Endorsee:

Bills Receivable A/c ...Dr.

To Endorser’s A/c

(Being Bills Receivable received from our debtor)

B. Endorsed bill honoured on the due date:

1. In the Books of Drawer / Endorser: No entry

(Drawer is not a party to the transaction)

2. In the Books of Drawee:

Bills Payable A/c Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

3. In the Books of Endorsee:

Cash / Bank A/c ...Dr.

To Bills Receivable A/c

(Being Bills Receivable received honoured)

C. Endorsed bill dishonoured on the due date:

1. In the Books of Drawer / Endorser:

Drawee’s A/c ...Dr.

To Endorsee’s A/c

(Being an endorsed bill dishonoured on the due date)

2. In the Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

3. In the Books of Endorsee:

Endorser’s A/c ...Dr.

To Bills Receivable A/c

(Being Bills Receivable dishonoured)

D. Endorsed bill dishonoured and noting charges paid by Endorsee:

1. In the Books of Drawer / Endorser:

Drawee’s A/c ...Dr.

To Endorsee’s A/c

(Being endorsed bill dishonoured and noting charges paid by Endorsee)

(Amount = Bill amount + Noting Charges)

2. In the Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and noting charges payable)

3. In the Books of Endorsee:

Endorser’s A/c ...Dr.

To Bills Receivable A/c

To Cash A/c

(Being Bills Receivable dishonoured and noting charges paid)

- Endorsement means transferring the title of a bill by signing it on the back and handing it over to another person.

- The person who transfers the bill is called the Endorser, and the one who receives it is the Endorsee.

- Endorsement is usually done to settle a debt the drawer or holder owes to others.

- A bill of exchange is a negotiable instrument and can be endorsed multiple times before maturity.

- On the due date, the endorsee presents the bill to the drawee and receives the payment.

A. Bill sent to the bank for collection:

1. Books of Drawer:

Bill Sent for Collection A/c ...Dr.

To Bills Receivable A/c

(Being bill sent to the bank for collection)

2. Books of Drawee: No entry

(Drawee is not a party to the transaction)

B. Bill sent to bank for collection honoured on the due date and bank charges debited by bank:

1. Books of Drawer:

Bank A/c ...Dr.

Bank Charges A/c ...Dr.

To Bill Sent for Collection A/c

(Being bill honoured and bank charges debited)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Cash / Bank A/c

(Being our acceptance honoured)

C. Bill sent to bank for collection dishonoured on the due date:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bill Sent for Collection A/c

(Being bill sent for collection dishonoured)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured)

D. Bill sent to bank for collection dishonoured on due date and Noting Charges paid:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bill Sent for Collection A/c

To Bank A/c

(Being bill sent for collection dishonoured and noting charges paid)

2. Books of Drawee:

Bills Payable A/c ...Dr.

Noting Charges A/c ...Dr.

To Drawer’s A/c

(Being our acceptance dishonoured and noting charges payable)

- The drawer can send the bill to the bank for collection instead of presenting it personally on the due date.

- The bank collects the amount from the drawee on the due date on behalf of the drawer.

- For this service, the bank charges a fee known as Bank Charges.

- A temporary account called “Bill Sent for Collection A/c” is opened by the drawer for this purpose.

- This account is closed when the bank collects the payment or if the bill is dishonoured.

A. Cancellation of old bill:

1. Books of Drawer:

Drawee’s A/c ...Dr.

To Bills Receivable A/c or

To Bank A/c or

To Bill Sent for Collection A/c or

To Endorsee’s A/c

(Being old bill cancelled)

2. Books of Drawee:

Bills Payable A/c ...Dr.

To Drawer A/c

(Being our acceptance cancelled)

B. Receiving final dividend and bad debts written off:

1. Books of Drawer:

Cash / Bank A/c ...Dr.

Bad Debts A/c ...Dr.

To Drawee’s A/c

(Being final dividend received and bad debts written off)

2. Books of Drawee:

Drawer’s A/c ...Dr.

To Cash / Bank A/c

To Deficiency A/c

(Being final dividend paid and balance credited to deficiency account)

1. Books of Drawer (Creditor/Seller):

Cash/Bank A/c ...Dr.

Rebate / Discount A/c ...Dr.

To Bills Receivable A/c

(Being bill retired and rebate allowed)

2. Books of Drawee (Debtor / Buyer):

Bills Payable A/c ...Dr.

To Cash / Bank A/c

To Rebate / Discount A/c

(Being our acceptance retired and rebate received)

- First Payment – Dissolution Expenses: Expenses related to the dissolution process are paid first from the firm's assets.

- Second – Outside Liabilities: All dues to third parties (e.g., creditors, loans, bank overdrafts) are settled next.

- Third – Partners’ Loans: If any money remains, it is used to repay loans given by partners to the firm.

- Fourth – Capital Repayment: Remaining surplus, if any, is distributed to partners against their capital balances.

