Advertisements

Advertisements

प्रश्न

Show how under perfect competition the price of a commodity is equal to its average and marginal costs of production in the long-run. Does the perfectly competitive firm always operate at the minimum point of the average cost curve?

“In a perfectly competitive equilibrium, the price of a commodity is equal to the marginal and average cost of production.” Explain.

स्पष्ट कीजिए

विस्तार में उत्तर

Advertisements

उत्तर

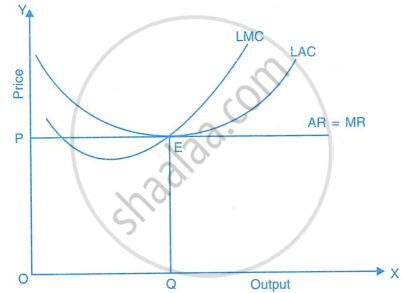

- In the long run, a firm under perfect competition earns only normal profit.

- Free entry and exit of firms ensure that abnormal profits or losses do not last.

- If firms earn supernormal profits, new firms enter the market.

- This increases industry supply, causing the market price to fall.

- As the price falls, supernormal profits reduce and become normal profits.

- If firms face losses, some firms exit the market.

- This decreases supply, raising the price until remaining firms earn normal profit.

- In the long run, firms earn just enough to cover all costs, i.e., normal profit.

- There is no incentive for new firms to enter or existing firms to exit.

- The firm is in equilibrium when LMC = MR and LMC cuts MR from below.

- Also, AR = LAC at equilibrium, ensuring normal profit.

- Since AR = MR in perfect competition, the equilibrium condition is:

LMC = MR = AR = LAC - This occurs at the minimum point of the LAC curve, where the firm produces optimum output.

- At this point, price = AR = MR = AC = MC, and the firm is fully efficient.

- Therefore, in the long run, the firm is in stable equilibrium with only normal profits.

shaalaa.com

क्या इस प्रश्न या उत्तर में कोई त्रुटि है?

अध्याय 13: Price Output Under Perfect Competition - TEST QUESTIONS [पृष्ठ १३.१९]