Advertisements

Advertisements

प्रश्न

From the following information, you are required to prepare a Cash Flow Statement of Messrs Nirmal & Co. Ltd. for the year ended 31st March, 2023, and give your comments about the same.

| BALANCE SHEET as at 31st March, 2023 | ||||

| Particulars | Note No. |

March 31, 2023 (₹) |

March 31, 2022 (₹) |

|

| I. | Equity & Liabilities | |||

| Shareholders’ Funds: | ||||

| Share Capital | 9,00,000 | 8,00,000 | ||

| Reserves and Surplus | 1,00,000 | 70,000 | ||

| Non-Current Liabilities | ||||

| Long-term Borrowings | 4,00,000 | - | ||

| Current Liabilities | ||||

| Trade Payables | 2,90,000 | 1,40,000 | ||

| Short-term Provision | 1 | 30,000 | 10,000 | |

| 17,20,000 | 10,20,000 | |||

| II. | Assets: | |||

| Non Current Assets | 2 | 10,10,000 | 6,00,000 | |

| Current Assets: | ||||

| Inventory | 4,00,000 | 1,50,000 | ||

| Trade Receivables | 2,00,000 | 50,000 | ||

| Cash Balance | 70,000 | 2,00,000 | ||

| Other Current Assets | 3 | 40,000 | 20,000 | |

| 17,20,000 | 10,20,000 | |||

Note:

| 2023 (₹) | 2022 (₹) | ||

| 1. | Short-term Provision: | ||

| Provision for Tax | 30,000 | 10,000 | |

| 2. | Non-Current Assets: | ||

| Plant & Machinery | 10,10,000 | 6,00,000 | |

| 3. | Other Current Assets: | ||

| Prepaid General Exp. | 40,000 | 20,000 | |

Additional Information:

- Interest paid on long-term borrowings ₹20,000.

- Depreciation charged during the year ₹60,000.

- Machinery discarded during the year ₹20,000.

- Provision for tax made during the year was ₹40,000.

- Interim Dividend paid ₹10,000.

Advertisements

उत्तर

Introduction of the Project:

The project work is to prepare a Cash Flow Statement and Comment upon the same.

Necessary data is provided in the form of Balance Sheets as at 31st March, 2022 and 2023. The data provided is used for the purpose of the project work.

The project work is planned and executed by preparing a Cash Flow Statement. The Plant & Machinery Account has also been prepared to ascertain the payments made for purchasing Plant & Machinery. A provision for the tax account has also been prepared to ascertain the tax payment during the year.

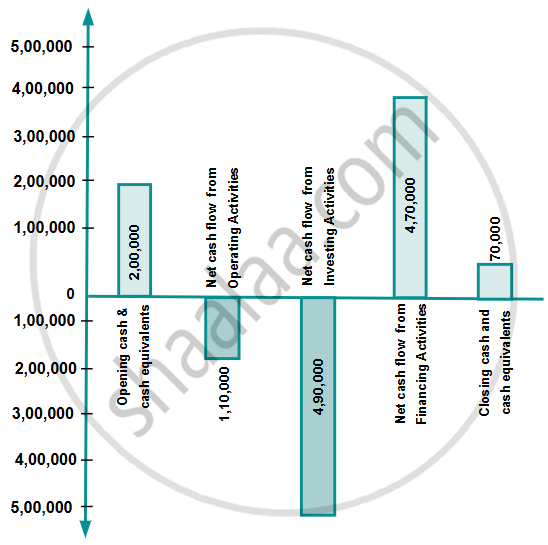

| CASH FLOW STATEMENT | ||||

| (As per AS-3 Revised) |

||||

| for the year ended 31st March, 2023 | ||||

| Particulars | Amount (₹) |

Amount (₹) |

Amount (₹) |

|

| A. | Cash flows from Operating Activities: | |||

| Net Profit before Tax (Note 1) | 80,000 | |||

| Adjustments For Non-Cash and Non-Operating Items: | ||||

| Add: Depreciation | 60,000 | |||

| Add: Machinery discarded | 20,000 | |||

| Add: Interest on Long-term Borrowings | 20,000 | |||

| Operating Profit before Working Capital Changes | 1,80,000 | |||

| Add: Increase in Trade Payables | 1,50,000 | |||

| 3,30,000 | ||||

| Less: Increase in Inventory | 2,50,000 | |||

| Less: Increase in Trade Receivables | 1,50,000 | |||

| Less: Increase in Prepaid Expenses | 20,000 | 4,20,000 | ||

| (90,000) | ||||

| Payment of Tax(3) | (20,000) | |||

| Loss of Cash in operating activities | (1,10,000) | (1,10,000) | ||

| B. | Cash flows from Investing Activities: | |||

| Purchase of Plant & Machinery(2) | (4,90,000) | (4,90,000) | ||

| C. | Cash flows from Financing Activities: | |||

| Issue of Share Capital | 1,00,000 | |||

| Long-Term Borrowings | 4,00,000 | |||

| Interim Dividend paid | (10,000) | |||

| Interest paid | (20,000) | |||

| Net cash from financing activities | 4,70,000 | 4,70,000 | ||

| Net decrease in cash and cash equivalents | (1,30,000) | |||

| Add: Cash and cash equivalents in the beginning | 2,00,000 | |||

| Add: Cash and cash equivalents at the end | 70,000 | |||

Notes:

(1)

| Amount (₹) |

|

| Calculation of Net Profit Before Tax: | |

| Profit & Loss on 31st March, 2023 | 1,00,000 |

| Profit & Loss on 31st March, 2022 | 70,000 |

| 30,000 | |

| Add: Current year’s Provision for Tax | 40,000 |

| Add: Interim Dividend Paid | 10,000 |

| 80,000 |

(2)

| PLANT & MACHINERY ACCOUNT | |||

| Particulars | Amount (₹) |

Particulars | Amount (₹) |

| To Balance b/d | 6,00,000 | By Depreciation A/c | 60,000 |

| To Bank A/c (Balancing figure, being purchase) | 4,90,000 | By Statement of P & L (Machinery discarded) | 20,000 |

| By Balance c/d | 10,10,000 | ||

| 10,90,000 | 10,90,000 | ||

(3)

| PROVISION FOR TAX ACCOUNT | |||

| Particulars | Amount (₹) |

Particulars | Amount (₹) |

| To Bank A/c (Balancing figure, being the payment of tax during the year) | 20,000 | By Balance b/d | 10,000 |

| To Balance c/d | 30,000 | By Statement of P & L (Provision made during the Current Year) | 40,000 |

| 50,000 | 50,000 | ||

PRESENTATION OF INFORMATION:

CASH FLOW ACTIVITIES IN NIRMAL & CO. LTD.

Comments:

- The operating tasks don’t bring in any cash. This is a bad situation for the business because it could have trouble getting cash in the future. An inventory going up from ₹1,50,000 to ₹4,00,000 could mean that the company has items that are taking a long time to sell. Also, the fact that trade receivables went from ₹50,000 to ₹2,00,000 shows that debt collection isn’t going well. It might make bad loans more likely.

- Inventory and trade debts have gone up a lot. The company should immediately remove the piled-up goods and collect the trade receivables.

- Almost twice as much money has been owed in trade. This may be because of a lack of cash, as trade debts are not being paid on time. The company should not wait to pay its trade debts because doing so will hurt its reputation and ability to get credit. It should get a loan from the bank to pay its trade debts.