- Profit Sharing Ratio: Any final surplus is shared among partners as per the agreed profit-sharing ratio.

| Basis | Firm’s Debts | Private Debts |

|---|---|---|

| Meaning | Debts owed by the firm to outsiders | Debts owed by a partner personally |

| Liability | All partners are jointly and severally liable | Only the concerned partner is liable |

| Application of Firm's Property | Used first to settle firm’s debts | Excess share (after firm’s debts) may be used for private debts |

| Application of Private Property | Surplus after private debts can be used for firm’s debts | Used first for private debts, then (if any) for firm’s debts |

Important Questions [19]

- Write a Word / Term / Phrase as a Substitute of the Following Statement. a Bill Which is Drawn in India and Payable in Other Country.

- Bank Account is Debited When a Bill is Sent to the Bank for Collection.

- Give one word/phrase/term which can substitute the following statement: Fees charged by Notary Public for getting the fact of dishonour noted.

- Give one word/phrase/term which can substitute the following statement:- Officer appointed by government for noting of dishonour of bill.

- Find the odd one: Retaining of Bill, Noting of Bill, Discounting of Bill, Endorsing of Bill.

- Journalise the following transactions in the books of Mr. Arvind. Bank informed that Sam’s acceptance for ₹ 30,000 sent to bank for collection has been honoured and bank charges debited ₹ 200.

- The Person Who Endorses Bill.

- Drawer and Payee of a Bill of Exchange May Be One and the Same Person.

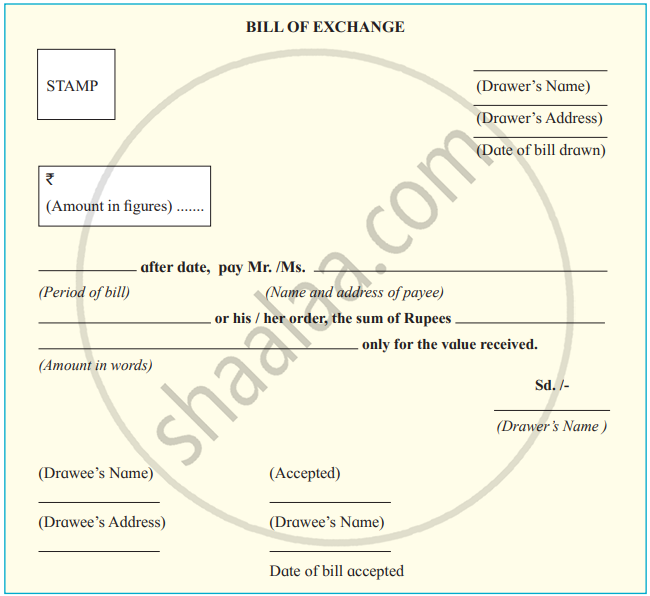

- Prepare a Specimen of Bill of Exchange from the Following Information

- Journalise the Following Transactions in the Books of 'Avadhoot'.(A) Nandini Informs Avadhoot that Nisha'S Acceptance for Rs. 5,000 Endorsed to Nandini Has Been Dishonoured

- The Balance Sheet of Samarth Traders is as Follows. the Partners Share Profits and Losses as 5 : 2 : 3,

- On andTh March 2016 Ram Drwas a Bill on Rohit for Rs 8000 at 3 Months. Rohit Accepts It and Returns to Ram. Ram Then Sends the Bill to His Bank for Collection.

- Journalise the Following Transactions in the Books of Jaydeep. (A) Arvind Renews His Acceptance of Jaydeep of Rs. 7,000 with Interest Rs. 500 for Two Months.

- Following Transactions in the Books of Mr. Vivek :On 1st January, 2010, Sameer Informs Vivek that Mahesh'S Acceptance for Rs 32,000 Endorsed to Sameer Has Been Dishonoured. Noting Charges Rs 800.

- Prepare a Specimen of Bill of Exchange from the Following Information

- Raja of Nagpur draws a bill on Pradhan of Bhandara for Rs. 6,000 at 3 months. Pradhan accepted and returned it to Raja. Raja then sent the bill to bank for collection.

- Date on Which Payment of a Bill is to Be Made.

- A Bill Which is Drawn in One Country and Made Payable in Other Country is Called __________.

- From the Following Information Prepare a Format of a Bill of Exchange:

Concepts [12]

- Necessity of Bill of Exchange (Only Trade Bill)

- Acceptance

- Concept of Bills of Exchange

- Honouring and Dishonouring of Bill of Exchange

- Accounting Treatment> Discounting the Bill of Exchange

- Accounting Treatment> Retaining the Bill till the Due Date

- Accounting Treatment> Endorsement of Bill of Exchanges

- Accounting Treatment > Bills Sent to Bank for Collection

- Insolvency of Drawee

- Retirement of Bill under Rebate

- Accounting at the Time of Dissolution of a Firm

- Examples on Bills of Exchange